Exhibit 99.7

|

|

Global Corporate Services Overview Bill Concannon CEO Global Corporate Services (GCS) December 6, 2012 |

Exhibit 99.7

|

|

Global Corporate Services Overview Bill Concannon CEO Global Corporate Services (GCS) December 6, 2012 |

|

|

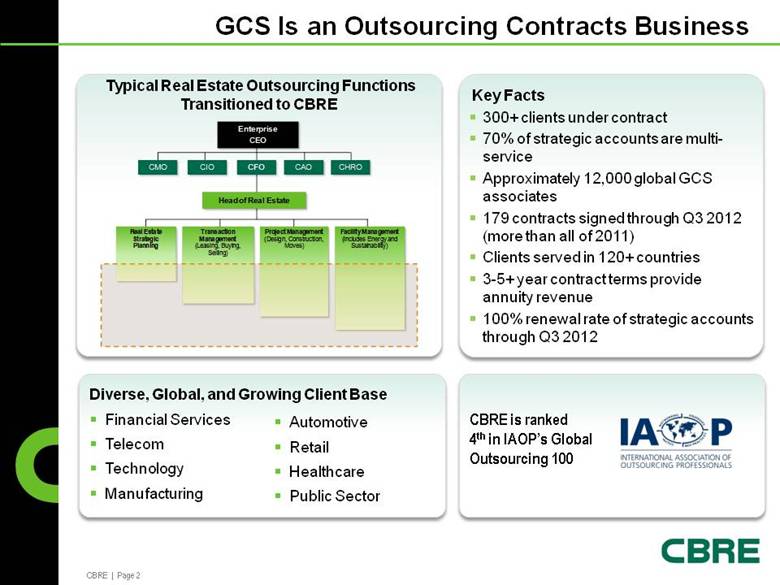

GCS Is an Outsourcing Contracts Business Ranked 4th in the IAOP Global Outsourcing 100 Key Facts 300+ clients under contract 70% of strategic accounts are multi-service Approximately 12,000 global GCS associates 179 contracts signed through Q3 2012 (more than all of 2011) Clients served in 120+ countries 3-5+ year contract terms provide annuity revenue 100% renewal rate of strategic accounts through Q3 2012 Diverse, Global, and Growing Client Base Financial Services Telecom Technology Manufacturing Automotive Retail Healthcare Public Sector CBRE is ranked 4th in IAOP’s Global Outsourcing 100 Typical Real Estate Outsourcing Functions Transitioned to CBRE Enterprise CEO Real Estate Strategic Planning Transaction Management (Leasing, Buying, Selling) Project Management (Design, Construction, Moves) Facility Management (includes Energy and Sustainability) Head of Real Estate CMO CHRO CFO CAO CIO |

|

|

SF Under Management* # of GCS Contracts Signed in BSF *Includes property management and facilities management clients; does not include affiliates. 88 179 173 121 YTD Q3 2012 Q3 2012 GCS Is a Growth Business “The GCS market is large and structurally attractive and still relatively underpenetrated.” – McKinsey and Associates 0 50 100 150 200 2009 2010 2011 YTD Q3 2012 31 25 32 88 34 25 62 121 67 45 61 173 74 35 70 179 0.0 1.0 2.0 3.0 2009 2010 2011 Q3 2012 2.2 2.6 2.9 3.0 |

|

|

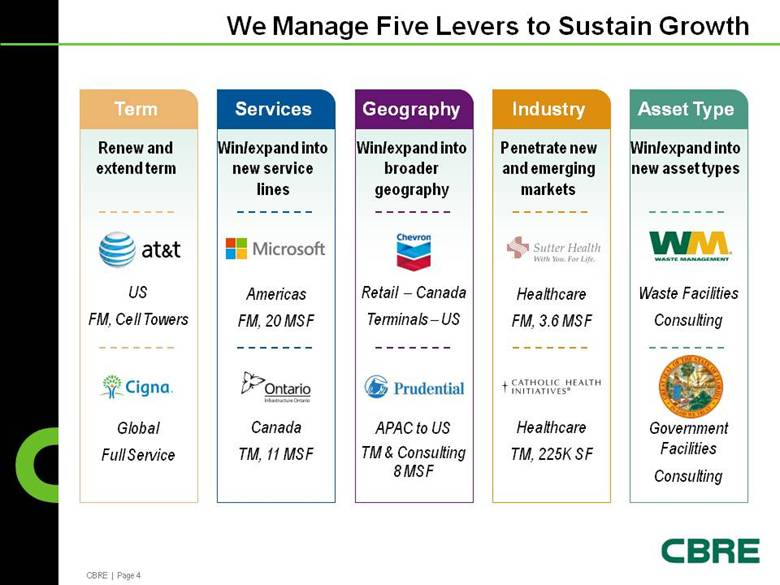

We Manage Five Levers to Sustain Growth Renew and extend term Term Win/expand into new service lines Services Win/expand into broader geography Geography Penetrate new and emerging markets Industry Win/expand into new asset types Asset Type US FM, Cell Towers Global Full Service Retail – Canada Terminals – US Canada TM, 11 MSF Americas FM, 20 MSF APAC to US TM & Consulting 8 MSF Healthcare FM, 3.6 MSF Healthcare TM, 225K SF Government Facilities Consulting Waste Facilities Consulting |

|

|

Outsourcing Expertise Consulting Expertise Improved Outcomes Corporate Sector Trends We Lead with Expertise to Help Clients Respond to a Changing Business Landscape Economic Uncertainty Centralization & Globalization Technology & Mobility Access to Talent Reducing Fixed Costs Portfolio Flexibility Speed to Market Competitive Advantage Execution Certainty Facility Management Transaction Management Project Management Portfolio Management Expense Reduction and Monetization Strategies Real Estate Organization Design & Portfolio Optimization Workplace Strategy Labor and Location Analytics |

|

|

Sector Spotlight: Momentum in Healthcare Rising Cost of Healthcare Regulatory Change Demographic Shifts Hospital System Consolidation CBRE Growth in Acute Care Hospitals 0 Q3 2012 Growth in Hospital Beds Managed by CBRE 0 Q3 2012 60 50 40 30 20 10 0 2010 2011 Q3 2012 25 33 51 0 4,000 8,000 12,000 2010 2011 Q3 2012 6,267 7,326 9,836 |

|

|

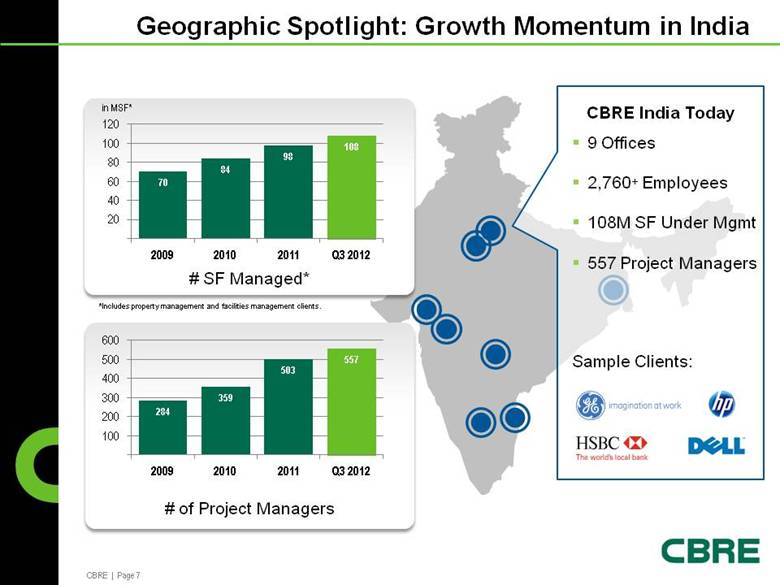

Geographic Spotlight: Growth Momentum in India # SF Managed* in MSF* CBRE India Today 9 Offices 2,760+ Employees 108M SF Under Mgmt 557 Project Managers Sample Clients: # of Project Managers *Includes property management and facilities management clients. in MSF* 20 40 60 80 100 120 2009 2010 2011 Q3 2012 70 84 98 108 100 200 300 400 500 600 2009 2010 2011 Q3 2012 284 359 503 557 |

|

|

CRE Centralization Supply Chain Rationalization Emerging Markets & Sectors *Source: McKinsey & Co. GCS Estimated Market Size and Potential* $50B Market Attributes Remain Favorable for Continued Growth |

|

|

Drive growth through sustaining satisfaction and identifying new points of entry with existing clients Continue investing in GCS platform to ensure capacity (consulting practice, technology, energy, sourcing, etc) Accelerate portfolio momentum by targeting attractive vertical markets and focusing on global growth Enhance our industry leadership position Key Strategic Priorities for 2013 |