Exhibit 99.2

|

|

Second Quarter 2008 Earnings Conference Call July 30, 2008 CB Richard Ellis Group, Inc. |

Exhibit 99.2

|

|

Second Quarter 2008 Earnings Conference Call July 30, 2008 CB Richard Ellis Group, Inc. |

|

|

CB Richard Ellis | Page 2 Forward Looking Statements This presentation contains statements that are forward looking within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding our momentum in and possible scenarios for 2008 and 2009, future operations, future expenses, and future financial performance. These statements should be considered as estimates only and actual results may ultimately differ from these estimates. Except to the extent required by applicable securities laws, we undertake no obligation to update or publicly revise any of the forward-looking statements that you may hear today. Please refer to our current annual report on Form 10-K (in particular, Risk Factors) and our current quarterly report on Form 10-Q, which are filed with the SEC and available at the SEC’s website (http://www.sec.gov), for a full discussion of the risks and other factors that may impact any estimates that you may hear today. We may make certain statements during the course of this presentation which include references to “non-GAAP financial measures,” as defined by SEC regulations. As required by these regulations, we have provided reconciliations of these measures to what we believe are the most directly comparable GAAP measures, which are attached hereto within the appendix. |

|

|

CB Richard Ellis | Page 3 Conference Call Participants Brett White President & Chief Executive Officer Kenneth J. Kay Senior Executive Vice President & Chief Financial Officer Ray Torto Global Chief Economist Nick Kormeluk Senior Vice President, Investor Relations |

|

|

CB Richard Ellis | Page 4 Business Overview Second quarter significantly impacted by credit crisis and economic decline What’s the same • Outsourcing continues to perform very well • We continue to gain market share • We remained aggressive in M&A • Continued growth in assets under management to $43.7 billion at June 30, 2008 What’s new • Global capital markets have deteriorated further • US leasing markets weakened materially in May and June • EMEA and Asia Pacific leasing also slowed |

|

|

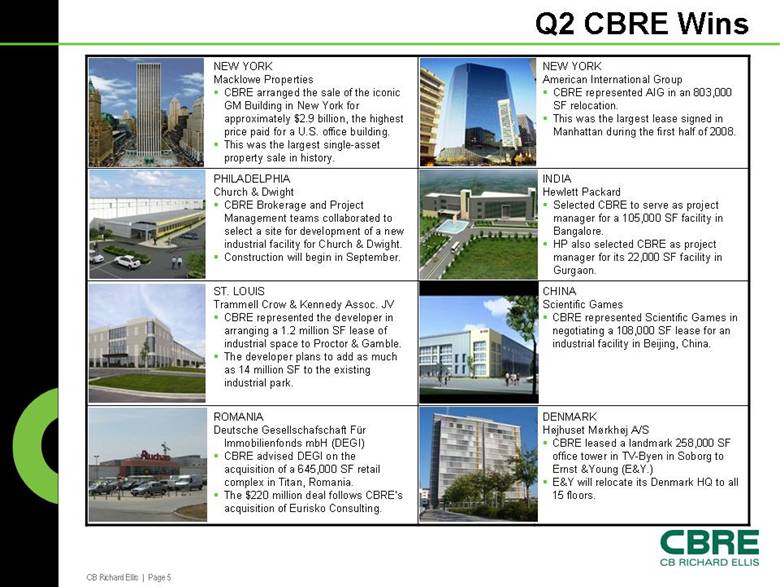

CB Richard Ellis | Page 5 Q2 CBRE Wins DENMARK Højhuset Mørkhøj A/S CBRE leased a landmark 258,000 SF office tower in TV-Byen in Soborg to Ernst &Young (E&Y.) E&Y w ill relocate its Denmark HQ to all 15 floors. ROMANIA Deutsche Gesellschafschaft Für Immobilienfonds mbH (DEGI) CBRE adv ised DEGI on the acquisition of a 645,000 SF retail complex in Titan, Romania. The $220 million deal follows CBRE’s acquisition of Eurisko Consulting. CHINA Scientific Games CBRE represented Scientific Games in negotiating a 108,000 SF lease for an industrial facility in Beijing, China. ST. LOUIS Trammell Crow & Kennedy Assoc. JV CBRE represented the developer in arranging a 1.2 million SF lease of industrial space to Proctor & Gamble. The developer plans to add as much as 14 million SF to the existing industrial park. INDIA Hewlett Packard Selected CBRE to serve as project manager for a 105,000 SF facility in Bangalore. HP also selected CBRE as project manager for its 22,000 SF facility in Gurgaon. PHILADELPHIA Church & Dwight CBRE Brokerage and Project Management teams collaborated to select a site for development of a new industrial facility for Church & Dwight. Construction w ill begin in September. NEW YORK American International Group CBRE represented A IG in an 803,000 SF relocation. This w as the largest lease signed in Manhattan during the first half of 2008. NEW YORK Macklow e Properties CBRE arranged the sale of the iconic GM Building in New York for approximately $2.9 billion, the highest price paid for a U.S. office building. This was the largest single-asset property sale in history. |

|

|

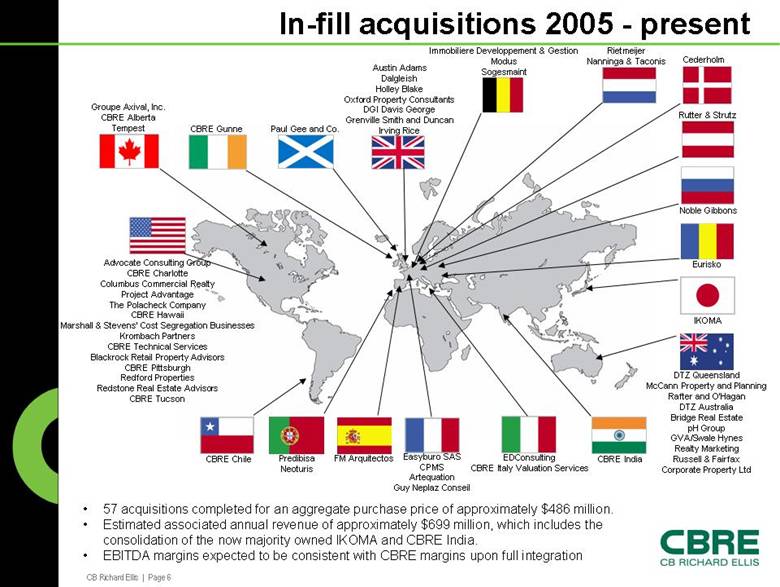

CB Richard Ellis | Page 6 In-fill acquisitions 2005 - present Groupe Axiv al, Inc. CBRE Alberta Tempest Advocate Consulting Group CBRE Charlotte Columbus Commercial Realty Project Advantage The Polacheck Company CBRE Hawaii Marshall & Stevens’ Cost Segregation Businesses Krombach Partners CBRE Technical Services Blackrock Retail Property Advisors CBRE Pittsburgh Redford Properties Redstone Real Estate Advisors CBRE Tucson CBRE Chile CBRE Gunne Paul Gee and Co. Austin Adams Dalgleish Holley Blake Oxford Property Consultants DGI Davis George Grenville Smith and Duncan Irving Rice Immobiliere Dev eloppement & Gestion Modus Sogesmaint Cederholm Rietmeijer Nanninga & Taconis Rutter & Strutz Eurisko Noble Gibbons IKOMA DTZ Queensland McCann Property and Planning Rafter and O’Hagan DTZ Australia Bridge Real Estate pH Group GVA/Swale Hynes Realty Marketing Russell & Fairfax Corporate Property Ltd CBRE India EDConsulting CBRE Italy Valuation Services Easy buro SAS CPMS Artequation Guy Neplaz Conseil FM Arquitectos Predibisa Neoturis • 57 acquisitions completed for an aggregate purchase price of approximately $486 million. • Estimated associated annual revenue of approximately $699 million, which includes the consolidation of the now majority owned IKOMA and CBRE India. • EBITDA margins expected to be consistent with CBRE margins upon full integration |

|

|

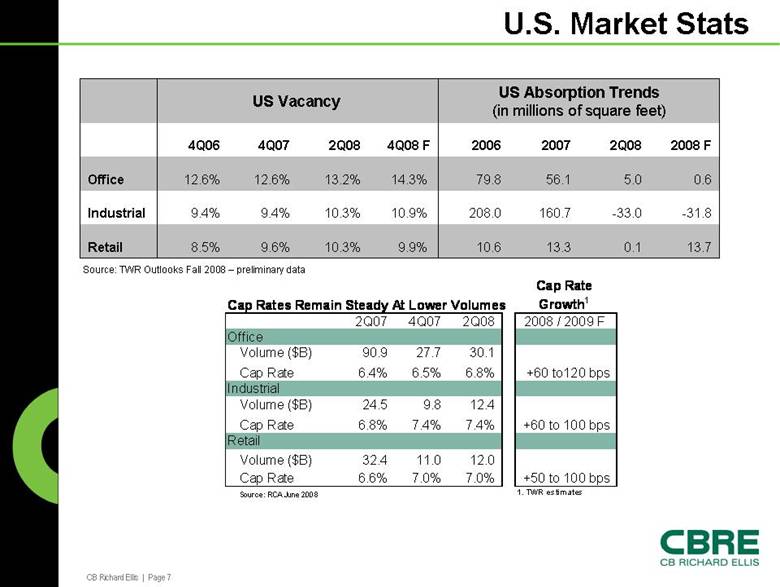

CB Richard Ellis | Page 7 U.S. Market Stats 8.5% 9.4% 12.6% 4Q06 10.6 208.0 79.8 2006 13.7 0.1 13.3 9.9% 10.3% 9.6% Retail -31.8 -33.0 160.7 10.9% 10.3% 9.4% Industrial 0.6 5.0 56.1 14.3% 13.2% 12.6% Office 2008 F 2Q08 2007 4Q08 F 2Q08 4Q07 US Absorption Trends (in millions of square feet) US Vacancy Source: TWR Outlooks Fall 2008 – preliminary data Cap Rates Remain Steady At Lower Volumes Cap Rate Growth 1 2Q07 4Q07 2Q08 2008 / 2009 F Office Volume ($B) 90.9 27.7 30.1 Cap Rate 6.4% 6.5% 6.8% +60 to 120 bps Industrial Volume ($B) 24.5 9.8 12.4 Cap Rate 6.8% 7.4% 7.4% +60 to 100 bps Retail Volume ($B) 32.4 11.0 12.0 Cap Rate 6.6% 7.0% 7.0% +50 to 100 bps Source: RCA June 2008 1. TWR estimates |

|

|

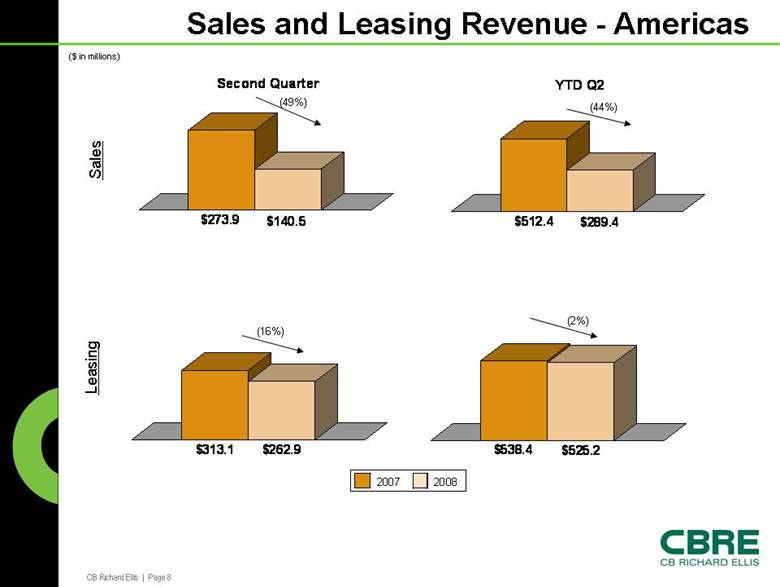

CB Richard Ellis | Page 8 Sales and Leasing Revenue - Americas $512.4 $289.4 YTD Q2 $273.9 $140.5 Second Quarter $538.4 $525.2 $313.1 $262.9 ($ in millions) Sales Leasing (44%) (2%) (49%) (16%) 2007 2008 |

|

|

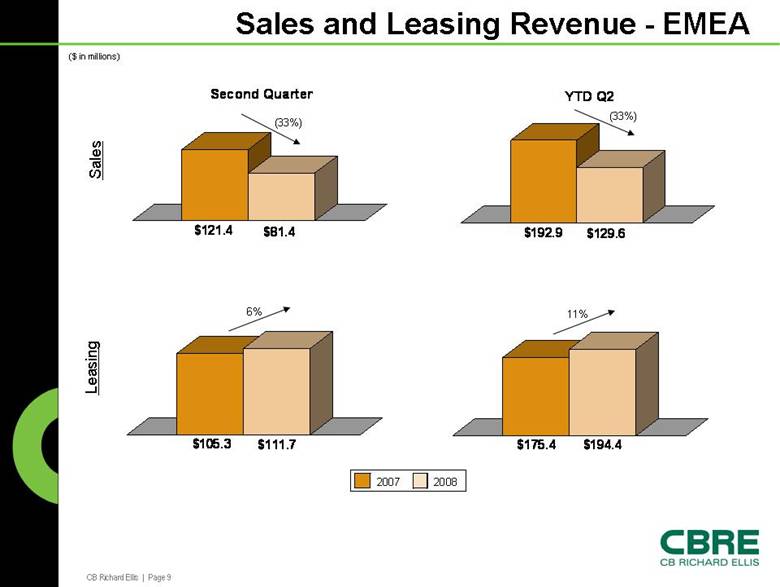

CB Richard Ellis | Page 9 Sales and Leasing Revenue - EMEA $192.9 $129.6 YTD Q2 $121.4 $81.4 Second Quarter $175.4 $194.4 $105.3 $111.7 ($ in millions) Sales Leasing (33%) (33%) 11% 6% 2007 2008 |

|

|

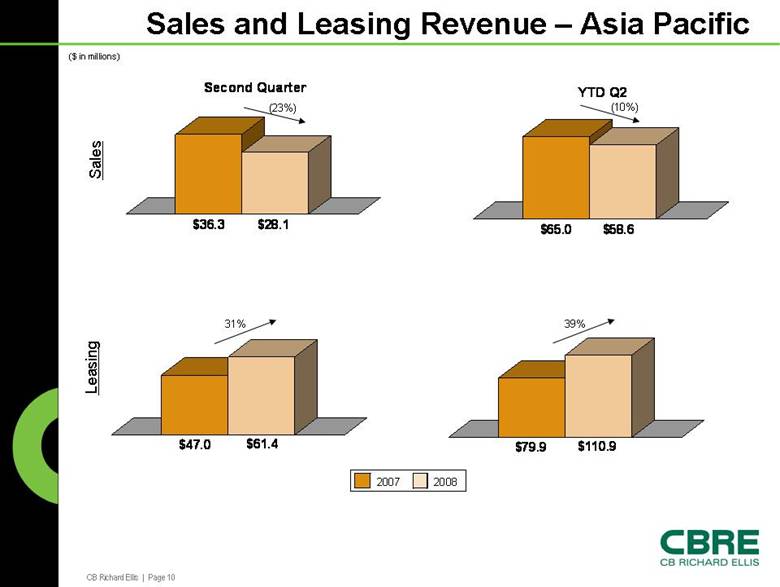

CB Richard Ellis | Page 10 $79.9 $110.9 Sales and Leasing Revenue – Asia Pacific $65.0 $58.6 YTD Q2 $36.3 $28.1 Second Quarter $47.0 $61.4 ($ in millions) Sales Leasing (10%) 39% (23%) 31% 2007 2008 |

|

|

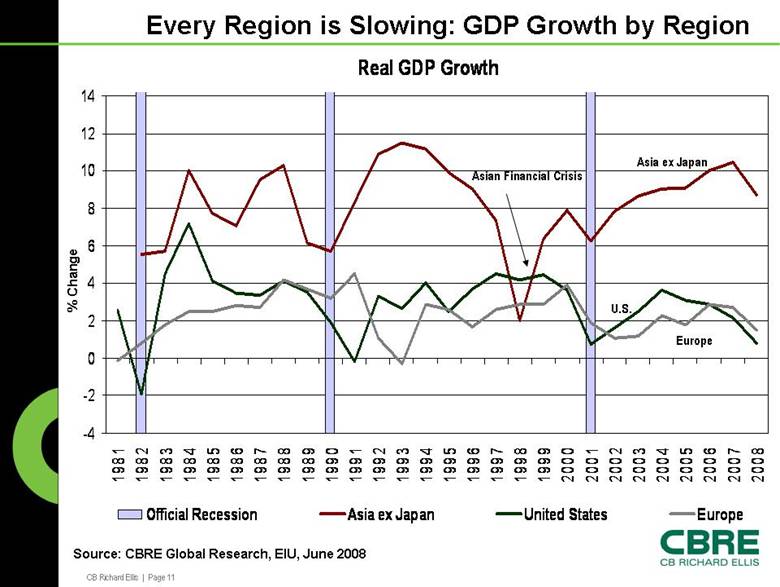

CB Richard Ellis | Page 11 Real GDP Growth -4 -2 0 2 4 6 8 10 12 14 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 Official Recession Asia ex Japan United States Europe Source: CBRE Global Research, EIU, June 2008 % Change Asian Financial Crisis Asia ex Japan Europe U.S. Every Region is Slowing: GDP Growth by Region |

|

|

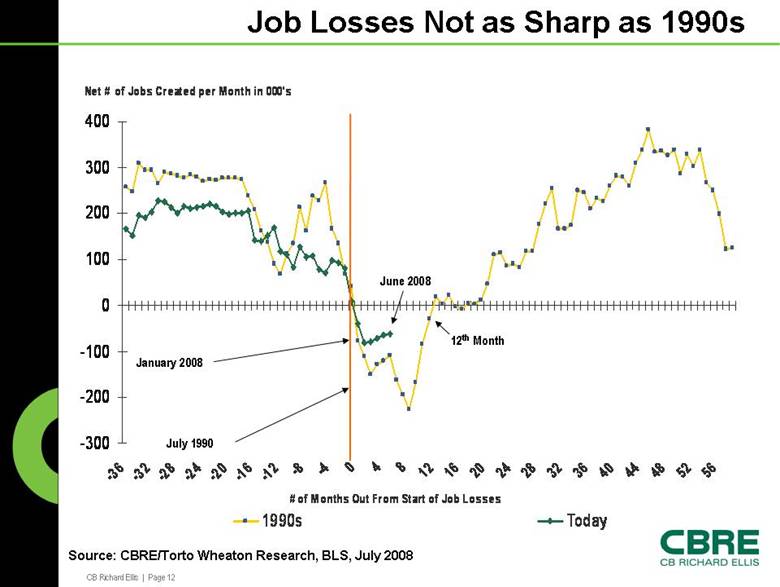

CB Richard Ellis | Page 12 Job Losses Not as Sharp as 1990s -300 -200 -100 0 100 200 300 400 -3 6-3 2-2 8-2 4-2 0-1 6-1 2 -8 -4 0 4 8 12 16 2 0 2 4 2 8 3 2 36 40 44 48 52 56 1990s Today Net # of Jobs Created per Month in 000's # of Months Out From Start of Job Losses July 1990 Source: CBRE/Torto Wheaton Research, BLS, July 2008 January 2008 June 2008 12th Month |

|

|

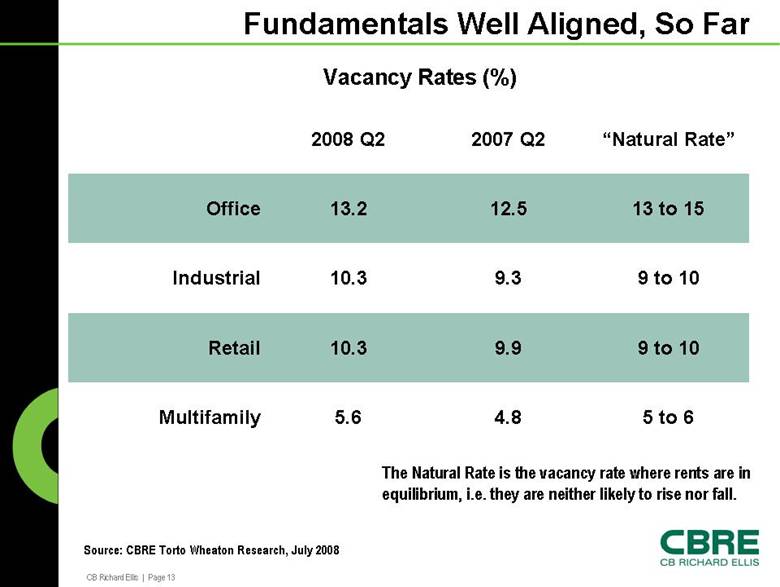

CB Richard Ellis | Page 13 Fundamentals Well Aligned, So Far 5 to 6 4.8 5.6 Multifamily 9 to 10 9.9 10.3 Retail 9 to 10 9.3 10.3 Industrial 13 to 15 12.5 13.2 Office “Natural Rate” 2007 Q2 2008 Q2 Vacancy Rates (%) The Natural Rate is the vacancy rate where rents are in equilibrium, i.e. they are neither likely to rise nor fall. Source: CBRE TortoWheaton Research, July 2008 |

|

|

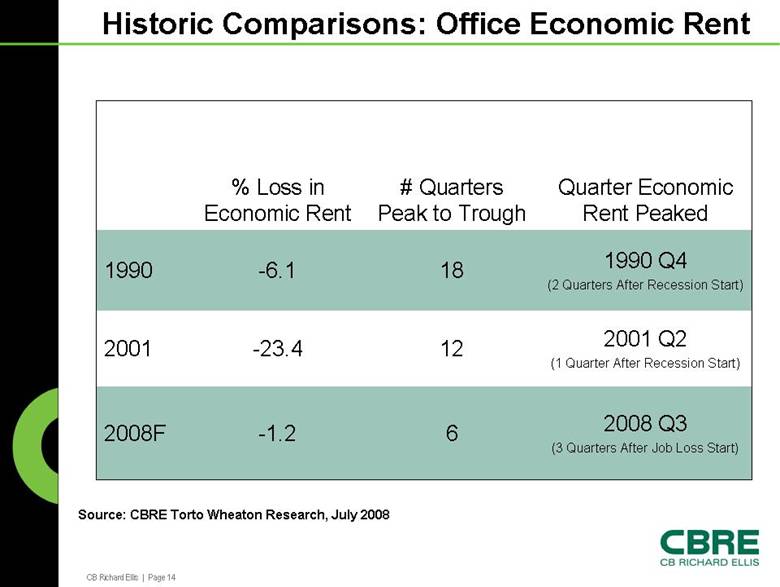

CB Richard Ellis | Page 14 Historic Comparisons: Office Economic Rent -1.2 -23.4 -6.1 % Loss in Economic Rent 2008 Q3 (3 Quarters After Job Loss Start) 2001 Q2 (1 Quarter After Recession Start) 1990 Q4 (2 Quarters After Recession Start) Quarter Economic Rent Peaked 6 2008F 12 2001 18 1990 # Quarters Peak to Trough Source: CBRE Torto Wheaton Research, July 2008 |

|

|

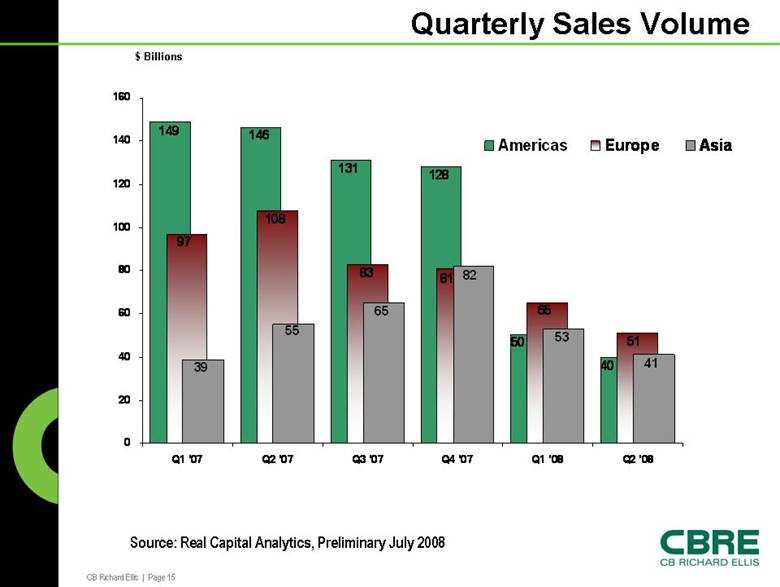

CB Richard Ellis | Page 15 Quarterly Sales Volume 40 50 128 131 146 149 97 108 83 81 65 51 39 55 65 82 53 41 0 20 40 60 80 100 120 140 160 Q1 '07 Q2 '07 Q3 '07 Q4 '07 Q1 '08 Q2 '08 Americas Europe Asia Source: Real Capital Analytics, Preliminary July 2008 $ Billions |

|

|

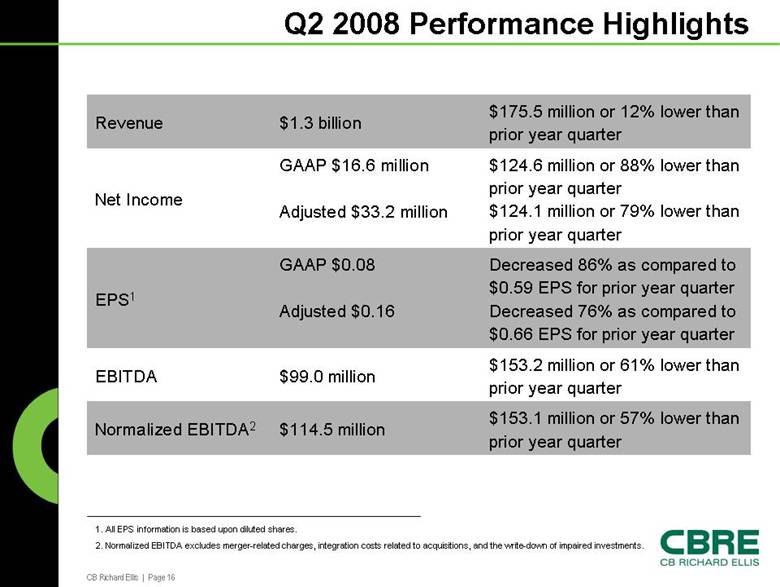

CB Richard Ellis | Page 16 Q2 2008 Performance Highlights $153.1 million or 57% lower than prior year quarter $114.5 million Normalized EBITDA2 $153.2 million or 61% lower than prior year quarter $99.0 million EBITDA Decreased 86% as compared to $0.59 EPS for prior year quarter Decreased 76% as compared to $0.66 EPS for prior year quarter GAAP $0.08 Adjusted $0.16 EPS1 $124.6 million or 88% lower than prior year quarter $124.1 million or 79% lower than prior year quarter GAAP $16.6 million Adjusted $33.2 million Net Income $175.5 million or 12% lower than prior year quarter $1.3 billion Revenue 1. All EPS information is based upon diluted shares. 2. Normalized EBITDA excludes merger-related charges, integration costs related to acquisitions, and the write-down of impaired investments. |

|

|

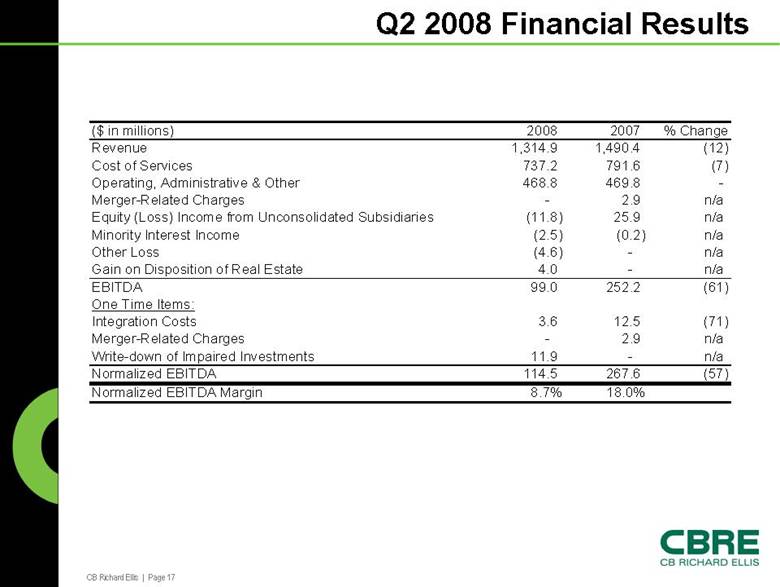

CB Richard Ellis | Page 17 Q2 2008 Financial Results ($ in millions) 2008 2007 % Change Revenue 1,314.9 1,490.4 (12) Cost of Services 737.2 791.6 (7) Operating, Administrative & Other 468.8 469.8 - Merger-Related Charges - 2.9 n/a Equity (Loss) Income from Unconsolidated Subsidiaries (11.8) 25.9 n/a Minority Interest Income (2.5) (0.2) n/a Other Loss (4.6) - n/a Gain on Disposition of Real Estate 4.0 - n/a EBITDA 99.0 252.2 (61) One Time Items: Integration Costs 3.6 12.5 (71) Merger-Related Charges - 2.9 n/a Write-down of Impaired Investments 11.9 - n/a Normalized EBITDA 114.5 267.6 (57) Normalized EBITDA Margin 8.7% 18.0% |

|

|

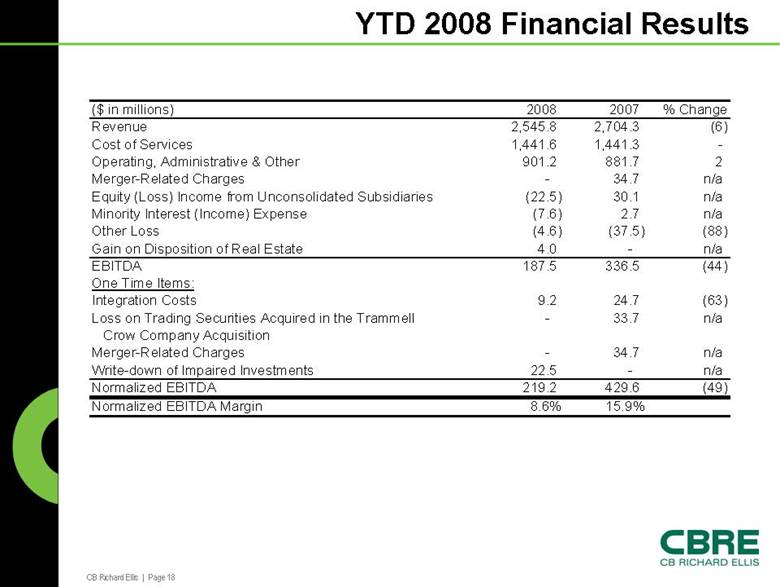

CB Richard Ellis | Page 18 YTD 2008 Financial Results ($ in millions) 2008 2007 % Change Revenue 2,545.8 2,704.3 (6) Cost of Services 1,441.6 1,441.3 - Operating, Administrative & Other 901.2 881.7 2 Merger-Related Charges - 34.7 n/a Equity (Loss) Income from Unconsolidated Subsidiaries (22.5) 30.1 n/a Minority Interest (Income) Expense (7.6) 2.7 n/a Other Loss (4.6) (37.5) (88) Gain on Disposition of Real Estate 4.0 - n/a EBITDA 187.5 336.5 (44) One Time Items: Integration Costs 9.2 24.7 (63) Loss on Trading Securities Acquired in the Trammell - 33.7 n/a Crow Company Acquisition Merger-Related Charges - 34.7 n/a Write-down of Impaired Investments 22.5 - n/a Normalized EBITDA 219.2 429.6 (49) Normalized EBITDA Margin 8.6% 15.9% |

|

|

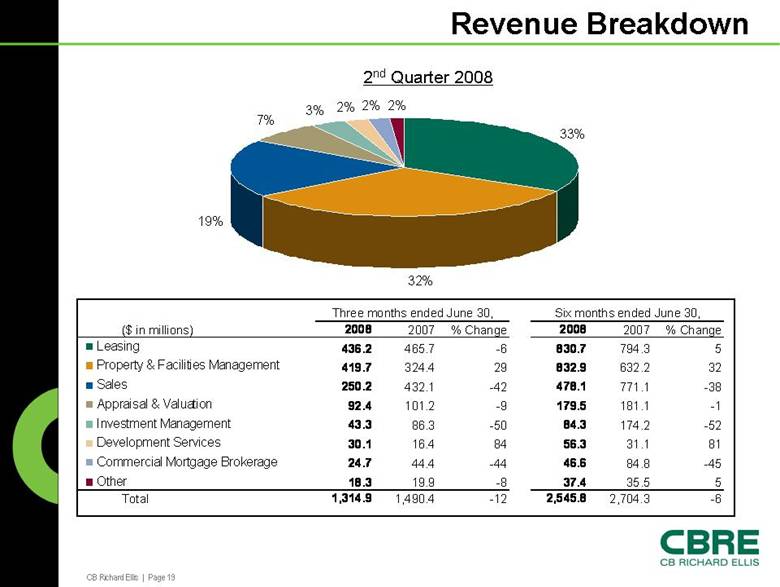

CB Richard Ellis | Page 19 32% 19% 7% 3% 2% 2% 33% 2% Leasing Property & Facilities Management Sales Appraisal & Valuation Investment Management Development Services Commercial Mortgage Brokerage Other Revenue Breakdown 2nd Quarter 2008 ($ in millions) 2008 2007 % Change 2008 2007 % Change 436.2 465.7 -6 830.7 794.3 5 419.7 324.4 29 832.9 632.2 32 250.2 432.1 -42 478.1 771.1 -38 92.4 101.2 -9 179.5 181.1 -1 43.3 86.3 -50 84.3 174.2 -52 30.1 16.4 84 56.3 31.1 81 24.7 44.4 -44 46.6 84.8 -45 18.3 19.9 -8 37.4 35.5 5 Total 1,314.9 1,490.4 -12 2,545.8 2,704.3 -6 Three months ended June 30, Six months ended June 30, |

|

|

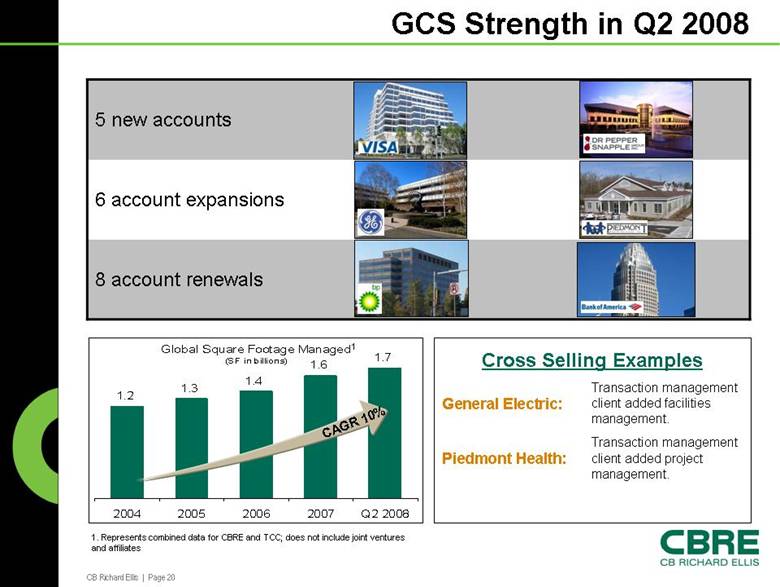

CB Richard Ellis | Page 20 GCS Strength in Q2 2008 8 account renewals 6 account expansions 5 new accounts Transaction management client added project management. Piedmont Health: Transaction management client added facilities management. General Electric: Cross Selling Examples Global Square Footage Managed (SF in billions) 1.2 1.3 1.4 1.6 1.7 2004 2005 2006 2007 Q2 2008 CAGR 1 0% 1. Represents combined data f or CBRE and TCC; does not include joint ventures and affiliates 1 |

|

|

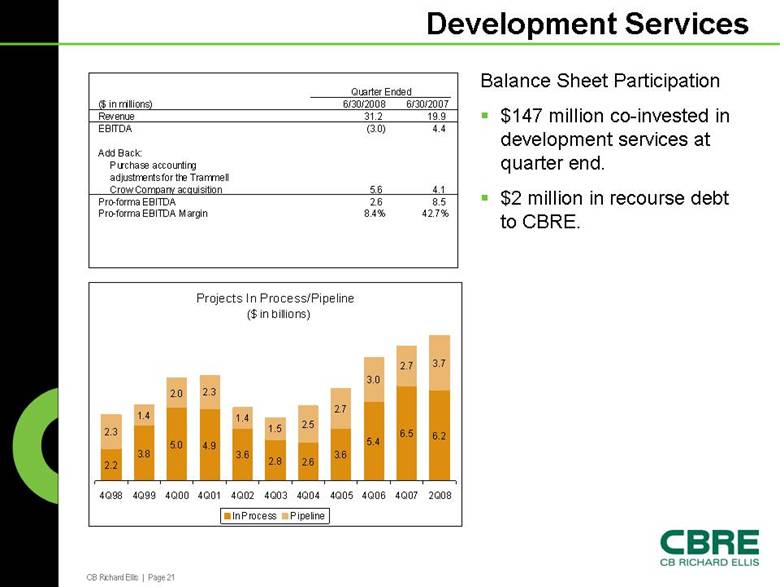

CB Richard Ellis | Page 21 Development Services Balance Sheet Participation $147 million co-invested in development services at quarter end. $2 million in recourse debt to CBRE. ($ in millions) 6/30/2008 6/30/2007 Revenue 31.2 19.9 EBITDA (3.0) 4.4 Add Back: Purchase accounting adjustments for the Trammell Crow Company acquisition 5.6 4.1 Pro-forma EBITDA 2.6 8.5 Pro-forma EBITDA Margin 8.4% 42.7% Quarter Ended Projects In Process/Pipeline ($ in billions) 2.2 3.8 5.0 4.9 3.6 2.8 2.6 3.6 5.4 6.5 6.2 2.3 1.4 2.0 2.3 1.4 1.5 2.5 2.7 3.0 2.7 3.7 4Q98 4Q99 4Q00 4Q01 4Q02 4Q03 4Q04 4Q05 4Q06 4Q07 2Q08 In Process Pipeline |

|

|

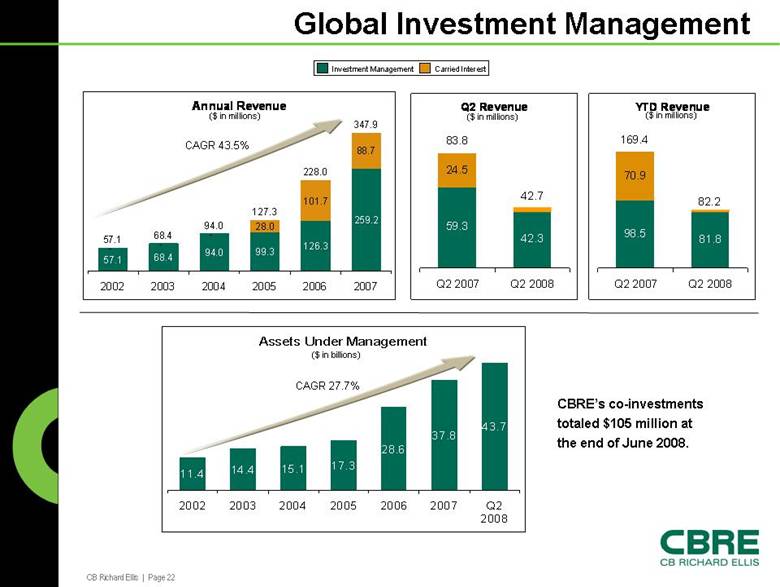

CB Richard Ellis | Page 22 Global Investment Management Annual Revenue 57.1 68.4 94.0 99.3 126.3 259.2 - - - 28.0 101.7 88.7 57.1 68.4 94.0 127.3 228.0 347.9 2002 2003 2004 2005 2006 2007 Assets Under Management 11.4 14.4 15.1 17.3 28.6 37.8 43.7 2002 2003 2004 2005 2006 2007 Q2 2008 Q2 Revenue 59.3 42.3 24.5 83.8 42.7 Q2 2007 Q2 2008 ($ in billions) Investment Management Carried Interest ($ in millions) CBRE’s co-investments totaled $105 million at the end of June 2008. CAGR 43.5% CAGR 27.7% ($ in millions) YTD Revenue 98.5 81.8 70.9 169.4 82.2 Q2 2007 Q2 2008 ($ in millions) |

|

|

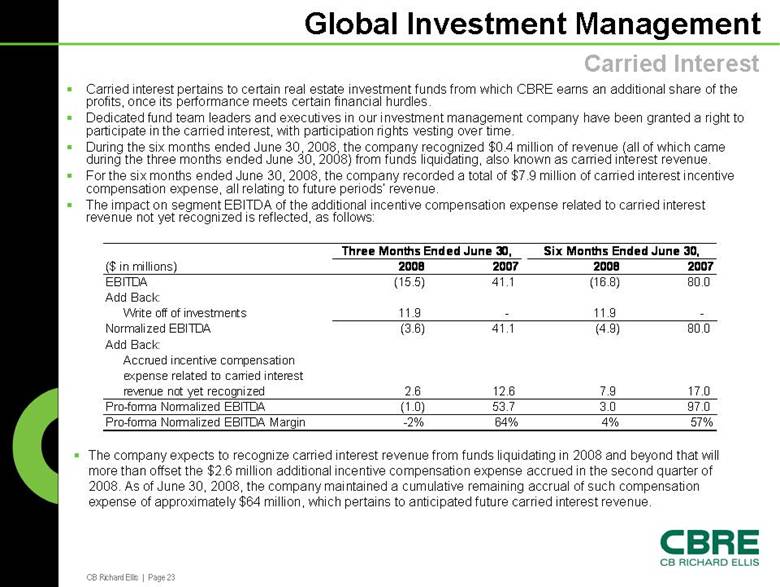

CB Richard Ellis | Page 23 Global Investment Management Carried interest pertains to certain real estate investment funds from which CBRE earns an additional share of the profits, once its performance meets certain financial hurdles. Dedicated fund team leaders and executives in our investment management company have been granted a right to participate in the carried interest, with participation rights vesting over time. During the six months ended June 30, 2008, the company recognized $0.4 million of revenue (all of which came during the three months ended June 30, 2008) from funds liquidating, also known as carried interest revenue. For the six months ended June 30, 2008, the company recorded a total of $7.9 million of carried interest incentive compensation expense, all relating to future periods’ revenue. The impact on segment EBITDA of the additional incentive compensation expense related to carried interest revenue not yet recognized is reflected, as follows: Carried Interest The company expects to recognize carried interest revenue from funds liquidating in 2008 and beyond that will more than offset the $2.6 million additional incentive compensation expense accrued in the second quarter of 2008. As of June 30, 2008, the company maintained a cumulative remaining accrual of such compensation expense of approximately $64 million, which pertains to anticipated future carried interest revenue. ($ in millions) 2008 2007 2008 2007 EBITDA (15.5) 41.1 (16.8) 80.0 Add Back: Write off of investments 11.9 - 11.9 - Normalized EBITDA (3.6) 41.1 (4.9) 80.0 Add Back: Accrued incentive compensation expense related to carried interest revenue not yet recognized 2.6 12.6 7.9 17.0 Pro-forma Normalized EBITDA (1.0) 53.7 3.0 97.0 Pro-forma Normalized EBITDA Margin -2% 64% 4% 57% Three Months Ended June 30, Six Months Ended June 30, |

|

|

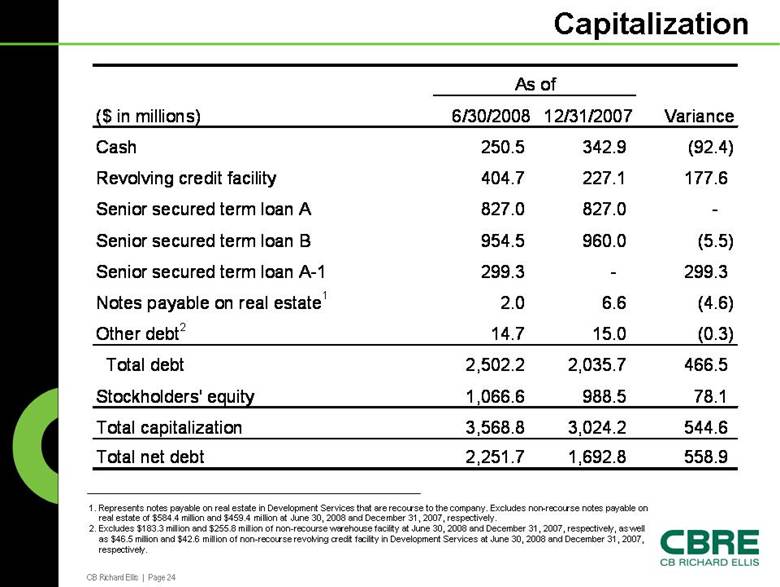

CB Richard Ellis | Page 24 Capitalization 1. Represents notes pay able on real estate in Development Services that are recourse to the company. Excludes non-recourse notes pay able on real estate of $584.4 million and $459.4 million at June 30, 2008 and December 31, 2007, respectively. 2. Excludes $183.3 million and $255.8 million of non-recourse warehouse facility at June 30, 2008 and December 31, 2007, respectively , as well as $46.5 million and $42.6 million of non-recourse revolving credit facility in Development Services at June 30, 2008 and December 31, 2007, respectively. ($ in millions) 6/30/2008 12/31/2007 Variance Cash 250.5 342.9 (92.4) Revolving credit facility 404.7 227.1 177.6 Senior secured term loan A 827.0 827.0 - Senior secured term loan B 954.5 960.0 (5.5) Senior secured term loan A-1 299.3 - 299.3 Notes payable on real estate 1 2.0 6.6 (4.6) Other debt 2 14.7 15.0 (0.3) Total debt 2,502.2 2,035.7 466.5 Stockholders' equity 1,066.6 988.5 78.1 Total capitalization 3,568.8 3,024.2 544.6 Total net debt 2,251.7 1,692.8 558.9 As of |

|

|

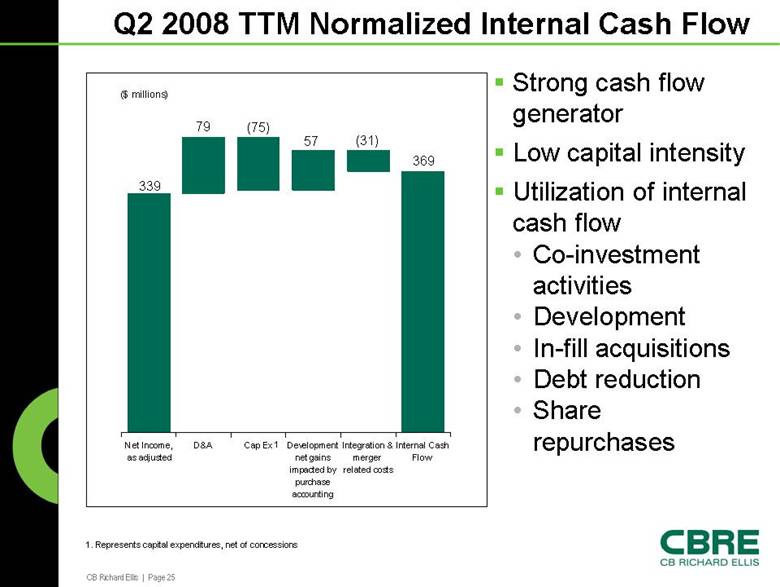

CB Richard Ellis | Page 25 Internal Cash Flow Integration & merger related costs Development net gains impacted by purchase accounting Cap Ex D&A Net Income, as adjusted ($ millions) Q2 2008 TTM Normalized Internal Cash Flow Strong cash flow generator Low capital intensity Utilization of internal cash flow • Co-investment activities • Development • In-fill acquisitions • Debt reduction • Share repurchases 339 79 (75) 57 (31) 369 1 1. Represents capital expenditures, net of concessions |

|

|

CB Richard Ellis | Page 26 Summary Deteriorating market conditions make it impossible to provide guidance Our current view has changed reflecting weaker market factors Outsourcing strength is expected to continue Variable cost structure and expense reductions partially offset margin decline We will remain aggressive in our client pursuits, M&A activity and strategic recruitment to gain further market share in this downturn. Currently anticipate markets to improve in mid-to-late 2009 Business Outlook |

|

|

CB Richard Ellis | Page 27 GAAP Reconciliation Tables |

|

|

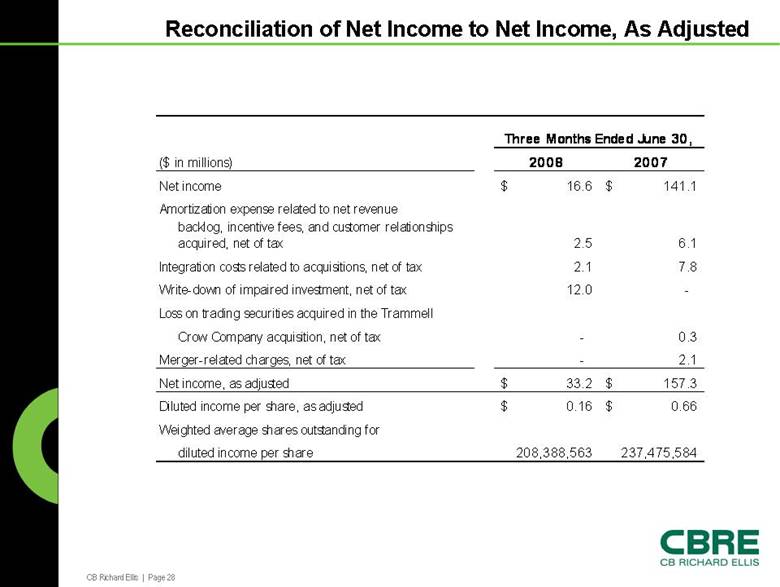

CB Richard Ellis | Page 28 Reconciliation of Net Income to Net Income, As Adjusted ($ in millions) 2008 2007 Net income 16.6 $ 141.1 $ Amortization expense related to net revenue backlog, incentive fees, and customer relationships acquired, net of tax 2.5 6.1 Integration costs related to acquisitions, net of tax 2.1 7.8 Write-down of impaired investment, net of tax 12.0 - Loss on trading securities acquired in the Trammell Crow Company acquisition, net of tax - 0.3 Merger-related charges, net of tax - 2.1 Net income, as adjusted 33.2 $ 157.3 $ Diluted income per share, as adjusted 0.16 $ 0.66 $ Weighted average shares outstanding for diluted income per share 208,388,563 237,475,584 Three Months Ended June 30, |

|

|

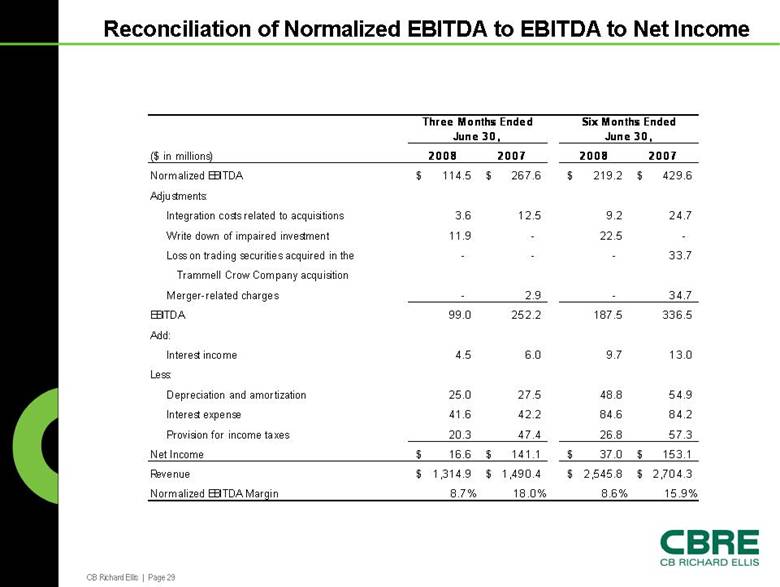

CB Richard Ellis | Page 29 Reconciliation of Normalized EBITDA to EBITDA to Net Income ($ in millions) 2008 2007 2008 2007 Normalized EBITDA 114.5 $ 267.6 $ 219.2 $ 429.6 $ Adjustments: Integration costs related to acquisitions 3.6 12.5 9.2 24.7 Write down of impaired investment 11.9 - 22.5 - Loss on trading securities acquired in the - - - 33.7 Trammell Crow Company acquisition Merger-related charges - 2.9 - 34.7 EBITDA 99.0 252.2 187.5 336.5 Add: Interest income 4.5 6.0 9.7 13.0 Less: Depreciation and amortization 25.0 27.5 48.8 54.9 Interest expense 41.6 42.2 84.6 84.2 Provision for income taxes 20.3 47.4 26.8 57.3 Net Income 16.6 $ 141.1 $ 37.0 $ 153.1 $ Revenue 1,314.9 $ 1,490.4 $ 2,545.8 $ 2,704.3 $ Normalized EBITDA Margin 8.7% 18.0% 8.6% 15.9% Three Months Ended June 3 0, Six Months Ended June 30 , |

|

|

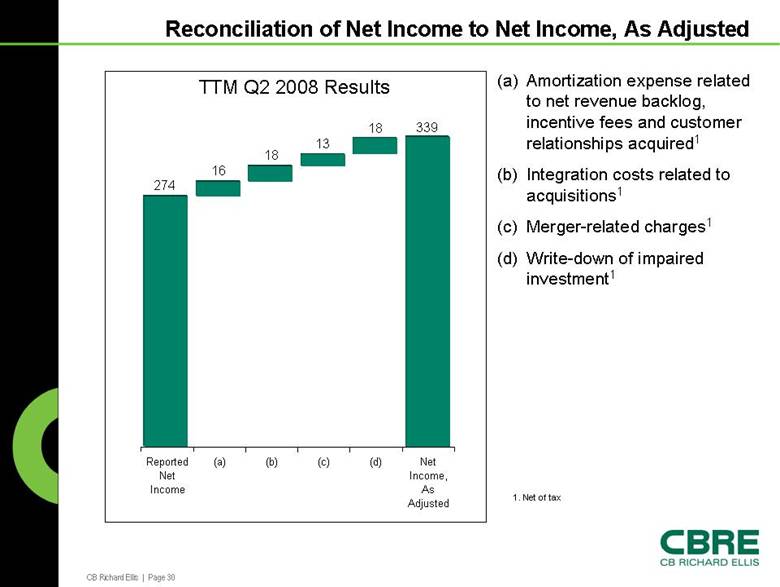

CB Richard Ellis | Page 30 Net Income, As Adjusted (d) (c) (b) (a) Reported Net Income Reconciliation of Net Income to Net Income, As Adjusted TTM Q2 2008 Results 274 16 18 13 18 339 (a) Amortization expense related to net revenue backlog, incentive fees and customer relationships acquired1 (b) Integration costs related to acquisitions1 (c) Merger-related charges1 (d) Write-down of impaired investment1 1. Net of tax |