Exhibit 99.4

|

|

EMEA Business Review Michael Strong President, EMEA |

Exhibit 99.4

|

|

EMEA Business Review Michael Strong President, EMEA |

|

|

2010 EMEA Corporate Stats Total Transaction Value $33.5 billion Property Sales (# of Transactions) 1,900 Property Sales (Transaction Value) $18.9 billion Property Leasing (# of Transactions) 5,125 Property Leasing (Transaction Value) $14.6 billion Valuation & Advisory Assignments 64,025 Loan Originations $1.2 billion* Loan Servicing $10.4 billion Property & Corporate Facilities Under Management 0.5 billion sq ft** Project Management Contract Value $1.1 billion * Includes loan sale advisory ** Includes affiliate offices |

|

|

EMEA Geographic Diversification Revenue Q3 2011 YTD 2007 UK France Spain/Portugal Germany Benelux Italy Russia CEE Ireland Other |

|

|

EMEA Revenue By Service Line Q3 2011 YTD Sales 18% Lease 36% Appraisal and Valuation 11% Other 2% Property and Facilities Management 33% Sales 35% Lease 32% Appraisal and Valuation 12% Other 2% Property and Facilities Management 19% 2007 |

|

|

EMEA Economic Trends Eurozone issues remain Low levels of economic growth in short term Structural deficits in southern Europe Paradoxically, our market dynamics are positive |

|

|

EMEA Investment (€m) 0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Rest of market CBRE |

|

|

EMEA Trends Capital Markets are showing resilience The “case for property” increasingly compelling Prime office, retail and logistics continue to attract capital Secondary sector remains weak (where we have very little exposure) Leasing Demand for grade A office and retail space remains solid, and rental levels are stable or rising Lack of development funding Minimal new supply of office development sustaining rental and capital values Intermediation levels still low in most countries across EMEA The outsourcing trend continues Significant new Global Corporate Services mandates, renewals, and expansions Cross border Property and Asset Management (PAM) contracts gathering momentum |

|

|

2011 Results Despite the economic environment, significant growth achieved Gross revenues up 28% and 18%, Q3 and YTD, respectively All service lines recording growth Significant market share gains recorded Leasing: maintained number one position in London (20%)* Outsourcing has increased materially (+26% YTD Q3 2011) Strategic acquisitions enhance EMEA platform Acquired EMCM (shopping centre property management) in Central and Eastern Europe in Q2 Acquired affiliate in Switzerland in Q2 Acquired Michael Peddar (luxury retail) in UK in Q3 Acquired SCM (shopping centre property management) in The Netherlands in Q3 *Source: EGI-London Offices Market Analysis, www.egi.co.uk |

|

|

EMEA Priorities Continued focus on leadership and growth in strategic service lines Manage business mix to retain superior margins Focus on costs Process re-engineering in GCS, PAM, FM Target high margin areas (ex. Real Estate Finance) Absolute focus on market leadership by any metric |

|

|

Notable Transactions Crown Estate / Regent St London Sale of 25% stake to Norges Bank 150 year ground lease - $750M White Tower CMBS Loan work-out $1.76B recovery culminating in sale of Aviva Tower |

|

|

Notable Transactions PRUPIM Property Management Outsourcing 800 properties, 45 million sq ft, $17B value OpernTurm Sale mandate of 732,000 sq ft prime office space in Frankfurt Single largest sale in Germany in 2011 |

|

|

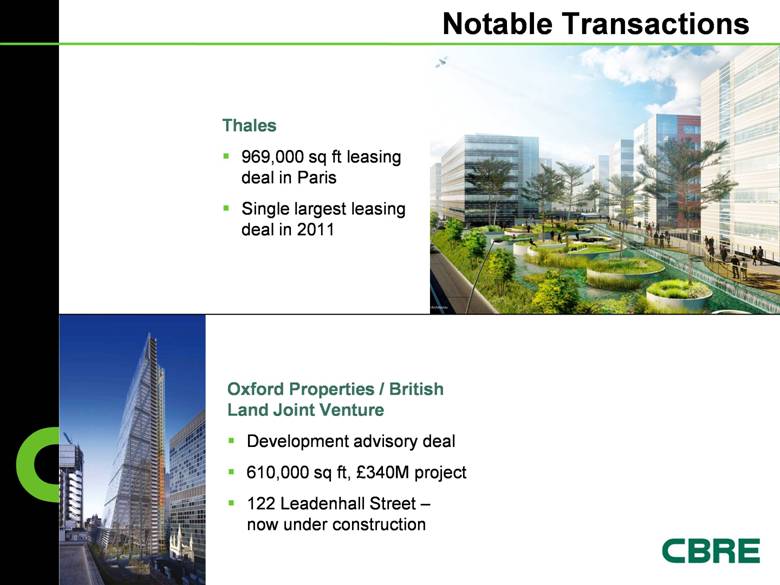

Notable Transactions Thales 969,000 sq ft leasing deal in Paris Single largest leasing deal in 2011 Oxford Properties / British Land Joint Venture Development advisory deal 610,000 sq ft, £340M project 122 Leadenhall Street – now under construction |

|

|

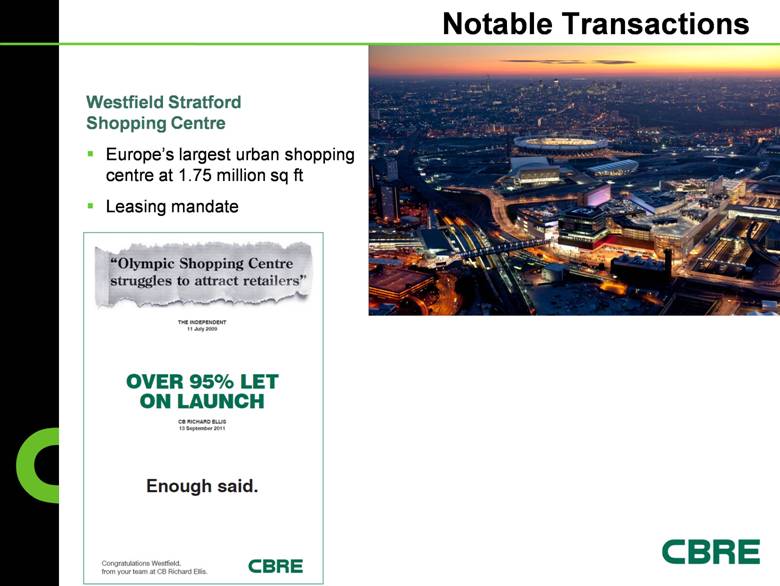

Notable Transactions Westfield Stratford Shopping Centre Europe’s largest urban shopping centre at 1.75 million sq ft Leasing mandate |