Exhibit 99.2

|

|

CBRE Group, Inc. Fourth Quarter 2012 Earnings Conference Call February 6, 2013 |

Exhibit 99.2

|

|

CBRE Group, Inc. Fourth Quarter 2012 Earnings Conference Call February 6, 2013 |

|

|

Forward-Looking Statements This presentation contains statements that are forward looking within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding our future growth momentum, operations, financial performance and business outlook. These statements should be considered as estimates only and actual results may ultimately differ from these estimates. Except to the extent required by applicable securities laws, we undertake no obligation to update or publicly revise any of the forward-looking statements that you may hear today. Please refer to our fourth quarter earnings report, filed on Form 8-K, our current annual report on Form 10-K and our current quarterly report on Form 10-Q, in particular any discussion of risk factors or forward-looking statements, which are filed with the SEC and available at the SEC’s website (www.sec.gov), for a full discussion of the risks and other factors that may impact any estimates that you may hear today. We may make certain statements during the course of this presentation, which include references to “non-GAAP financial measures,” as defined by SEC regulations. As required by these regulations, we have provided reconciliations of these measures to what we believe are the most directly comparable GAAP measures, which are attached hereto within the appendix. |

|

|

Conference Call Participants Bob Sulentic PRESIDENT AND CHIEF EXECUTIVE OFFICER Gil Borok CHIEF FINANCIAL OFFICER Bill Concannon CHIEF EXECUTIVE OFFICER, GLOBAL CORPORATE SERVICES Nick Kormeluk INVESTOR RELATIONS |

|

|

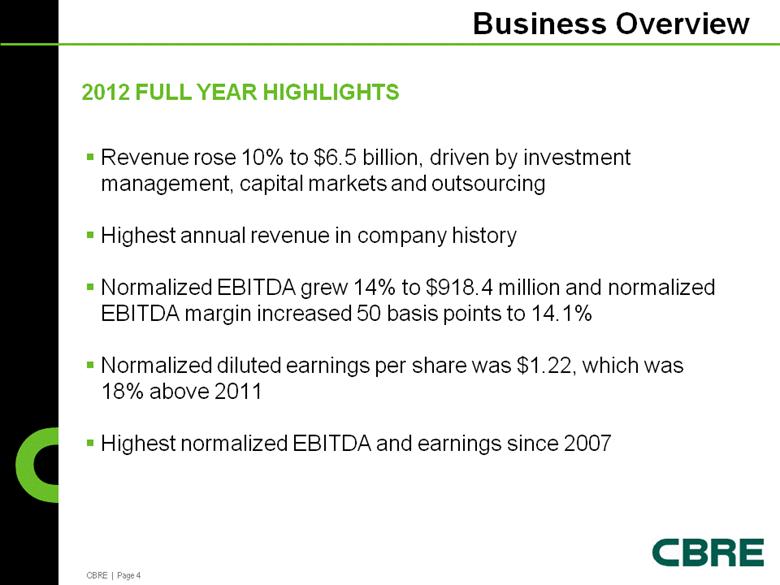

Business Overview 2012 FULL YEAR HIGHLIGHTS Revenue rose 10% to $6.5 billion, driven by investment management, capital markets and outsourcing Highest annual revenue in company history Normalized EBITDA grew 14% to $918.4 million and normalized EBITDA margin increased 50 basis points to 14.1% Normalized diluted earnings per share was $1.22, which was 18% above 2011 Highest normalized EBITDA and earnings since 2007 |

|

|

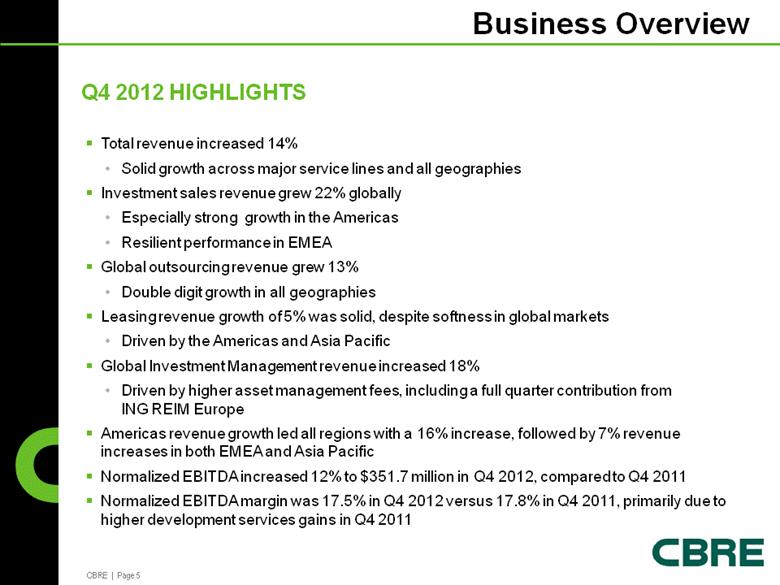

Business Overview Q4 2012 HIGHLIGHTS Total revenue increased 14% Solid growth across major service lines and all geographies Investment sales revenue grew 22% globally Especially strong growth in the Americas Resilient performance in EMEA Global outsourcing revenue grew 13% Double digit growth in all geographies Leasing revenue growth of 5% was solid, despite softness in global markets Driven by the Americas and Asia Pacific Global Investment Management revenue increased 18% Driven by higher asset management fees, including a full quarter contribution from ING REIM Europe Americas revenue growth led all regions with a 16% increase, followed by 7% revenue increases in both EMEA and Asia Pacific Normalized EBITDA increased 12% to $351.7 million in Q4 2012, compared to Q4 2011 Normalized EBITDA margin was 17.5% in Q4 2012 versus 17.8% in Q4 2011, primarily due to higher development services gains in Q4 2011 |

|

|

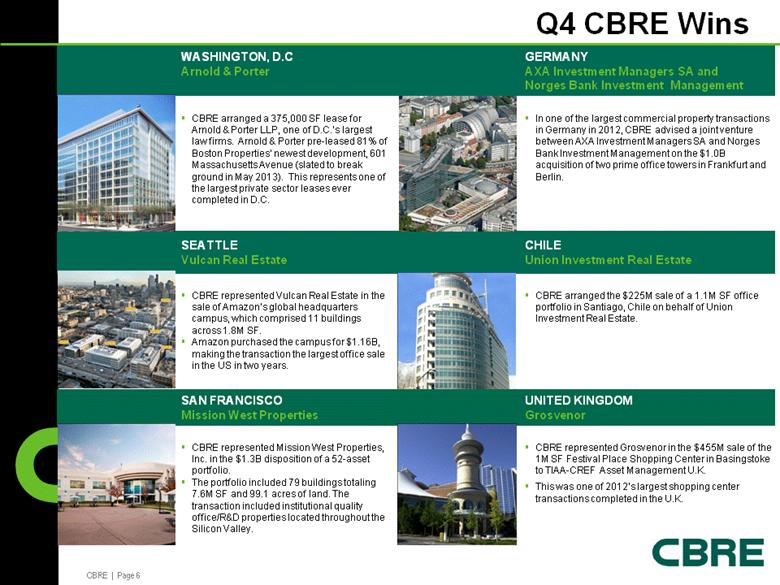

WASHINGTON, D.C Arnold & Porter GERMANY AXA Investment Managers SA and Norges Bank Investment Management CBRE arranged a 375,000 SF lease for Arnold & Porter LLP, one of D.C.’s largest law firms. Arnold & Porter pre-leased 81% of Boston Properties’ newest development, 601 Massachusetts Avenue (slated to break ground in May 2013). This represents one of the largest private sector leases ever completed in D.C. In one of the largest commercial property transactions in Germany in 2012, CBRE advised a joint venture between AXA Investment Managers SA and Norges Bank Investment Management on the $1.0B acquisition of two prime office towers in Frankfurt and Berlin. SEATTLE Vulcan Real Estate CHILE Union Investment Real Estate CBRE represented Vulcan Real Estate in the sale of Amazon’s global headquarters campus, which comprised 11 buildings across 1.8M SF. Amazon purchased the campus for $1.16B, making the transaction the largest office sale in the US in two years. CBRE arranged the $225M sale of a 1.1M SF office portfolio in Santiago, Chile on behalf of Union Investment Real Estate. SAN FRANCISCO Mission West Properties UNITED KINGDOM Grosvenor CBRE represented Mission West Properties, Inc. in the $1.3B disposition of a 52-asset portfolio. The portfolio included 79 buildings totaling 7.6M SF and 99.1 acres of land. The transaction included institutional quality office/R&D properties located throughout the Silicon Valley. CBRE represented Grosvenor in the $455M sale of the 1M SF Festival Place Shopping Center in Basingstoke to TIAA-CREF Asset Management U.K. This was one of 2012’s largest shopping center transactions completed in the U.K. Q4 CBRE Wins |

|

|

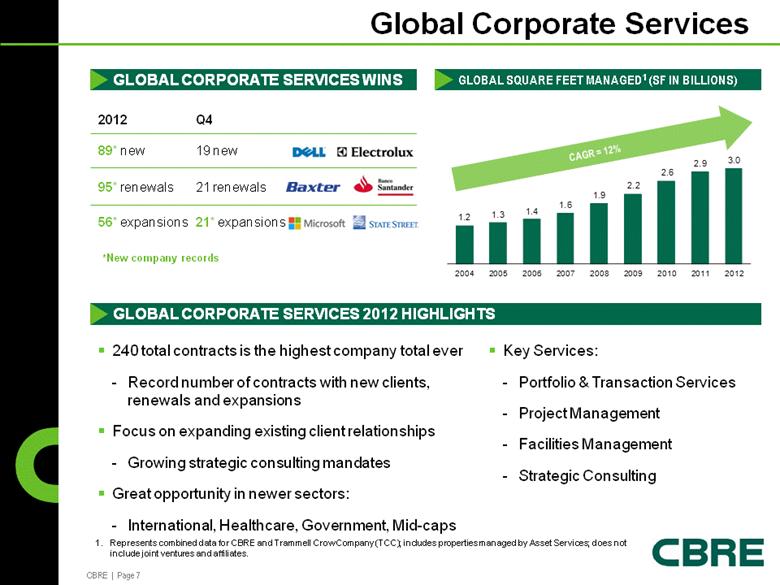

Global Corporate Services 1. Represents combined data for CBRE and Trammell Crow Company (TCC); includes properties managed by Asset Services; does not include joint ventures and affiliates. 2012 Q4 89* new 19 new 95* renewals 21 renewals 56* expansions 21* expansions 240 total contracts is the highest company total ever Record number of contracts with new clients, renewals and expansions Focus on expanding existing client relationships Growing strategic consulting mandates Great opportunity in newer sectors: International, Healthcare, Government, Mid-caps *New company records CAGR = 12% GLOBAL CORPORATE SERVICES WINS GLOBAL SQUARE FEET MANAGED1 (SF IN BILLIONS) GLOBAL CORPORATE SERVICES 2012 HIGHLIGHTS Key Services: Portfolio & Transaction Services Project Management Facilities Management Strategic Consulting 1 . 2 1 . 3 1 . 4 1 . 6 1 . 9 2 . 2 2 . 6 2 . 9 3 . 0 2004 2005 2006 2007 2008 2009 2010 2011 2012 |

|

|

Global Corporate Services Macro Trends *McKinsey Report estimated Global Real Estate outsourcing market size to be ~$50B Clients Continue to Shift Towards CRE Centralization Clients Continue to Rationalize Supply Chain Activities New Markets & Sectors are Emerging CRE Market Size Holds Potential for Additional Growth* $50B |

|

|

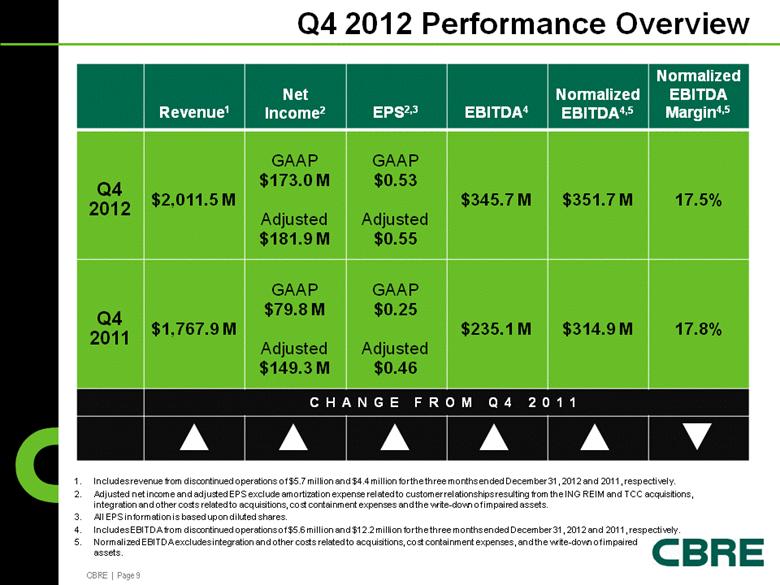

Q4 2012 Performance Overview 1. Includes revenue from discontinued operations of $5.7 million and $4.4 million for the three months ended December 31, 2012 and 2011, respectively. 2. Adjusted net income and adjusted EPS exclude amortization expense related to customer relationships resulting from the ING REIM and TCC acquisitions, integration and other costs related to acquisitions, cost containment expenses and the write-down of impaired assets. 3. All EPS information is based upon diluted shares. 4. Includes EBITDA from discontinued operations of $5.6 million and $12.2 million for the three months ended December 31, 2012 and 2011, respectively. 5. Normalized EBITDA excludes integration and other costs related to acquisitions, cost containment expenses, and the write-down of impaired assets. Revenue1 Net Income2 EPS2,3 EBITDA4 Normalized EBITDA4,5 Normalized EBITDA Margin4,5 Q4 2012 $2,011.5 M GAAP $173.0 M Adjusted $181.9 M GAAP $0.53 Adjusted $0.55 $345.7 M $351.7 M 17.5% Q4 2011 $1,767.9 M GAAP $79.8 M Adjusted $149.3 M GAAP $0.25 Adjusted $0.46 $235.1 M $314.9 M 17.8% CHANGE FROM Q4 2011 |

|

|

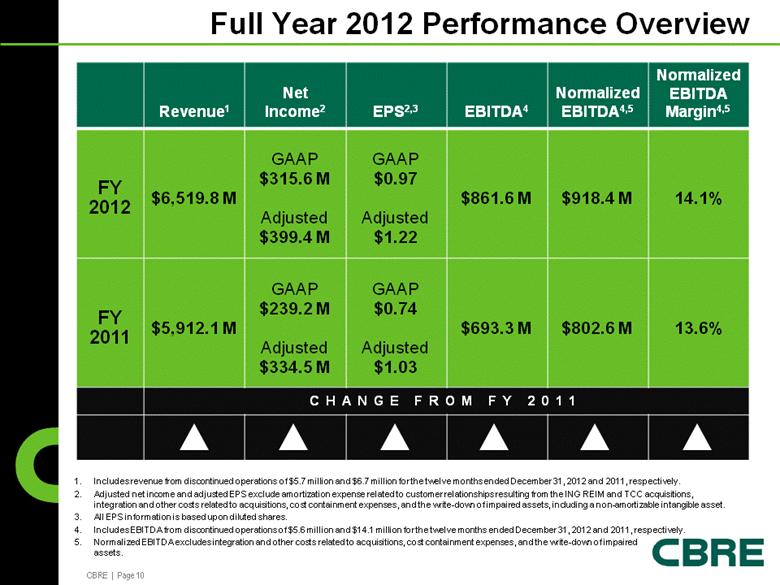

Full Year 2012 Performance Overview 1. Includes revenue from discontinued operations of $5.7 million and $6.7 million for the twelve months ended December 31, 2012 and 2011, respectively. 2. Adjusted net income and adjusted EPS exclude amortization expense related to customer relationships resulting from the ING REIM and TCC acquisitions, integration and other costs related to acquisitions, cost containment expenses, and the write-down of impaired assets, including a non-amortizable intangible asset. 3. All EPS information is based upon diluted shares. 4. Includes EBITDA from discontinued operations of $5.6 million and $14.1 million for the twelve months ended December 31, 2012 and 2011, respectively. Normalized EBITDA excludes integration and other costs related to acquisitions, cost containment expenses, and the write-down of impaired assets. Revenue1 Net Income2 EPS2,3 EBITDA4 Normalized EBITDA4,5 5. Normalized EBITDA Margin4,5 FY 2012 $6,519.8 M GAAP $315.6 M Adjusted $399.4 M GAAP $0.97 Adjusted $1.22 $861.6 M $918.4 M 14.1% FY 2011 $5,912.1 M GAAP $239.2 M Adjusted $334.5 M GAAP $0.74 Adjusted $1.03 $693.3 M $802.6 M 13.6% CHANGE FROM FY 2011 |

|

|

Revenue Breakdown 1. Includes revenue from discontinued operations of $5.7 million and $4.4 million for the three months ended December 31, 2012 and 2011, respectively. 2. 2. Contains recurring revenue aggregating approximately 55% of total revenue for the three months ended December 31, 2012. 4TH QUARTER 2012 Three months ended December 31, % Change ($ in millions) 20121 20111 USD Local Currency Leasing2 621.4 590.8 5 5 Property & Facilities Management2 611.8 539.6 13 14 Sales 384.5 314.2 22 22 Appraisal & Valuation 118.2 108.9 9 9 Investment Management2 116.5 96.7 21 22 Commercial Mortgage Brokerage2 100.5 72.6 38 38 Development Services 30.3 17.5 73 73 Other 28.3 27.6 3 2 Total 2,011.5 1,767.9 14 14 |

|

|

FULL YEAR 2012 Revenue Breakdown 1. Includes revenue from discontinued operations of $5.7 million and $6.7 million for the twelve months ended December 31, 2012 and 2011, respectively. 2. Contains recurring revenue aggregating approximately 59% of total revenue for the twelve months ended December 31, 2012. Twelve months ended December 31, % Change ($ in millions) 20121 20111 USD Local Currency Leasing2 1,911.4 1,909.0 - 1 Property & Facilities Management2 2,244.5 2,038.4 10 12 Sales 1,058.2 954.6 11 13 Appraisal & Valuation 384.5 365.4 5 7 Investment Management2 452.3 251.9 80 85 Commercial Mortgage Brokerage2 300.0 228.6 31 31 Development Services 74.7 65.4 14 14 Other 94.2 98.8 -5 -4 Total 6,519.8 5,912.1 10 12 |

|

|

US Market Statistics Source: CBRE Econometric Advisors (EA) Outlooks 1Q 2013 preliminary Starting in Q2 2011 retail was expanded to include strip centers, neighborhood centers and community centers US Vacancy US Absorption Trends (in millions of square feet) 4Q11 3Q12 4Q12 4Q13 F 4Q14F 2011 2012 2013F 2014F 4Q11 4Q12 Office 16.0% 15.6% 15.4% 15.2% 14.4% 26.3 28.7 22.2 39.6 9.0 8.4 Industrial 13.5% 13.1% 12.8% 12.2% 11.5% 122.7 127.9 126.4 154.7 25.6 55.9 Retail 13.1% 12.9% 12.8% 11.8% 11.1% 5.2 15.0 31.1 38.4 4.1 6.2 Cap Rates Stable and Volumes Up Cap Rate Growth 1 4Q11 3Q12 4Q12 4Q13 F Office Volume ($B) 20.7 17.6 29.1 Cap Rate 7.4% 7.2% 7.0% -10 to +50 bps Industrial Volume ($B) 8.6 8.5 13.5 Cap Rate 7.8% 7.8% 7.8% 0 to +30 bps Retail Volume ($B) 12.0 9.3 18.4 Cap Rate 7.4% 7.2% 7.4% -10 to +30 bps Source: CBRE EA Estimates from RCA data Jan 2013 1. CBRE EA estimates |

|

|

Sales, Leasing and Outsourcing Revenue: Americas Total Q4 2012 revenue was up 16% SALES LEASING OUTSOURCING ($ in millions) 32% Q4 FULL YEAR 20% 7% 4% 13% 12% 2011 2012 |

|

|

Sales, Leasing and Outsourcing Revenue: EMEA 0% or 4% in local currency (12%) or (7%) in local currency 13% or 14% in local currency 3% or 9% in local currency 0% or 1% in local currency 17% or 20% in local currency SALES LEASING OUTSOURCING ($ in millions) Total Q4 2012 revenue was up 7% or 8% in local currency Q4 FULL YEAR 2011 2012 |

|

|

Sales, Leasing and Outsourcing Revenue: Asia Pacific (8%) or (7%) in local currency 2% or 3% in local currency 8% or 13% in local currency (1%) or (3%) in local currency 7% and 7% in local currency 13% or 14% in local currency SALES LEASING OUTSOURCING ($ in millions) Total Q4 2012 revenue was up 7% or 8% in local currency Q4 FULL YEAR 2011 2012 |

|

|

Development Services 1. In Process figures include Long-Term Operating Assets (LTOA) of $1.2 billion for 4Q 12, $1.5 billion for 4Q 11, $1.6 billion for 4Q 10, $1.4 billion for 4Q 09 and $0.4 billion for both 4Q 08 and 4Q 07. LTOA are projects that have achieved a stabilized level of occupancy or have been held 18-24 months following shell completion or acquisition. 1. Includes revenue from discontinued operations of $4.9 million for both the three and twelve months ended December 31, 2012 and $1.3 million for both the three and twelve months ended December 31, 2011. 2. Includes EBITDA from discontinued operations of $5.1 million for both the three and twelve months ended December 31, 2012 and $10.1 million for both the three and twelve months ended December 31, 2011. PROJECTS IN PROCESS/PIPELINE ($ IN BILLIONS) HIGHLIGHTS $70.5 million of co-investments at the end of Q4 2012 $16.1 million in recourse debt to CBRE and repayment guarantees at the end of Q4 2012 2.2 3.8 5.0 4.9 3.6 2.8 2.6 3.6 5.4 6.5 5.6 4.7 4.9 4.9 4.2 2.3 1.4 2.0 2.3 1.4 1.5 2.5 2.7 3.0 2.7 2.5 0.9 1.2 1.2 2.1 4Q98 4Q99 4Q00 4Q01 4Q02 4Q03 4Q04 4Q05 4Q06 4Q07 4Q08 4Q09 4Q10 4Q11 4Q12 In Process Pipeline ($ in millions) 12/31/2012 12/31/2011 12/31/2012 12/31/2011 Revenue 1 33.3 22.4 83.7 77.6 EBITDA 2 35.6 49.4 51.7 76.1 Add Back: Net write-down of impaired assets - 2.7 - 4.1 Normalized EBITDA 2 35.6 52.1 51.7 80.2 EBITDA Margin 2 107% 233% 62% 103% THREE MONTHS ENDED TWELVE MONTHS ENDED |

|

|

Global Investment Management 1. Includes revenue from discontinued operations of $0.8 million for both the three and twelve months ended December 31, 2012. 2. Includes revenue from discontinued operations of $3.1 million and $5.5 million for the three and twelve months ended December 31, 2011, respectively. Investment Management Carried Interest 2 Asset Management Acquisition, Disposition & Incentive Rental Carried Interest 2 1 1 2 1 ANNUAL REVENUE ($ IN MILLIONS) CAGR = 24% FULL YEAR REVENUE ($ IN MILLIONS) Q4 REVENUE ($ IN MILLIONS) Asset Management Acquisition, Disposition & Incentive Rental 57.1 68.4 94.0 99.3 126.3 259.2 160.8 141.4 195.7 294.0 483.4 28.0 101.7 88.7 0.4 19.9 1.5 57.1 68.4 94.0 127.3 228.0 347.9 161.2 141.4 215.6 295.5 483.4 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 |

|

|

Global Investment Management Performance of combined legacy and ING REIM businesses in line with expectations CBRE Strategic Partners (SP) US Value 6 fund closed with $1.1 billion of equity commitments, exceeding expectations CBRE’s co-investments totaled $211.5 million at the end of Q4 2012 ASSETS UNDER MANAGEMENT ($ IN BILLIONS) CAGR = 23% HIGHLIGHTS 400 S. HOPE, LOS ANGELES Owned by CBRE SP US Value 6 11.4 14.4 15.1 17.3 28.6 37.8 38.5 34.7 37.6 94.1 92.0 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 |

|

|

Global Investment Management Pro-forma Normalized EBITDA For the three months ended December 31, 2012 and 2011, the Company recorded net carried interest compensation expense pertaining to future periods of $6.0 million and $10.5 million, respectively. For the twelve months ended December 31, 2012 and 2011, the Company recorded net carried interest compensation expense pertaining to future periods of $8.3 million and $24.2 million, respectively. As of December 31, 2012, the Company maintained a cumulative remaining accrual of such compensation expense of approximately $48 million, which pertains to anticipated future carried interest revenue. 1. Includes EBITDA from discontinued operations of $0.5 million for both the three and twelve months ended December 31, 2012 and $2.1 million and $4.0 million for the three and twelve months ended December 31, 2011, respectively. 2. Calculation includes EBITDA and revenue from discontinued operations. Three Months Ended December 31, Twelve Months Ended December 31, ($ in millions) 2012 2011 2012 2011 EBITDA 1 18.5 (29.4) 96.4 (14.8) Add Back: Integration and other costs related to acquisitions 5.9 45.0 39.2 66.7 Write-down of investments - 0.9 - 5.4 Normalized EBITDA 1 24.4 16.5 135.6 57.3 Net accrual of incentive compensation expense related to carried interest revenue not yet recognized 6.0 10.5 8.3 24.2 Pro-forma Normalized EBITDA 1 30.4 27.0 143.9 81.5 Pro-forma Normalized EBITDA Margin 2 24% 25% 30% 28% |

|

|

Mandatory Amortization and Maturity Schedule $ in millions $700.0 million revolver facility matures in May 2015. As of December 31, 2012, the outstanding revolver balance was $73.0 million. As of December 31, 2012 1 Global Cash Revolver Available 1 , 607 71 76 373 424 458 378 370 350 - 250 . 0 500 . 0 750 . 0 1 , 000 . 0 1 , 250 . 0 1 , 500 . 0 1 , 750 . 0 Q 4 2012 2013 2014 2015 2016 2017 2018 2019 2020 Term Loan A Term Loan A - 1 Term Loan B Term Loan C Term Loan D Sr. Subordinated Notes Sr. Unsecured Notes Revolver Current Liquidity |

|

|

Capitalization Excludes $94.6 million and $208.1 million of cash in consolidated funds and other entities not available for Company use at December 31, 2012 and December 31, 2011, respectively. Net of original issue discount of $9.5 million and $11.0 million at December 31, 2012 and December 31, 2011, respectively. Represents notes payable on real estate in Development Services that are recourse to the Company. Excludes non-recourse notes payable on real estate of $312.1 million and $359.3 million at December 31, 2012 and December 31, 2011, respectively. Excludes $1,026.4 million and $713.4 million of aggregate warehouse facilities at December 31, 2012 and December 31, 2011, respectively. ($ in millions) 12/31/2012 12/31/2011 Variance Cash 1 994.7 885.1 109.6 Revolving credit facility 73.0 44.8 28.2 Senior secured term loan A 271.3 306.2 (34.9) Senior secured term loan A-1 275.2 285.1 (9.9) Senior secured term loan B 293.2 296.3 (3.1) Senior secured term loan C 394.0 398.0 (4.0) Senior secured term loan D 394.0 398.0 (4.0) Senior subordinated notes 2 440.5 439.0 1.5 Senior unsecured notes 350.0 350.0 - Notes payable on real estate 3 13.9 13.6 0.3 Other debt 4 9.4 0.1 9.3 Total debt 2,514.5 2,531.1 (16.6) Stockholders' equity 1,539.2 1,151.5 387.7 Total capitalization 4,053.7 3,682.6 371.1 Total net debt 1,519.8 1,646.0 (126.2) As of |

|

|

Business Outlook We expect 2013 to be the fourth year in a slow commercial real estate recovery Overall revenue is expected to grow in the mid to high single digits Leasing revenue expected to strengthen modestly in the second half Investment sales revenue should increase in line with improving fundamentals Outsourcing growth is expected to be in the low double digits We believe growth will again be paced by the Americas, with Asia Pacific rebounding and EMEA challenged by a weak macro environment Assuming the recovery continues as described, we expect some moderate expansion of our industry-leading margins while modestly increasing our platform investments to bolster long-term, profitable growth EPS is expected to be in a range of $1.40 to $1.45 implying a growth rate of approximately 15% to 20% 2013 EXPECTATIONS |

|

|

GAAP Reconciliation Tables |

|

|

Reconciliation of Normalized EBITDA to EBITDA to Net Income ($ in millions) 2012 2011 2012 2011 Normalized EBITDA 351.7 $ 314.9 $ 918.4 $ 802.6 $ Adjustments: Integration and other costs related to acquisitions 6.0 45.1 39.2 68.8 Cost containment expenses - 31.1 17.6 31.1 Write-down of impaired assets - 3.6 - 9.4 EBITDA 345.7 235.1 861.6 693.3 Add: Interest income 1.9 2.4 7.6 9.4 Less: Depreciation and amortization 46.0 36.5 170.9 116.9 Interest expense 44.6 45.1 176.6 153.5 Non-amortizable intangible asset impairment - - 19.8 - Provision for income taxes 84.0 76.1 186.3 193.1 Net income attributable to CBRE Group, Inc. 173.0 79.8 315.6 239.2 Revenue 2,011.5 $ 1,767.9 $ 6,519.8 $ 5,912.1 $ Normalized EBITDA Margin 17.5% 17.8% 14.1% 13.6% Three Months Ended December 31, Twelve Months Ended December 31, |

|

|

Reconciliation of Net Income to Net Income, As Adjusted ($ in millions, except for per share data) 2012 2011 2012 2011 Net income attributable to CBRE Group, Inc. 173.0 $ 79.8 $ 315.6 $ 239.2 $ Integration and other costs related to acquisitions, net of tax 4.5 42.8 29.9 59.6 Amortization expense related to ING REIM and TCC incentive fees and customer relationships acquired, net of tax 4.4 3.9 25.4 9.4 Non-amortizable intangible asset impairment, net of tax - - 15.0 - Cost containment expenses, net of tax - 20.6 13.5 20.6 Write-down of impaired assets, net of tax - 2.2 - 5.7 Net income attributable to CBRE Group, Inc., as adjusted 181.9 $ 149.3 $ 399.4 $ 334.5 $ Diluted income per share attributable to CBRE Group, Inc., as adjusted 0.55 $ 0.46 $ 1.22 $ 1.03 $ Weighted average shares outstanding for diluted income per share 329,012,910 324,117,111 327,044,145 323,723,755 Three Months Ended December 31, Twelve Months Ended December 31, |