Exhibit 99.1

|

|

Investor Presentation August 2008 CB Richard Ellis Group, Inc. |

Exhibit 99.1

|

|

Investor Presentation August 2008 CB Richard Ellis Group, Inc. |

|

|

CB Richard Ellis | Page 2 Forward Looking Statements This presentation contains statements that are forward looking within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding our momentum in and possible scenarios for 2008 and 2009, future operations, future expenses, and future financial performance. These statements should be considered as estimates only and actual results may ultimately differ from these estimates. Except to the extent required by applicable securities laws, we undertake no obligation to update or publicly revise any of the forward-looking statements that you may hear today. Please refer to our current annual report on Form 10-K (in particular, Risk Factors) and our current quarterly report on Form 10-Q, which are filed with the SEC and available at the SEC’s website (http://www.sec.gov), for a full discussion of the risks and other factors that may impact any estimates that you may hear today. We may make certain statements during the course of this presentation which include references to “non-GAAP financial measures,” as defined by SEC regulations. As required by these regulations, we have provided reconciliations of these measures to what we believe are the most directly comparable GAAP measures, which are attached hereto within the appendix. |

|

|

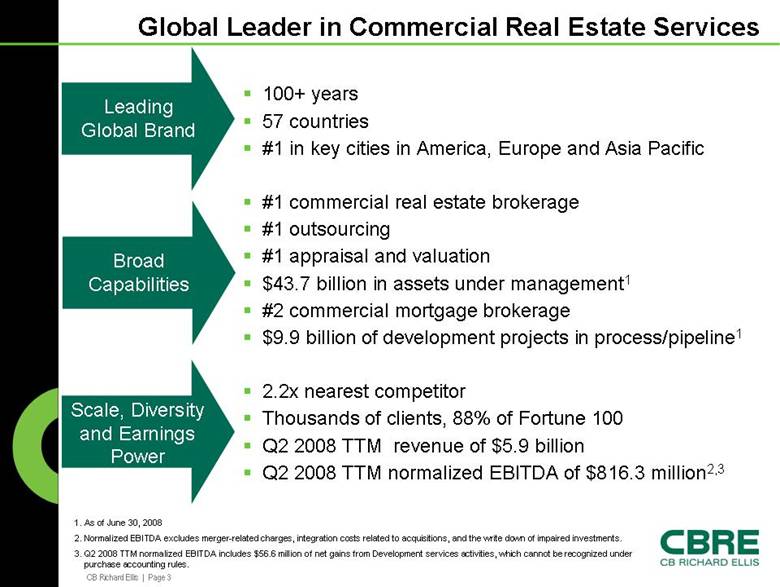

CB Richard Ellis | Page 3 Global Leader in Commercial Real Estate Services 100+ years 57 countries #1 in key cities in America, Europe and Asia Pacific #1 commercial real estate brokerage #1 outsourcing #1 appraisal and valuation $43.7 billion in assets under management1 #2 commercial mortgage brokerage $9.9 billion of development projects in process/pipeline1 2.2x nearest competitor Thousands of clients, 88% of Fortune 100 Q2 2008 TTM revenue of $5.9 billion Q2 2008 TTM normalized EBITDA of $816.3 million2,3 Leading Global Brand Broad Capabilities Scale, Diversity and Earnings Power 1. As of June 30, 2008 2. Normalized EBITDA excludes merger-related charges, integration costs related to acquisitions, and the write down of impaired investments. 3. Q2 2008 TTM normalized EBITDA includes $56.6 million of net gains from Development services activities, which cannot be recognized under purchase accounting rules. |

|

|

CB Richard Ellis | Page 4 2008 Milestones One of the world’s leading outsourcing companies #1 brand for seven consecutive years World’s Most Powerful Brokerage Firm World’s Top Brokerage and Property Management Firm #1 Brokerage and Capital Markets Firm U.S. EPA 2008 ENERGY STAR Partner of the Year Property Advisor of the Year First commercial real estate services company in the Fortune 500; Ranked #404 Ranked #11 among 50 “Best-in-Class” companies Named to “Companies that Care” 2008 Honor Roll |

|

|

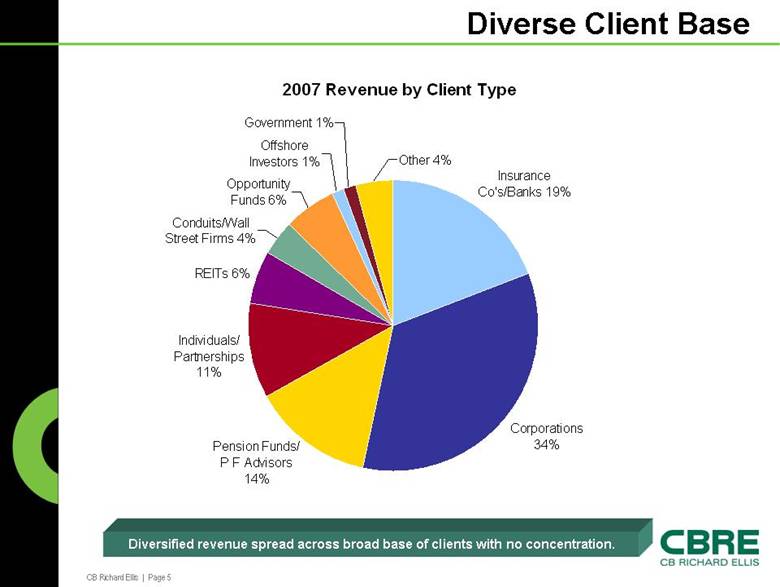

CB Richard Ellis | Page 5 Diverse Client Base 2007 Revenue by Client Type Corporations 34% Individuals/ Partnerships 11% REITs 6% Conduits/Wall Street Firms 4% Opportunity Funds 6% Offshore Investors 1% Pension Funds/ P F Advisors 14% Insurance Co's/Banks 19% Other 4% Government 1% Diversified revenue spread across broad base of clients with no concentration. |

|

|

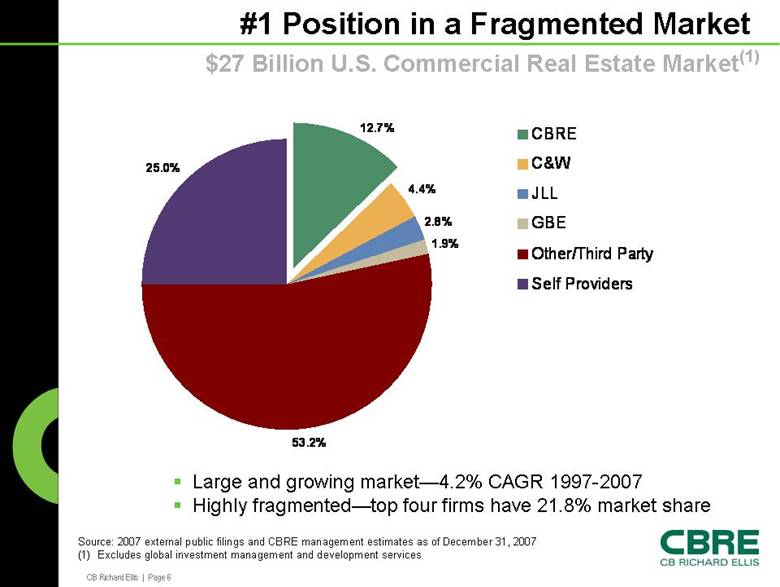

CB Richard Ellis | Page 6 #1 Position in a Fragmented Market 4.4% 2.8% 1.9% 53.2% 25.0% 12.7% CBRE C&W JLL GBE Other/Third Party Self Providers $27 Billion U.S. Commercial Real Estate Market(1) Large and growing market—4.2% CAGR 1997-2007 Highly fragmented—top four firms have 21.8% market share Source: 2007 external public filings and CBRE management estimates as of December 31, 2007 (1) Excludes global investment management and development services |

|

|

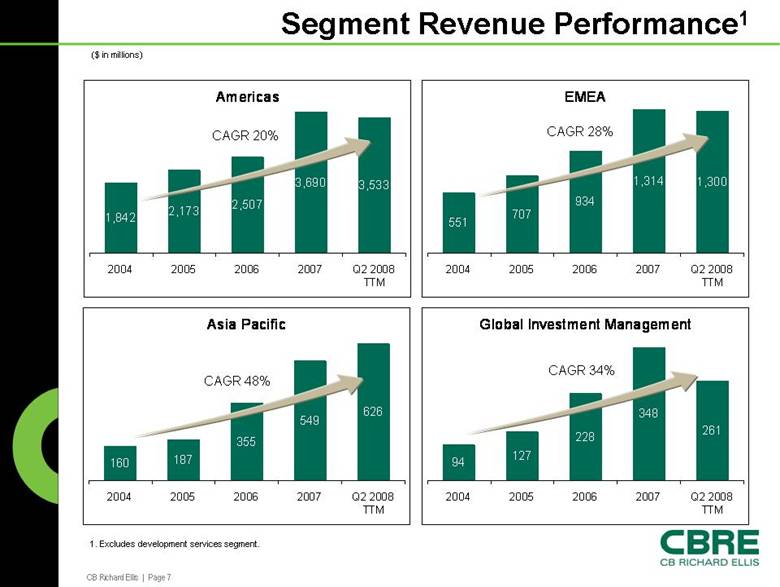

CB Richard Ellis | Page 7 Segment Revenue Performance1 Americas 1,842 2,173 2,507 3,690 3,533 2004 2005 2006 2007 Q2 2008 TTM EMEA 551 707 934 1,314 1,300 2004 2005 2006 2007 Q2 2008 TTM Global Investment Management 94 127 228 348 261 2004 2005 2006 2007 Q2 2008 TTM Asia Pacific 160 187 355 549 626 2004 2005 2006 2007 Q2 2008 TTM CAGR 34% CAGR 20% CAGR 28% CAGR 48% 1. Excludes development services segment. ($ in millions) |

|

|

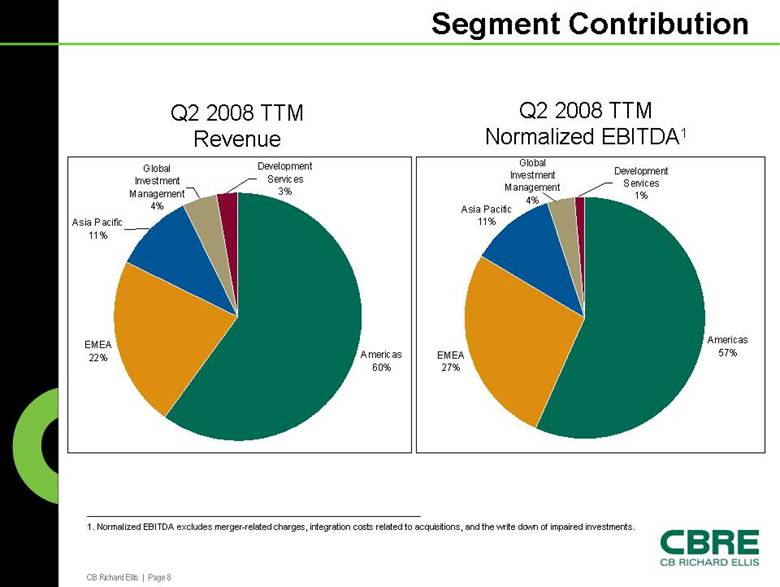

CB Richard Ellis | Page 8 Segment Contribution Q2 2008 TTM Revenue Q2 2008 TTM Normalized EBITDA1 1. Normalized EBITDA excludes merger-related charges, integration costs related to acquisitions, and the write down of impaired investments. Americas 60% EMEA 22% Development Services 3% Global Investment Management 4% Asia Pacific 11% Americas 57% EMEA 27% Development Services 1% Global Investment Management 4% Asia Pacific 11% |

|

|

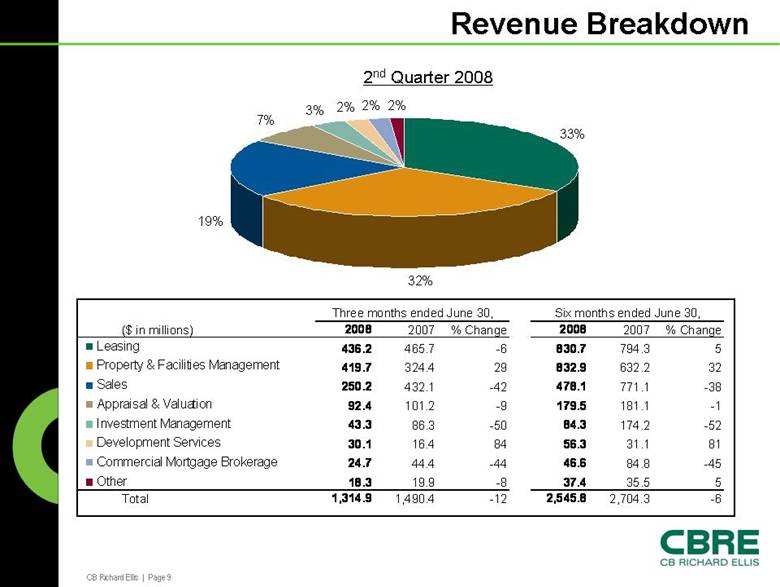

CB Richard Ellis | Page 9 32% 19% 7% 3% 2% 2% 33% 2% Leasing Property & Facilities Management Sales Appraisal & Valuation Investment Management Development Services Commercial Mortgage Brokerage Other Revenue Breakdown 2nd Quarter 2008 ($ in millions) 2008 2007 % Change 2008 2007 % Change 436.2 465.7 -6 830.7 794.3 5 419.7 324.4 29 832.9 632.2 32 250.2 432.1 -42 478.1 771.1 -38 92.4 101.2 -9 179.5 181.1 -1 43.3 86.3 -50 84.3 174.2 -52 30.1 16.4 84 56.3 31.1 81 24.7 44.4 -44 46.6 84.8 -45 18.3 19.9 -8 37.4 35.5 5 Total 1,314.9 1,490.4 -12 2,545.8 2,704.3 -6 Three months ended June 30, Six months ended June 30, |

|

|

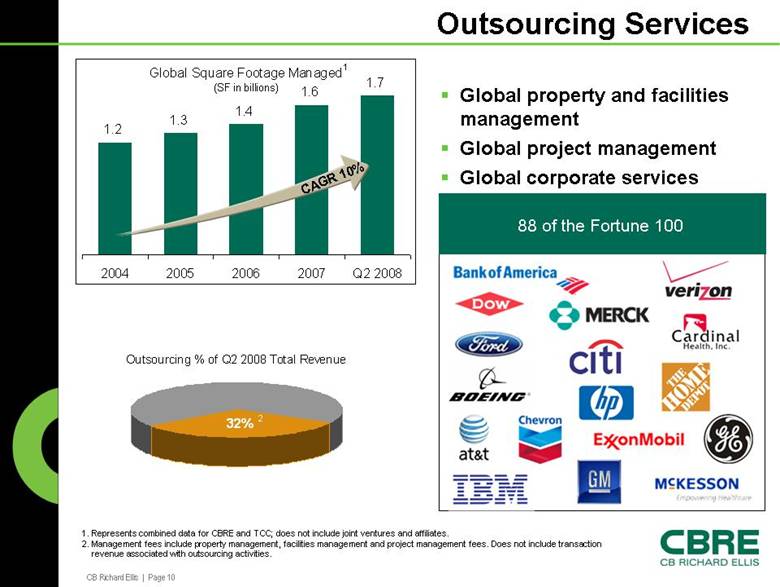

CB Richard Ellis | Page 10 Outsourcing % of Q2 2008 Total Revenue 32% Global Square Footage Managed (SF in billions) 1.2 1.3 1.4 1.6 1.7 2004 2005 2006 2007 Q2 2008 Outsourcing Services Global property and facilities management Global project management Global corporate services 1 88 of the Fortune 100 1. Represents combined data for CBRE and TCC; does not include joint ventures and affiliates. 2. Management fees include property management, facilities management and project management fees. Does not include transaction revenue associated with outsourcing activities. 2 CAGR 10% |

|

|

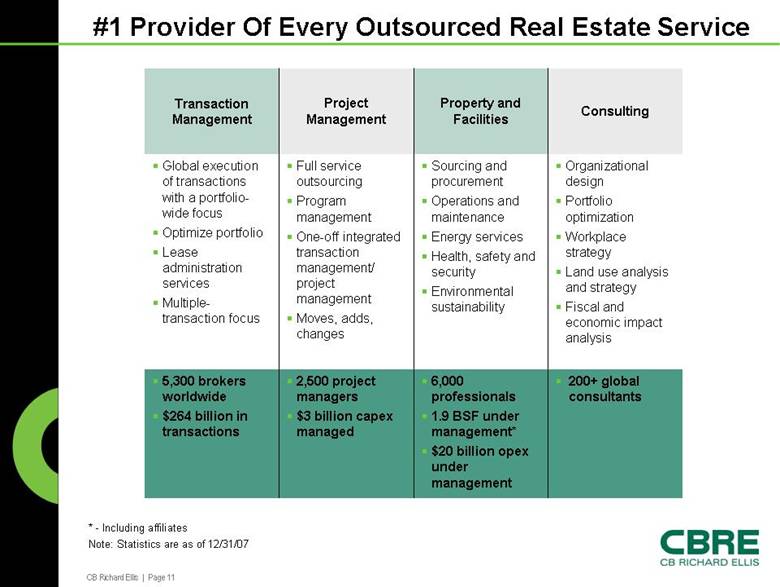

CB Richard Ellis | Page 11 #1 Provider Of Every Outsourced Real Estate Service * - Including affiliates Note: Statistics are as of 12/31/07 Transaction Management Project Management Property and Facilities Consulting Global execution of transactions with a portfoliowide focus Optimize portfolio Lease administration services Multipletransaction focus Full service outsourcing Program management One-off integrated transaction management/ project management Moves, adds, changes Sourcing and procurement Operations and maintenance Energy services Health, safety and security Environmental sustainability Organizational design Portfolio optimization Workplace strategy Land use analysis and strategy Fiscal and economic impact analysis 5,300 brokers worldwide $264 billion in transactions 2,500 project managers $3 billion capex managed 6,000 professionals 1.9 BSF under management* $20 billion opex under management 200+ global consultants |

|

|

CB Richard Ellis | Page 12 U.S. Market Stats 8.5% 9.4% 12.6% 4Q06 10.6 208.0 79.8 2006 13.7 0.1 13.3 9.9% 10.3% 9.6% Retail -31.8 -33.0 160.7 10.9% 10.3% 9.4% Industrial 0.6 5.0 56.1 14.3% 13.2% 12.6% Office 2008 F 2Q08 2007 4Q08 F 2Q08 4Q07 US Absorption Trends (in millions of square feet) US Vacancy Source: TWR Outlooks Fall 2008 – preliminary data Cap Rates Remain Steady At Lower Volumes Cap Rate Growth1 2Q07 4Q07 2Q08 2008 / 2009 F Office Volume ($B) 90.9 27.7 30.1 Cap Rate 6.4% 6.5% 6.8% +60 to120 bps Industrial Volume ($B) 24.5 9.8 12.4 Cap Rate 6.8% 7.4% 7.4% +60 to 100 bps Retail Volume ($B) 32.4 11.0 12.0 Cap Rate 6.6% 7.0% 7.0% +50 to 100 bps Source: RCA June 2008 1. TWR estimates |

|

|

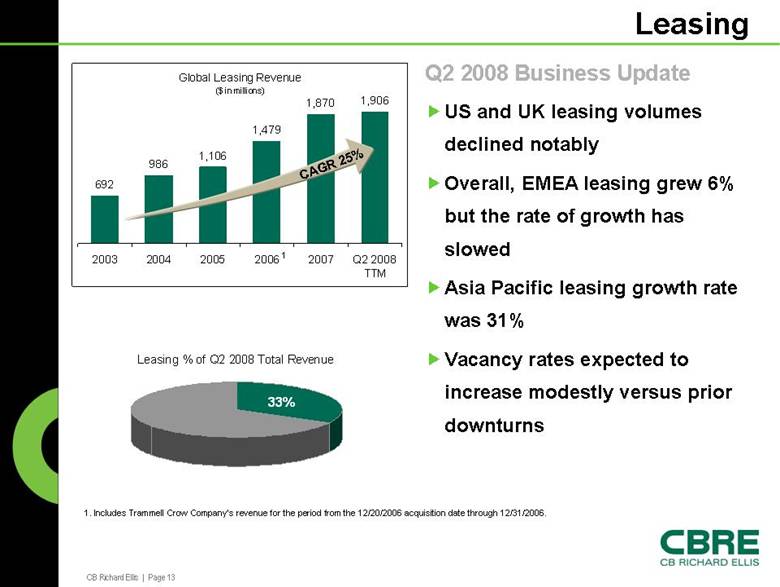

CB Richard Ellis | Page 13 Leasing Q2 2008 Business Update US and UK leasing volumes declined notably Overall, EMEA leasing grew 6% but the rate of growth has slowed Asia Pacific leasing growth rate was 31% Vacancy rates expected to increase modestly versus prior downturns Global Leasing Revenue ($ in millions) 692 986 1,106 1,479 1,870 1,906 2003 2004 2005 2006 2007 Q2 2008 TTM Leasing % of Q2 2008 Total Revenue 33% 1 1. Includes Trammell Crow Company’s revenue for the period from the 12/20/2006 acquisition date through 12/31/2006. CAGR 25% |

|

|

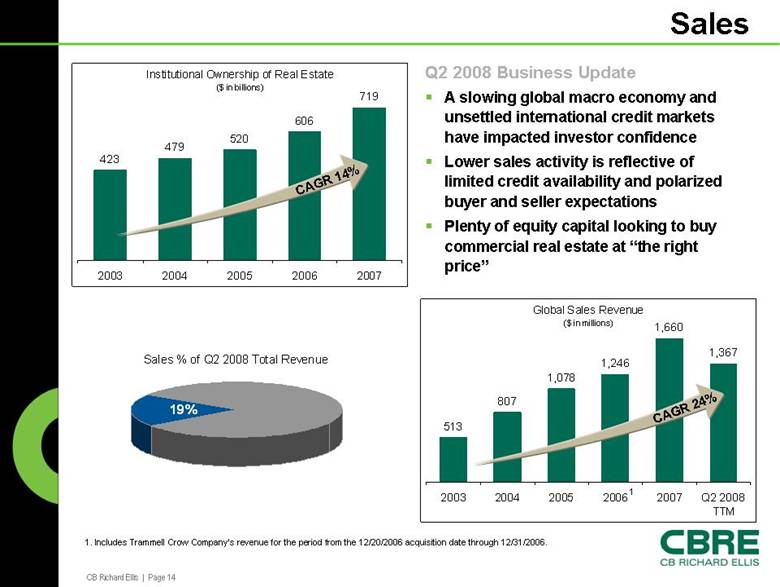

CB Richard Ellis | Page 14 Sales Q2 2008 Business Update A slowing global macro economy and unsettled international credit markets have impacted investor confidence Lower sales activity is reflective of limited credit availability and polarized buyer and seller expectations Plenty of equity capital looking to buy commercial real estate at “the right price” Global Sales Revenue ($ in millions) 513 807 1,078 1,246 1,660 1,367 2003 2004 2005 2006 2007 Q2 2008 TTM CAGR 24% 1 1. Includes Trammell Crow Company’s revenue for the period from the 12/20/2006 acquisition date through 12/31/2006. Institutional Ownership of Real Estate ($ in billions) 423 479 520 606 719 2003 2004 2005 2006 2007 CAGR 14% Sales % of Q2 2008 Total Revenue 19% |

|

|

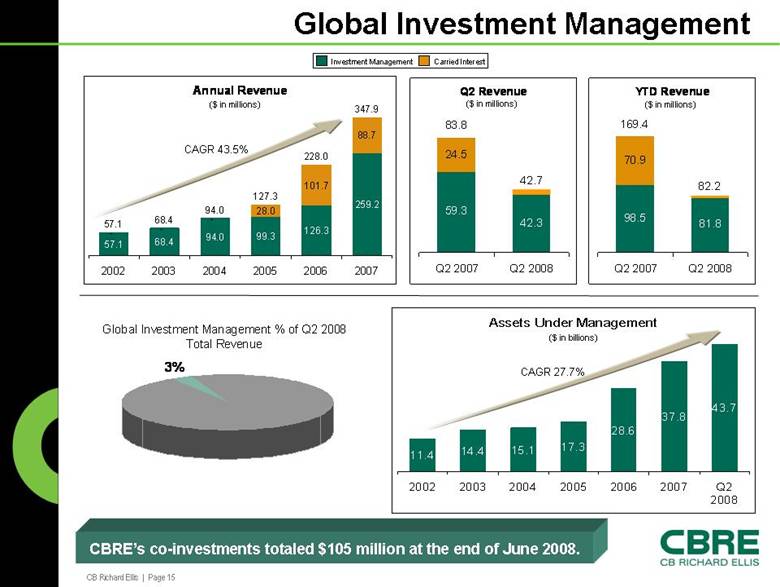

CB Richard Ellis | Page 15 Global Investment Management Annual Revenue 57.1 68.4 94.0 99.3 126.3 259.2 - - - 28.0 101.7 88.7 57.1 68.4 94.0 127.3 228.0 347.9 2002 2003 2004 2005 2006 2007 Assets Under Management 11.4 14.4 15.1 17.3 28.6 37.8 43.7 2002 2003 2004 2005 2006 2007 Q2 2008 Q2 Revenue 59.3 42.3 24.5 83.8 42.7 Q2 2007 Q2 2008 ($ in billions) Investment Management Carried Interest ($ in millions) CBRE’s co-investments totaled $105 million at the end of June 2008. CAGR 43.5% CAGR 27.7% ($ in millions) YTD Revenue 98.5 81.8 70.9 169.4 82.2 Q2 2007 Q2 2008 ($ in millions) Global Investment Management % of Q2 2008 Total Revenue 3% |

|

|

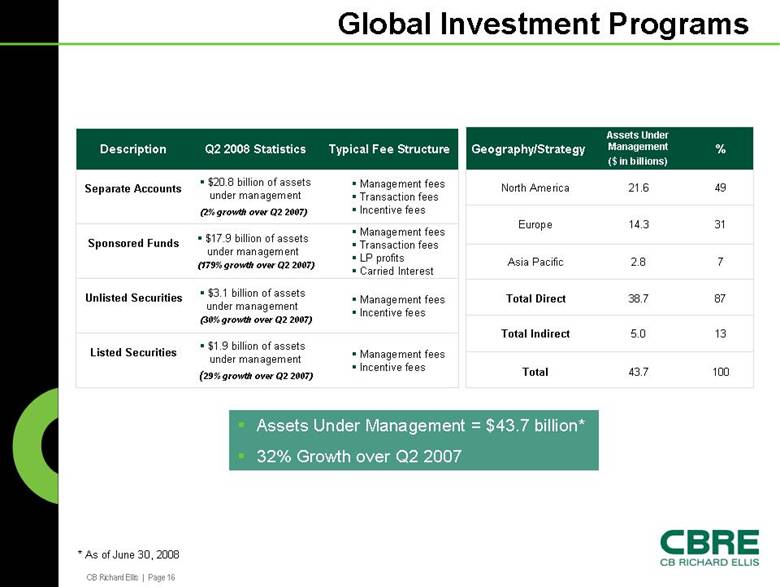

CB Richard Ellis | Page 16 Global Investment Programs Description Q2 2008 Statistics Typical Fee Structure Separate Accounts $20.8 billion of assets under management (2% growth over Q2 2007) Management fees Transaction fees Incentive fees Sponsored Funds $17.9 billion of assets under management (179% growth over Q2 2007) Management fees Transaction fees LP profits Carried Interest Unlisted Securities $3.1 billion of assets under management (30% growth over Q2 2007) Management fees Incentive fees Listed Securities $1.9 billion of assets under management (29% growth over Q2 2007) Management fees Incentive fees Geography/Strategy Assets Under Management ($ in billions) % North America 21.6 49 Europe 14.3 31 Asia Pacific 2.8 7 Total Direct 38.7 87 Total Indirect 5.0 13 Total 43.7 100 Assets Under Management = $43.7 billion* 32% Growth over Q2 2007 * As of June 30, 2008 |

|

|

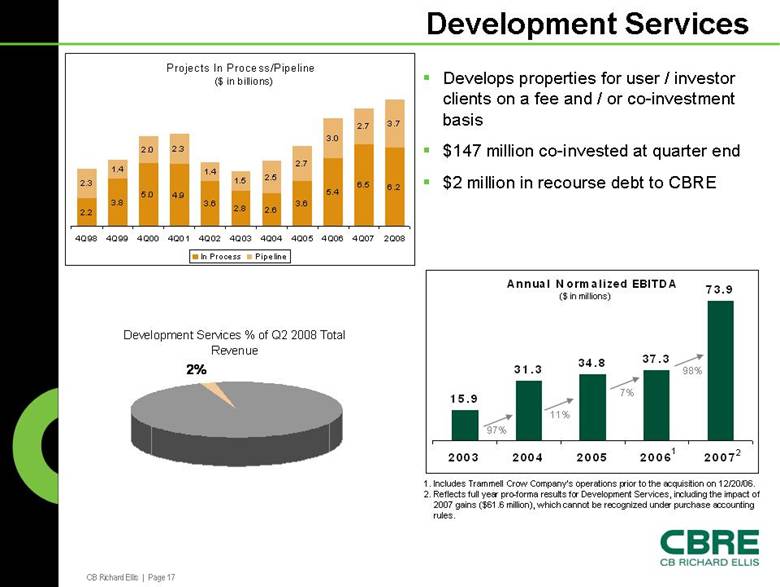

CB Richard Ellis | Page 17 Development Services Develops properties for user / investor clients on a fee and / or co-investment basis $147 million co-invested at quarter end $2 million in recourse debt to CBRE Annual N ormalized EBITDA 15.9 31.3 34.8 37.3 73.9 2003 2004 2005 2006 2007 1. Includes Trammell Crow Company’s operations prior to the acquisition on 12/20/06. 2. Reflects full year pro-forma results for Development Services, including the impact of 2007 gains ($61.6 million), which cannot be recognized under purchase accounting rules. 97% 11% 7% 98% 1 2 ($ in millions) Projects In Process/Pipeline ($ in billions) 2.2 3.8 5.0 4.9 3.6 2.8 2.6 3.6 5.4 6.5 6.2 2.3 1.4 2.0 2.3 1.4 1.5 2.5 2.7 3.0 2.7 3.7 4Q98 4Q99 4Q00 4Q01 4Q02 4Q03 4Q04 4Q05 4Q06 4Q07 2Q08 In Process Pipeline Development Services % of Q2 2008 Total Revenue 2% |

|

|

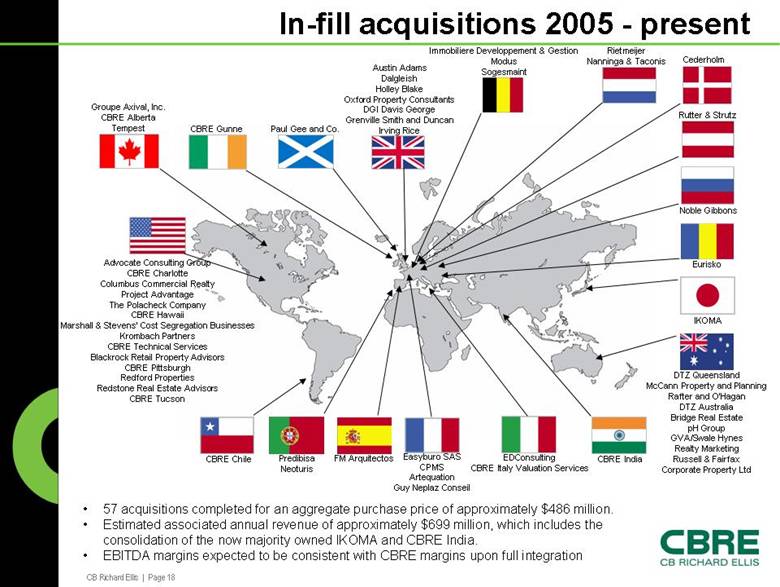

CB Richard Ellis | Page 18 In-fill acquisitions 2005 - present Groupe Axival, Inc. CBRE Alberta Tempest Advocate Consulting Group CBRE Charlotte Columbus Commercial Realty Project Advantage The Polacheck Company CBRE Hawaii Marshall & Stevens’ Cost Segregation Businesses Krombach Partners CBRE Technical Services Blackrock Retail Property Advisors CBRE Pittsburgh Redford Properties Redstone Real Estate Advisors CBRE Tucson CBRE Chile CBRE Gunne Paul Gee and Co. Austin Adams Dalgleish Holley Blake Oxford Property Consultants DGI Davis George Grenville Smith and Duncan Irving Rice Immobiliere Developpement & Gestion Modus Sogesmaint Cederholm Rietmeijer Nanninga & Taconis Rutter & Strutz Eurisko Noble Gibbons IKOMA DTZ Queensland McCann Property and Planning Rafter and O’Hagan DTZ Australia Bridge Real Estate pH Group GVA/Swale Hynes Realty Marketing Russell & Fairfax Corporate Property Ltd CBRE India EDConsulting CBRE Italy Valuation Services Easyburo SAS CPMS Artequation Guy Neplaz Conseil FM Arquitectos Predibisa Neoturis • 57 acquisitions completed for an aggregate purchase price of approximately $486 million. • Estimated associated annual revenue of approximately $699 million, which includes the consolidation of the now majority owned IKOMA and CBRE India. • EBITDA margins expected to be consistent with CBRE margins upon full integration |

|

|

CB Richard Ellis | Page 19 Financial Overview |

|

|

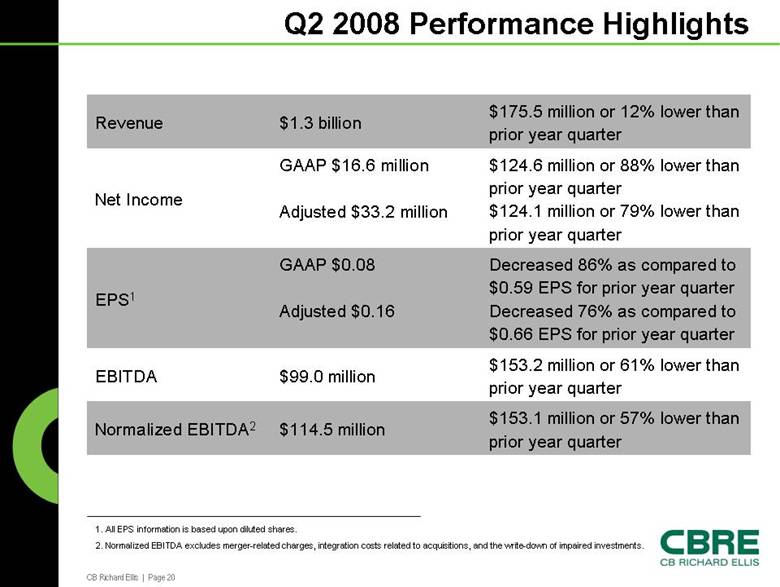

CB Richard Ellis | Page 20 Q2 2008 Performance Highlights $153.1 million or 57% lower than prior year quarter $114.5 million Normalized EBITDA2 $153.2 million or 61% lower than prior year quarter $99.0 million EBITDA Decreased 86% as compared to $0.59 EPS for prior year quarter Decreased 76% as compared to $0.66 EPS for prior year quarter GAAP $0.08 Adjusted $0.16 EPS1 $124.6 million or 88% lower than prior year quarter $124.1 million or 79% lower than prior year quarter GAAP $16.6 million Adjusted $33.2 million Net Income $175.5 million or 12% lower than prior year quarter $1.3 billion Revenue 1. All EPS information is based upon diluted shares. 2. Normalized EBITDA excludes merger-related charges, integration costs related to acquisitions, and the write-down of impaired investments. |

|

|

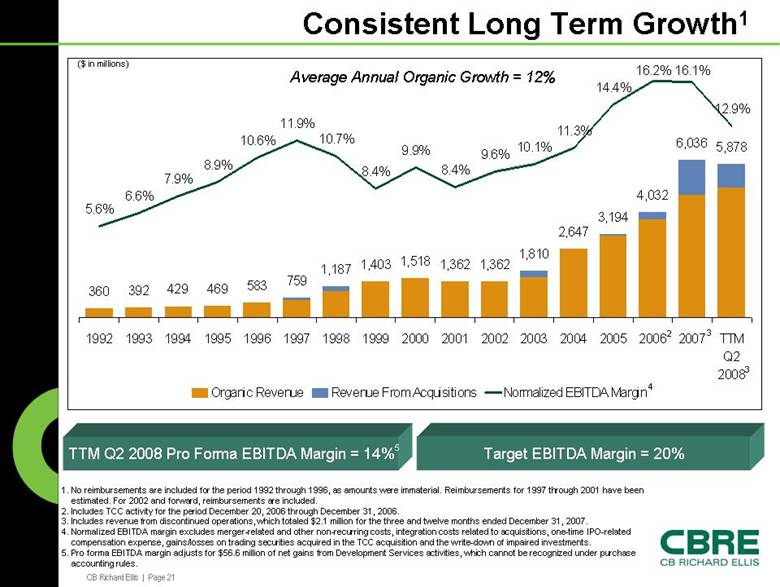

CB Richard Ellis | Page 21 5.6% 6.6% 7.9% 8.9% 10.6% 11.9% 10.7% 8.4% 9.9% 8.4% 9.6% 10.1% 11.3% 14.4% 16.2% 16.1% 12.9% 360 392 429 469 583 759 1,187 1,403 1,518 1,362 1,362 1,810 2,647 3,194 4,032 6,036 5,878 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 TTM Q2 2008 Organic Revenue Revenue From Acquisitions Normalized EBITDA Margin . Consistent Long Term Growth1 Average Annual Organic Growth = 12% ($ in millions) TTM Q2 2008 Pro Forma EBITDA Margin = 14% Target EBITDA Margin = 20% 1. No reimbursements are included for the period 1992 through 1996, as amounts were immaterial. Reimbursements for 1997 through 2001 have been estimated. For 2002 and forward, reimbursements are included. 2. Includes TCC activity for the period December 20, 2006 through December 31, 2006. 3. Includes revenue from discontinued operations, which totaled $2.1 million for the three and twelve months ended December 31, 2007. 4. Normalized EBITDA margin excludes merger-related and other non-recurring costs, integration costs related to acquisitions, one-time IPO-related compensation expense, gains/losses on trading securities acquired in the TCC acquisition and the write-down of impaired investments. 5. Pro forma EBITDA margin adjusts for $56.6 million of net gains from Development Services activities, which cannot be recognized under purchase accounting rules. 2 3 4 5 3 |

|

|

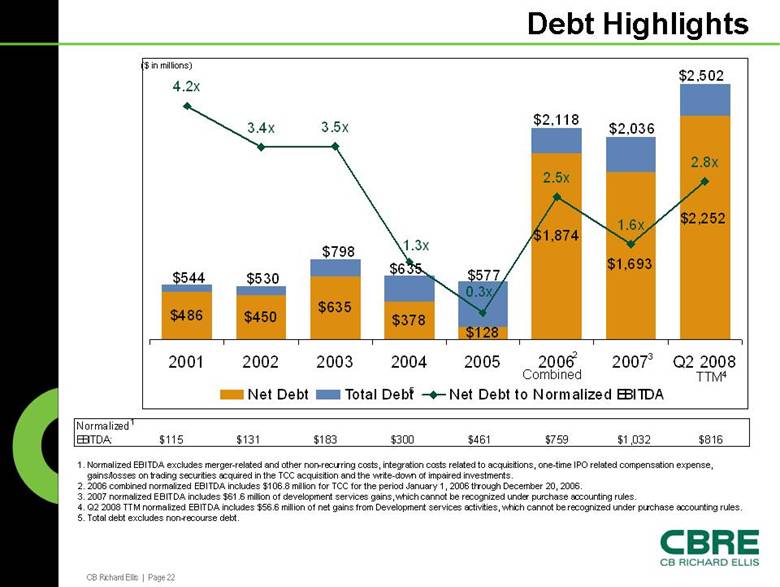

CB Richard Ellis | Page 22 $486 $450 $635 $378 $128 $2,252 $1,874 $1,693 4.2x 3.4x 3.5x 2.5x 2.8x 0.3x 1.3x 1.6x $2,502 $2,036 $2,118 $577 $635 $798 $530 $544 2001 2002 2003 2004 2005 2006 2007 Q2 2008 Net Debt Total Debt Net Debt to Normalized EBITDA . Normalized EBITDA: $115 $131 $183 $300 $461 $759 $1,032 $816 Debt Highlights 1. Normalized EBITDA excludes merger-related and other non-recurring costs, integration costs related to acquisitions, one-time IPO related compensation expense, gains/losses on trading securities acquired in the TCC acquisition and the write-down of impaired investments. 2. 2006 combined normalized EBITDA includes $106.8 million for TCC for the period January 1, 2006 through December 20, 2006. 3. 2007 normalized EBITDA includes $61.6 million of development services gains, which cannot be recognized under purchase accounting rules. 4. Q2 2008 TTM normalized EBITDA includes $56.6 million of net gains from Development services activities, which cannot be recognized under purchase accounting rules. 5. Total debt excludes non-recourse debt. ($ in millions) 1 2 3 TTM4 5 Combined |

|

|

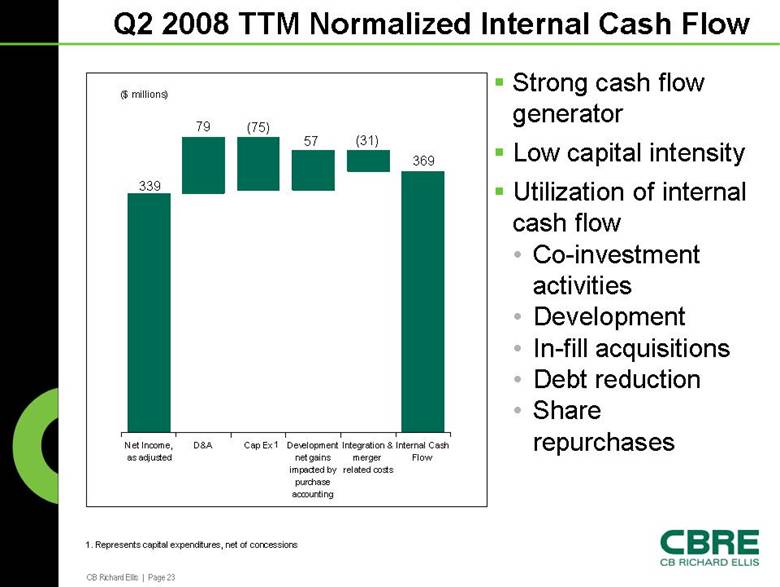

CB Richard Ellis | Page 23 Internal Cash Flow Integration & merger related costs Development net gains impacted by purchase accounting Cap Ex D&A Net Income, as adjusted ($ millions) Q2 2008 TTM Normalized Internal Cash Flow Strong cash flow generator Low capital intensity Utilization of internal cash flow • Co-investment activities • Development • In-fill acquisitions • Debt reduction • Share repurchases 339 79 (75) 57 (31) 369 1 1. Represents capital expenditures, net of concessions |

|

|

CB Richard Ellis | Page 24 Key Investment Points Uniquely positioned to succeed in tough market –Most diversified revenue base (geography and services) –Strong balance sheet –Variable cost structure –Strong cash flow generation Opportunity to gain share / grow –Cross selling –Industry consolidation –Acquisition opportunities –Attracting and retaining talent |

|

|

CB Richard Ellis | Page 25 GAAP Reconciliation Tables |

|

|

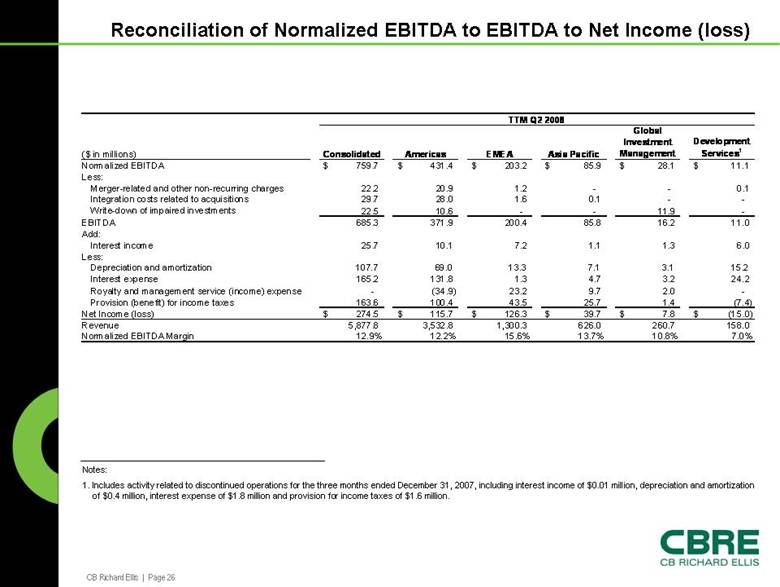

CB Richard Ellis | Page 26 Reconciliation of Normalized EBITDA to EBITDA to Net Income (loss) Notes: 1. Includes activity related to discontinued operations for the three months ended December 31, 2007, including interest income of $0.01 million, depreciation and amortization of $0.4 million, interest expense of $1.8 million and provision for income taxes of $1.6 million. ($ in millions) Consolidated Americas EMEA Asia Pacific Global Investment Management Development Services1 Normalized EBITDA 759.7 $ 431.4 $ 203.2 $ 85.9 $ 28.1 $ 11.1 $ Less: Merger-related and other non-recurring charges 22.2 20.9 1.2 - - 0.1 Integration costs related to acquisitions 29.7 28.0 1.6 0.1 - - Write-down of impaired investments 22.5 10.6 - - 11.9 - EBITDA 685.3 371.9 200.4 85.8 16.2 11.0 Add: Interest income 25.7 10.1 7.2 1.1 1.3 6.0 Less: Depreciation and amortization 107.7 69.0 13.3 7.1 3.1 15.2 Interest expense 165.2 131.8 1.3 4.7 3.2 24.2 Royalty and management service (income) expense - (34.9) 23.2 9.7 2.0 - Provision (benefit) for income taxes 163.6 100.4 43.5 25.7 1.4 (7.4) Net Income (loss) 274.5 $ 115.7 $ 126.3 $ 39.7 $ 7.8 $ (15.0) $ Revenue 5,877.8 3,532.8 1,300.3 626.0 260.7 158.0 Normalized EBITDA Margin 12.9% 12.2% 15.6% 13.7% 10.8% 7.0% TTM Q2 2008 |

|

|

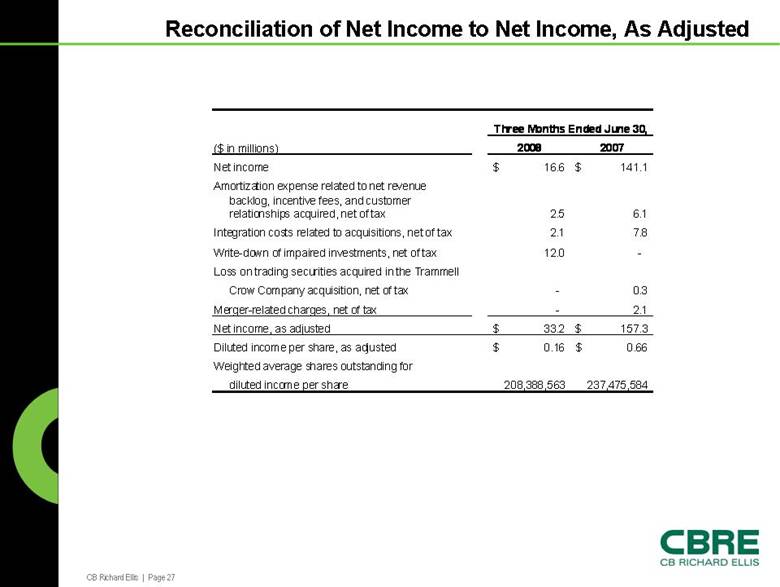

CB Richard Ellis | Page 27 Reconciliation of Net Income to Net Income, As Adjusted ($ in millions) 2008 2007 Net income 16.6 $ 141.1 $ Amortization expense related to net revenue backlog, incentive fees, and customer relationships acquired, net of tax 2.5 6.1 Integration costs related to acquisitions, net of tax 2.1 7.8 Write-down of impaired investments, net of tax 12.0 - Loss on trading securities acquired in the Trammell Crow Company acquisition, net of tax - 0.3 Merger-related charges, net of tax - 2.1 Net income, as adjusted 33.2 $ 157.3 $ Diluted income per share, as adjusted 0.16 $ 0.66 $ Weighted average shares outstanding for diluted income per share 208,388,563 237,475,584 Three Months Ended June 30, |

|

|

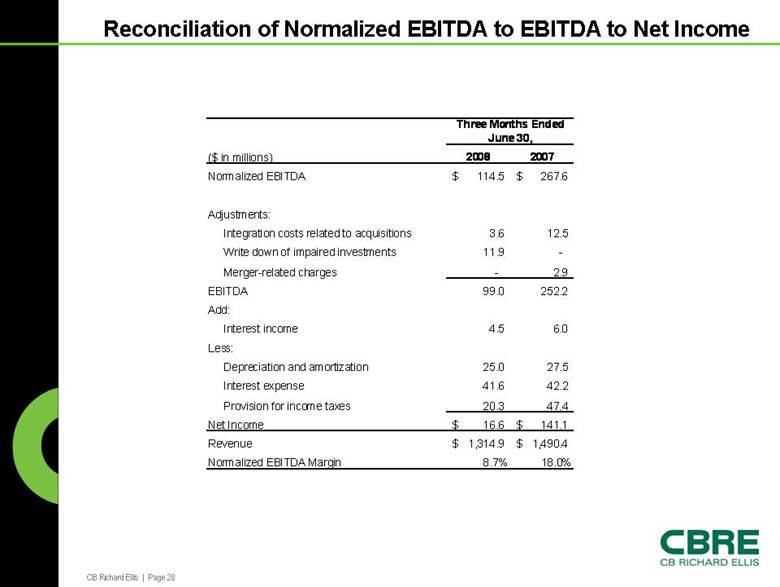

CB Richard Ellis | Page 28 Reconciliation of Normalized EBITDA to EBITDA to Net Income ($ in millions) 2008 2007 Normalized EBITDA 114.5 $ 267.6 $ Adjustments: Integration costs related to acquisitions 3.6 12.5 Write down of impaired investments 11.9 - Merger-related charges - 2.9 EBITDA 99.0 252.2 Add: Interest income 4.5 6.0 Less: Depreciation and amortization 25.0 27.5 Interest expense 41.6 42.2 Provision for income taxes 20.3 47.4 Net Income 16.6 $ 141.1 $ Revenue 1,314.9 $ 1,490.4 $ Normalized EBITDA Margin 8.7% 18.0% Three Months Ended June 30, |

|

|

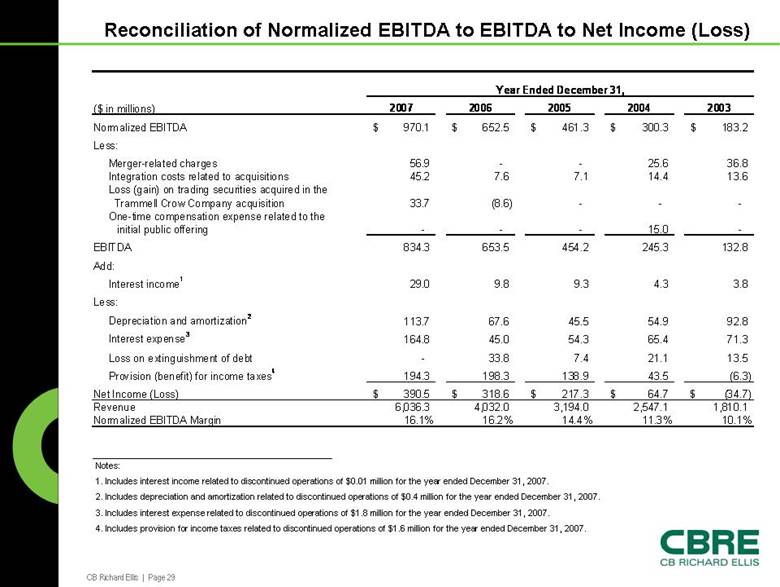

CB Richard Ellis | Page 29 Reconciliation of Normalized EBITDA to EBITDA to Net Income (Loss) Notes: 1. Includes interest income related to discontinued operations of $0.01 million for the year ended December 31, 2007. 2. Includes depreciation and amortization related to discontinued operations of $0.4 million for the year ended December 31, 2007. 3. Includes interest expense related to discontinued operations of $1.8 million for the year ended December 31, 2007. 4. Includes provision for income taxes related to discontinued operations of $1.6 million for the year ended December 31, 2007. ($ in millions) 2007 2006 2005 2004 2003 Normalized EBITDA 970.1 $ 652.5 $ 461.3 $ 300.3 $ 183.2 $ Less: Merger-related charges 56.9 - - 25.6 36.8 Integration costs related to acquisitions 45.2 7.6 7.1 14.4 13.6 Loss (gain) on trading securities acquired in the Trammell Crow Company acquisition 33.7 (8.6) - - - One-time compensation expense related to the initial public offering - - - 15.0 - EBITDA 834.3 653.5 454.2 245.3 132.8 Add: Interest income1 29.0 9.8 9.3 4.3 3.8 Less: Depreciation and amortization2 113.7 67.6 45.5 54.9 92.8 Interest expense3 164.8 45.0 54.3 65.4 71.3 Loss on extinguishment of debt - 33.8 7.4 21.1 13.5 Provision (benefit) for income taxes4 194.3 198.3 138.9 43.5 (6.3) Net Income (Loss) 390.5 $ 318.6 $ 217.3 $ 64.7 $ (34.7) $ Revenue 6,036.3 4,032.0 3,194.0 2,547.1 1,810.1 Normalized EBITDA Margin 16.1% 16.2% 14.4% 11.3% 10.1% Year Ended December 31, |

|

|

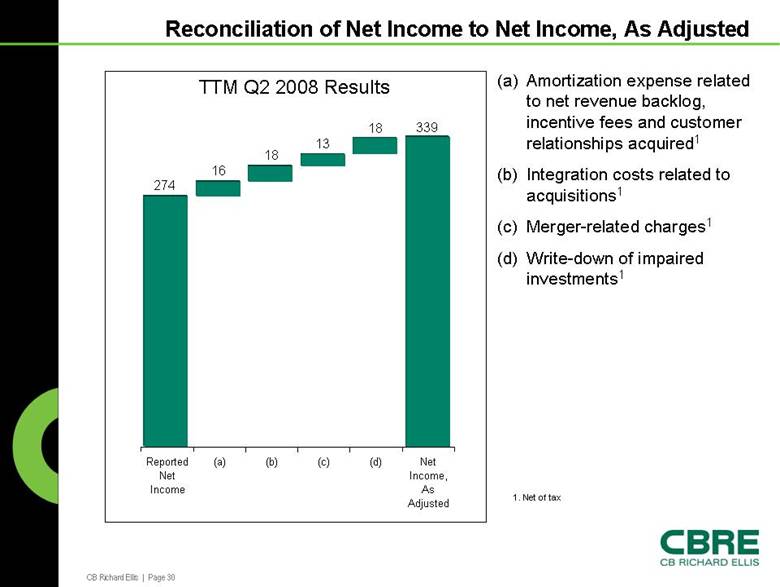

CB Richard Ellis | Page 30 Net Income, As Adjusted (d) (c) (b) (a) Reported Net Income Reconciliation of Net Income to Net Income, As Adjusted TTM Q2 2008 Results 274 16 18 13 18 339 (a) Amortization expense related to net revenue backlog, incentive fees and customer relationships acquired1 (b) Integration costs related to acquisitions1 (c) Merger-related charges1 (d) Write-down of impaired investments1 1. Net of tax |