Exhibit 99.8

|

|

Brokerage Overview Jack Durburg Global President, Transaction Services December 6, 2012 |

Exhibit 99.8

|

|

Brokerage Overview Jack Durburg Global President, Transaction Services December 6, 2012 |

|

|

Overview Global leasing trends Global sales trends Strategy and opportunities |

|

|

Global Leasing Trends 1. CBRE and TCC revenue for the period December 20, 2006, through December 31, 2006 Q3 2012 Update 1 Global Leasing Revenue ($ in Millions) Incremental market recovery still evident, despite general softening in Q3 2012. Performance globally was mixed. U.S. vacancy continues to edge down as job growth remains strong enough to produce positive absorption. Slow market improvement forecasted to continue across most property types. Caution among occupiers resulting in dearth of large transactions across EMEA. However, vacancy and rents holding relatively steady due to limited development activity. Economic ills in U.S. and Europe slowed demand for space in Asia Pacific; most leasing activity came from domestic companies. Overall rents have changed little through Q3 and expected to recover marginally in 2013. Lack of speculative construction will aid market rebound when firmer space demand revives. |

|

|

U.S. Office Leases Sq.Ft. Number of Leases Average Lease Size # of Leases YTD Q3 Q4 |

|

|

Global Sales Trends 1. CBRE and TCC revenue for the period December 20, 2006, through December 31, 2006 Q3 2012 Update 1 Global Sales Revenue ($ in Millions) Global business centers seen as safe havens continue to draw investment capital. Debt financing generally remains available in these markets, especially for core assets. Gateway U.S. markets have led the recovery, primarily on both coasts. Multi-housing properties remain the market bellwether due to strong demand/rent growth and liquidity provided by government agencies. EMEA investment markets are polarized with the U.K., Germany, and the Nordics drawing the most interest. Risk aversion has been widening pricing gap between prime and secondary assets, with yields relatively stable for the best assets. Asia Pacific investment activity remains largely stable but not expected to revive significantly until stronger growth in China returns and Western economies gain momentum. Office remains the favored asset class but growing interest in retail. Cross-border capital flows remain highly active, targeting well-leased assets in the largest, most liquid global business centers. |

|

|

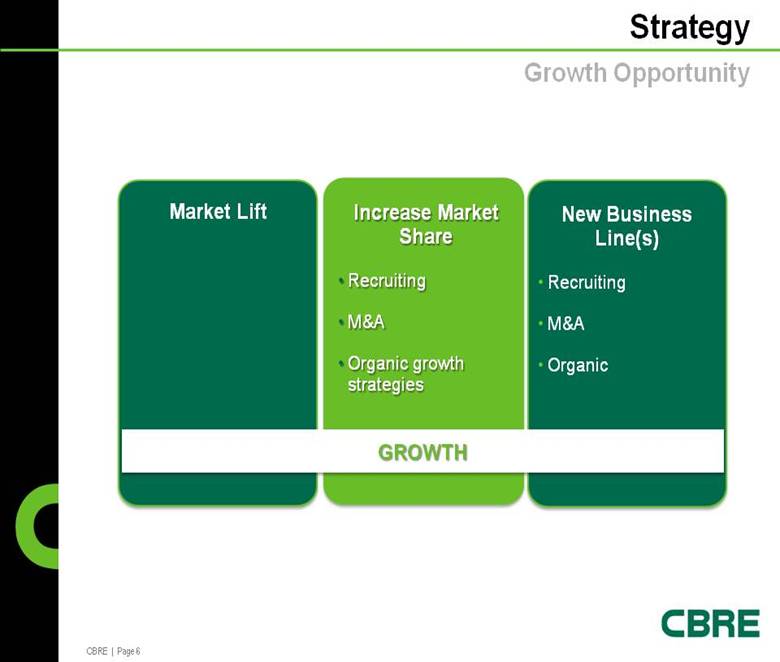

Strategy GROWTH New Business Line(s) Recruiting M&A Organic Increase Market Share Recruiting M&A Organic growth strategies Market Lift Growth Opportunity |

|

|

Matrix Leadership Structure Go-to-Market Strategy Recruiting M&A Global Connectivity PRIORITY Strategy Growth Plan |

|

|

Americas EMEA APAC Investor Services Office Retail Industrial Occupier Services Finance GCS Transaction Management Occupier Brokerage Agency Brokerage Capital Markets Office Industrial Retail Investment Sales Platform Office Retail Industrial Multi Housing Hotels Advisory The Winning Structure Service Line Structure |

|

|

Strategy Transcends Geography Occupier Clients and Investor Clients Service Delivery and Go-to-Market Strategy |

|

|

Go-to-Market Strategy Leasing Capital Markets Americas APAC EMEA Global Brokerage Plan Managed Brokerage Occupier Playbook Agency Playbook Finishing First Global Capital Markets Plan Producer Gap Analysis & Recruiting Plan Managed Brokerage Finishing First Global Global CRM Global Recruiting Process Global and Regional M&A Process |