Exhibit 99.6

|

|

Americas Business Overview Mike Lafitte President, The Americas |

Exhibit 99.6

|

|

Americas Business Overview Mike Lafitte President, The Americas |

|

|

2010 Americas Corporate Stats Total Transaction Value $73.7 billion Property Sales (# of Transactions) 4,350 Property Sales (Transaction Value) $29.8 billion Property Leasing (# of Transactions) 30,975 Property Leasing (Transaction Value) $43.9 billion Valuation and Advisory Assignments 31,525 Loan Originations $14.5 billion Loan Servicing $112.7 billion(1) Property & Corporate Facilities Under Management 1.45 billion sq. ft.(2) Project Management Contract Value $9.9 billion (1) Reflects loans serviced by GEMSA, a joint venture between CBRE Capital Markets and GE Capital Real Estate (2) Includes affiliate offices Unique Breadth and Depth |

|

|

Revenue by Region Full Year 2007 Q3 2011 YTD Canada: 23 owned offices and 1 affiliate Advisory and Outsourcing revenue at record pace in 2011 Latin America: Owned offices in Brazil, Chile and Mexico; affiliates in 4 other countries Substantial growth in Brazil and Chile Growing GCS portfolio Key Facts US All Other Regions |

|

|

San Francisco Sao Paulo Seattle Toronto Washington, DC Biotech Business Services Financial Services Law Firms Technology Automotive Business Services Financial Services Telecommunications Textiles Aerospace Business Services Healthcare Technology Consulting Financial Services Government Insurance Law Firms Federal Government Financial Services Government Contractors Law Firms Non-profits / Associations Top Cities Atlanta Chicago Dallas Los Angeles New York Business Services Education Government Healthcare Leisure & Hospitality Transportation Utilities Education Financial Services Healthcare Retail Technology Business Services Healthcare Logistics & Trade Technology Education Entertainment Government Healthcare/Hospitals Law Firms Entertainment Financial Services Law Firms Publishing |

|

|

Americas Revenue by Service Line 2007 Q3 2011 YTD Leasing Sales Property and Facilities Management Commercial Mortgage Brokerage Appraisal and Valuation Other |

|

|

Americas Trends Leasing: Leasing activity has maintained solid growth despite sluggish economy Vacancy remains historically high Rental growth has been modest Capital Markets: Recovery of investment activity has continued with availability of low-priced capital. Commercial real estate ownership as an asset class is attractive Pricing stable in core markets Private and institutional capital gravitates toward core markets Ample debt available from life companies, banks and GSE’s (CMBS market in flux) Appraisal and Valuation: Portfolio assignments are increasing; stress in secondary markets creating workout opportunities Asset Services: High vacancy pressures owners to increase efficiencies to improve ROI Industrial portfolios have been largest outsourcing deals brought to market |

|

|

Results Sustaining strong growth in spite of sub-par economic recovery Gross revenue up 17% and 19%, Q3 2011 and YTD Q3 2011, respectively All service lines growing YTD by double digits Taking advantage of capital markets recovery Property sales revenue up 49% YTD Q3 2011 #1 investment sales market share (14.3%) YTD Q3 2011 (RCA) Commercial mortgage brokerage revenue up 47% YTD Q3 2011 Outsourcing strength continues Property and Facilities Management revenue up 13% YTD Q3 2011 Canada and Latin America making increased contributions |

|

|

Americas Strategic Priorities Lead the industry (by revenue and margin) in the top markets Invest in our people to enable best-in-class client service Grow and integrate Global Asset Services Grow and integrate Global Corporate Services Invest in enhancing our Shared Services systems and platform |

|

|

People and Platform MarketView Reports Special Reports Global In-Sights Video Podcast Mapping and Demographics Labor Analytic and Economic Incentives Groups Robust Technology Global LaborView CBRE for iPhone The Best People in the Business Training For All Levels of Professional Development Active Social Media Presence Industry Leading Research and Consulting Insight Client Portal Global In-Sights U.S. Real Estate Outlook CBRE |

|

|

Property Leasing Services 1 As of December 31, 2010. Does not include affiliate offices. Approximately 2,6001 leasing professionals in the Americas Tailored service delivery by property type and industry/market specialization $43.9 billion in Americas lease transactions in 2010 Despite a sluggish economy, the leasing market posted solid growth through Q3 2011 YTD. Key Facts Major 2011 Transactions 1,100,000 sq. ft. Boston 1,050,000 sq. ft. New York 540,000 sq. ft. New York (suburbs) 250,000 sq. ft. Tampa 218,000 sq. ft. Chicago 180,000 sq. ft. Toronto Percent of Q3 2011 YTD Americas Revenue 33% |

|

|

Top 5 Manhattan Brokerage Firms Source: Crain’s New York Business, February 14, 2011. 0 1 2 3 4 5 6 CBRE Cushman & Wakefield Newmark Jones Lang LaSalle Studley Number of Deals Sq. Ft. in millions 4.8 23 3.0 17 1.4 10 1.2 5 1.1 6 Sq. Ft. in millions Number of Deals 0 5 10 15 20 25 30 35 40 45 50 2010 Leasing Activity; Top 50 Transactions |

|

|

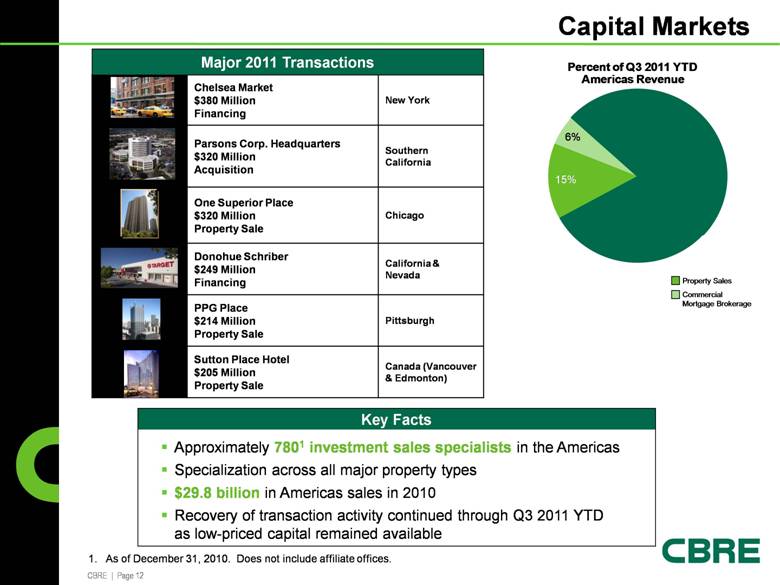

Capital Markets 1. As of December 31, 2010. Does not include affiliate offices. Key Facts Approximately 7801 investment sales specialists in the Americas Specialization across all major property types $29.8 billion in Americas sales in 2010 Recovery of transaction activity continued through Q3 2011 YTD as low-priced capital remained available Chelsea Market $380 Million Financing New York Parsons Corp. Headquarters $320 Million Acquisition Southern California One Superior Place $320 Million Property Sale Chicago Donohue Schriber $249 Million Financing California & Nevada PPG Place $214 Million Property Sale Pittsburgh Sutton Place Hotel $205 Million Property Sale Canada (Vancouver & Edmonton) Major 2011 Transactions 15% 6% Property Sales Commercial Mortgage Brokerage Percent of Q3 2011 YTD Americas Revenue |

|

|

Top 5 U.S. Investment Sales Firms Source: Real Capital Analytics, October 2011. 772 286 194 265 167 0 5 10 15 20 25 CBRE Eastdil HFF Cushman & Wakefield Jones Lang LaSalle Total Properties Sold Total Volume in $ billions 20.0 13.4 8.3 6.8 6.3 Total Volume in $ billions Total Properties Sold 0 100 300 500 700 900 1100 1300 1500 |

|

|

Top 5 U.S. Financial Intermediaries Volume in $ billions Source: NREI “Top Lenders” Survey, May 2011* *Includes loan sales volume, which was left out of NREI survey as published. |

|

|

Capital Markets Distressed Deal Volume NPI Total Returns Summary – Retail Catches up to Apartments Q3 2011 1 Year 3 Year 15 Year Since Inception Apartment 3.60 18.58 -.11 9.35 8.66 Industrial 3.39 15.41 -2.64 9.34 9.23 Office 2.96 15.33 -3.09 9.51 8.30 Retail 3.58 15.30 1.13 9.92 9.43 Total 3.30 16.10 -1.45 9.39 9.03 Source: The National Council of Real Estate Investment Fiduciaries (NCREIF) and CBRE Research, as of Q3 2011 U.S. Commercial & Multifamily Outstanding Total $2.4 Trillion Source: Mortgage Bankers Association 2Q 2011 Source: Real Capital Analytics, Troubled Asset Radar as of September 30, 2011 0 20 40 60 80 100 120 140 160 180 200 220 240 260 280 300 320 340 360 Troubled Lender REO Restructured/Extended Resolved |

|

|

Appraisal and Valuation Services Largest Clients Number of Americas Appraisals Largest Corporate Clients Largest Special Servicer Clients 19,800 25,000 30,725 30,425 30,150 31,525 0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 2005 2006 2007 2008 2009 2010 Number of Properties Appraised 4% Percent of Q3 2011 YTD Americas Revenue |

|

|

Asset Services Top U.S. Asset Services Clients 1. Represents combined data for CBRE and Trammell Crow Company for Facilities Management and Asset Services. Includes affiliate company portfolios. 2. Revenue includes property management, facilities management and project management fees for Global Corporate Services and Asset Services. Does not include transaction revenue associated with outsourcing activities. Americas Square Footage Managed1 (SF in Billions) 2 41% Percent of Q3 2011 YTD Americas Revenue 2 |