Robert E. Sulentic Group President EMEA, Asia Pacific & Development Services India Overview Exhibit 99.9 |

| Robert E. Sulentic Group President EMEA, Asia Pacific & Development Services India Overview Exhibit 99.9 |

CB

Richard Ellis | Page 2 “India – the Growth Story” Population (2007 estimate): 1.1 billion Approx. 300 million ‘Middle Class’ fueling future growth GDP (Total): $4.0 trillion; Per Capita: $3,737 GDP growing at 7%+ annually India One of the largest economies in the world Service sector accounts for almost 60% of the GDP Consumption expenditures fueling economic growth – 78% of GDP |

CB

Richard Ellis | Page 3 Strong Fundamentals Received approximately $100 billion Foreign Direct Investment (FDI) since 1991 - $47 billion received in last 2 years Huge population of technically skilled English-speakers – one of the youngest in the world (median age approximately 25 years) Majority of the Fortune 500 companies already operate in India Emerging as a hub of manufacturing excellence - IT, Pharmaceuticals, Bio-Technology, Nano-Technology, Agri-Business 3.2 3.7 World 1.4 1.4 Japan 0.5 2.2 US 7.7 7.9 India 9.9 11.5 P.R. China 2008 GDP growth (%)* 2007 GDP growth (%)^ Source: National statistics departments, CBRE Research, EIU December 2007, AT

Kearney ^ EIU estimates, * EIU forecasts, IMF One of the fastest-growing economies in the world |

CBRE

India |

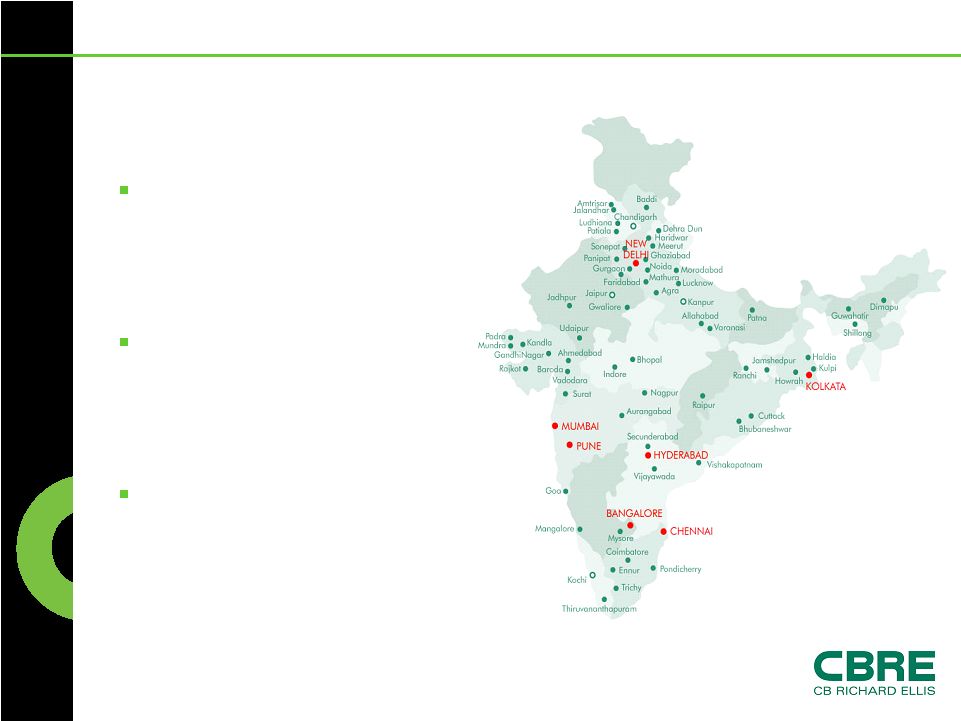

CB

Richard Ellis | Page 5 CBRE India – Market Presence Established in 1994 • First real estate services firm to set up operations in India Presence • Over 50 offices • Full service offices in 7 cities 1,300+ employees |

CB

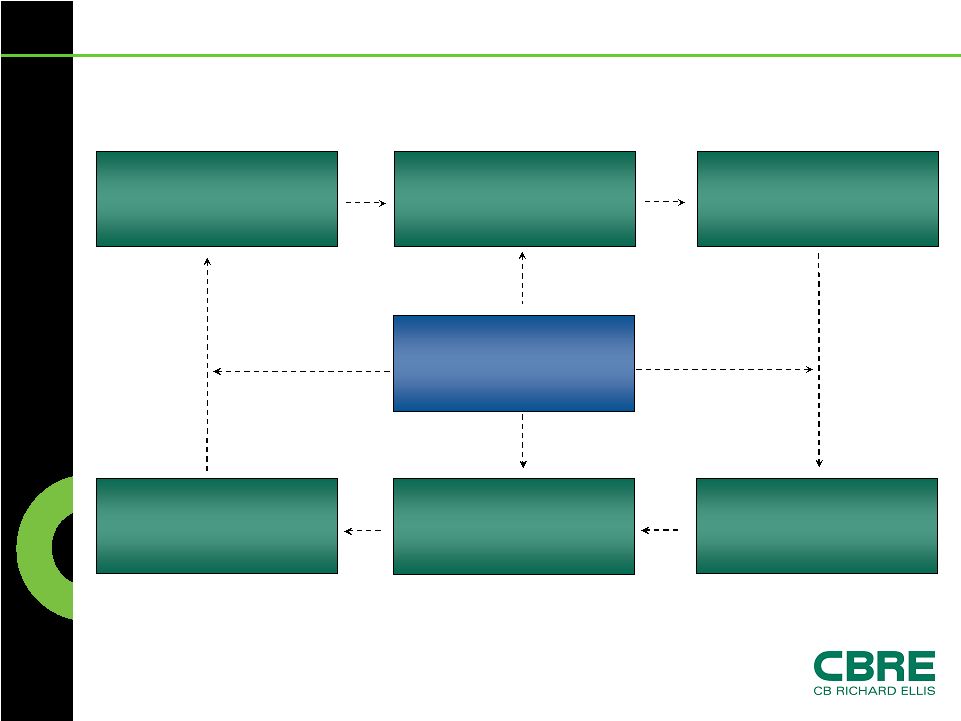

Richard Ellis | Page 6 CBRE India: Extensive Services

Portfolio Integrated Service Delivery Platform CBRE Consulting Transaction Management/ Corporate Services Project/Construction Management Facilities/Property Management Valuation Advisory Investment/Capital Markets |

CB

Richard Ellis | Page 7 India Capabilities 85 professionals More than 850 assignments across 85 cities • represented Federal and 14 state governments Approximately 55% of the business originates from repeat clients Emerging focus • Hospitality sector • Retail advisory • Infrastructure segments, e.g. logistics, etc. Consulting & Valuation Advisory |

CB

Richard Ellis | Page 8 India Capabilities 80 transaction professionals with strong relationships across India and globally More than 1,500 transaction assignments carried out across 33 cities Services more than 240 corporate clients – exclusive mandate or preferred relationship with more than 40 companies Emerging focus/New services • Landlord representation • Retail services • Industrial/Logistics Transaction Management/Corporate Services |

CB

Richard Ellis | Page 9 India Capabilities More than 285 professionals Assignments carried out for approximately 35 million square feet Executed projects in more than 30 locations 70% of clients are repeat business Emerging focus • Industrial/Logistics • Townships • Healthcare • Development consultancy ICICI BANK | Hyderabad 4,000,000 SF CISCO Systems | Bangalore 550,000 SF Project/Construction Management |

CB

Richard Ellis | Page 10 India Capabilities 840 professionals Property/Facilities Management for more than 50 million square feet 150+ clients spread over 470 facilities ISO 9001: 2000 certified systems and process Property/Facilities Management |

Indian Real Estate Markets & Our Role |

CB

Richard Ellis | Page 12 Bottlenecks continue but major focus on upgrades Big bottleneck area Infrastructure Improving – Greater transparency Bureaucratic and non-transparent Legal/Policy Framework Growing rapidly Minimal Financial Institution Participation High Low Underlying Demand Moving toward global standards Low Construction Quality Approximately 175 million sq. ft. (across Tier I cities only) Approximately 2.5 million sq. ft. Office Supply (Investment Grade) 2008 1994 Parameters Real Estate: Evolution and Existing Size |

CB

Richard Ellis | Page 13 Dramatically Growing Demand For

Professional Services Current Dynamics Liberalization of real estate FDI norms – scramble for projects Massive infrastructure development across the board Integration with financial markets – private placement/IPOs/M&A Industry getting organized and transparent On the Horizon Real Estate Mutual Funds REITS Further liberalization of FDI norms |

CB

Richard Ellis | Page 14 Opportunities Office Space • Commercial activity dominated by IT/back office • Additional demand for 100 million square feet expected over the next three years • Movement toward global quality standards Residential/Multi-Family Sector • India to add 150 to 200 million people by 2030, creating huge demand for urban housing • Integrated projects with focus on lifestyle orientation |

CB

Richard Ellis | Page 15 Opportunities Retail Sector • Huge potential: low per capita organized retail space (less than 15% of U.S.) • Movement toward liberalizing FDI requirements • Rising consumer spending fuels demand for more retail space Infrastructure Projects • Revamping/expansion of road networks and development of expressways • Focus on special economic zones • Greenfield airports and mass/rapid transport systems • Projects being implemented in public-private-partnership modes |

CB

Richard Ellis | Page 16 CBRE India Platform Geographical coverage with CBRE service, quality assurance and trust Unmatched depth of experience Readily available market intelligence in a “not-yet- fully-organized” market 14 years experience, which pre-dates organized development in the country Access to strongest professional real estate team in India Benefits to CBRE Global Clients |