Exhibit 99.3

|

|

LEASING OUTLOOK Jack Durburg Global President, Transaction Services |

Exhibit 99.3

|

|

LEASING OUTLOOK Jack Durburg Global President, Transaction Services |

|

|

Total lease value As of January 1, 2014; excludes affiliates Advise occupiers and investors in formulating and executing leasing strategies Tailored service delivery by property type and industry/market specialization Strategic insight and high-level execution driving significant market share gains Approximately 4,3502 leasing professionals worldwide OVERVIEW ($ in millions) Historical Fee Revenue YTD Q3 2013 Lease Transactions1 #1 Global Market Position Office: $56.2 billion Retail: $15.1 billion Industrial: $10.5 billion Other: $ 1.3 billion $83.1 billion |

|

|

MARKET GROWTH DRIVERS | AMERICAS Sustained, strong job growth Improved GDP growth in the second half of 2014 E-commerce growth (same/next-day delivery) Construction remains low but picking up Best office absorption in Q3 in seven years Q3 office rents up 1.3%; net absorption up 5% from Q2 16 straight quarters of falling industrial availability Q3 industrial rents up 0.5%; net absorption up 14.8% from Q2 Macro Trends Leasing Market Trends Volumes and Rents Outlook |

|

|

MARKET GROWTH DRIVERS | EMEA Likely zero growth in Eurozone in Q3, better in non-Eurozone countries and strong in UK ECB action has weakened Euro very good for exports Despite weak GDP growth, real estate demand improving, giving grounds for measured optimism Q3 office take up increased by 10%, while rents edged up by 1.3% from Q2 Q3 industrial take up posted 3%, increase while rents moved up 1% from Q2 Macro Trends Leasing Market Trends Volumes and Rents Outlook |

|

|

MARKET GROWTH DRIVERS | ASIA PACIFIC APAC growth slowing from 2013, but still strongest globally China in transition and facing weaker growth, but not recession Australia growth remains sub-par Growth improving in India Japan volatile but positive Emerging Asia countries benefiting from exports to U.S. Demand rising but strong construction activity will limit rent increases in some markets Q3 office take up increased 15%; rents rose 2.5% from Q2 Q3 industrial take up increased 6.5%; rents stable from Q2 Macro Trends Leasing Market Trends Volumes and Rents Outlook |

|

|

GROWTH STRATEGY VISION: Continue to lead our sector in the core business of Leasing and create more distance between CBRE and competitors Sales Management Integration with Other Business Lines Mergers and Acquisitions Client Care and Development Platform Enhancements Recruiting and Retention Matrix Leadership |

|

|

Geographic Footprint CBRE STRENGTHS Entrepreneurial and Collaborative Culture Sales Management Operating Model Depth of Service Offering Resources Tools Enviable Client Roster Top Talent Across Service Lines and Markets |

|

|

2014 U.S. SUCCESS STEWART TITLE CBRE’s Role Collaboration across CBRE service lines Brokerage Capital Markets Labor Analytics Location Incentive Practice Project Management Workplace Strategies Produce exceptional total outcome for Stewart Title Key Facts 240,000 square foot occupier lease Advisory and Transaction solution Integrated multiple service lines to drive more value to client HOUSTON Texas |

|

|

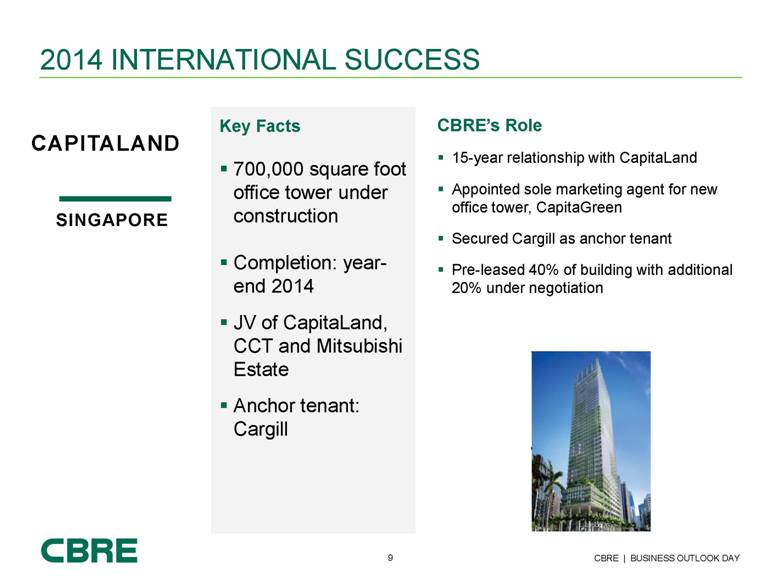

2014 INTERNATIONAL SUCCESS CAPITALAND CBRE’s Role 15-year relationship with CapitaLand Appointed sole marketing agent for new office tower, CapitaGreen Secured Cargill as anchor tenant Pre-leased 40% of building with additional 20% under negotiation Key Facts 700,000 square foot office tower under construction Completion: year-end 2014 JV of CapitaLand, CCT and Mitsubishi Estate Anchor tenant: Cargill SINGAPORE |