Exhibit 99.1

|

|

Investor Presentation March 2007 |

Exhibit 99.1

|

|

Investor Presentation March 2007 |

|

|

Forward Looking Statements This presentation contains statements that are forward looking within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding our growth momentum in 2007, future operations, future financial performance, and the impact of our acquisition of the Trammell Crow Company and related financing. These statements should be considered as estimates only and actual results may ultimately differ from these estimates. Except to the extent required by applicable securities laws, we undertake no obligation to update or publicly revise any of the forward-looking statements that you may hear today. Please refer to our current annual report on Form 10-K (in particular, “Risk Factors”) which is filed with the SEC and available at the SEC’s website (http://www.sec.gov), for a full discussion of the risks and other factors that may impact any estimates that you may hear today. We may make certain statements during the course of this presentation which include references to “non-GAAP financial measures”, as defined by SEC regulations. As required by these regulations, we have provided reconciliations of these measures to what we believe are the most directly comparable GAAP measures, which are attached hereto within the appendix. |

|

|

Industry/Company Trends |

|

|

2.5x nearest competitor Thousands of clients, 85% of Fortune 100 2006 combined CBRE & TCC Revenue of approximately $5 billion 2006 combined CBRE & TCC EBITDA of $759 million(2) Strong organic revenue and earnings growth #1 commercial real estate brokerage #1 appraisal and valuation #1 property and facilities management #2 commercial mortgage brokerage $29 billion in investment assets under management(1) $8 billion of development projects in process/pipeline(1) Leading Global Brand Broad Capabilities Scale, Diversity and Earnings Power 100 years 50 countries #1 in key cities in U.S., Europe and Asia (1) As of 12/31/2006. (2) EBITDA excludes one-time items, including integration costs related to acquisitions and income related to investment in Savills. Combined normalized EBITDA includes $107.1 million for TCC for the period January 1, 2006 through December 31, 2006. The World’s Premier Commercial Real Estate Services Provider |

|

|

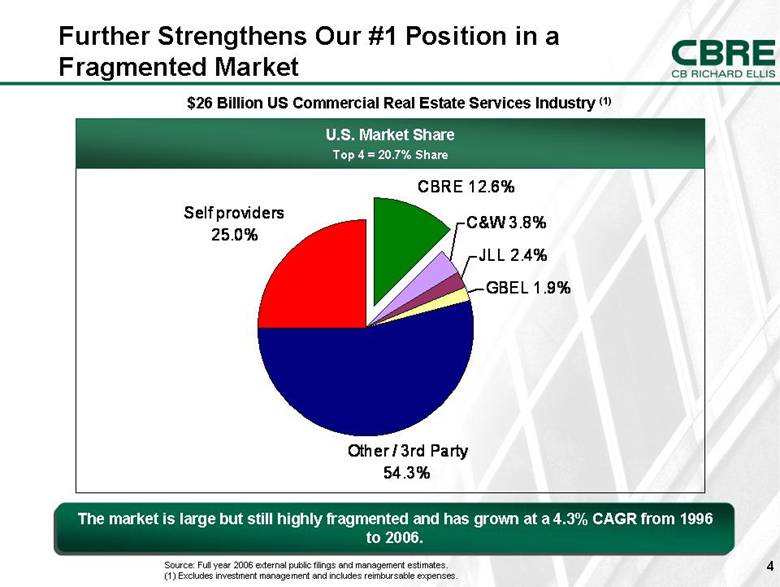

$26 Billion US Commercial Real Estate Services Industry (1) U.S. Market Share Top 4 = 20.7% Share Further Strengthens Our #1 Position in a Fragmented Market Source: Full year 2006 external public filings and management estimates. (1) Excludes investment management and includes reimbursable expenses. The market is large but still highly fragmented and has grown at a 4.3% CAGR from 1996 to 2006. Self providers 25.0% CBRE 12.6% C&W 3.8% JLL 2.4% GBEL 1.9% Other / 3rd Party 54.3% |

|

|

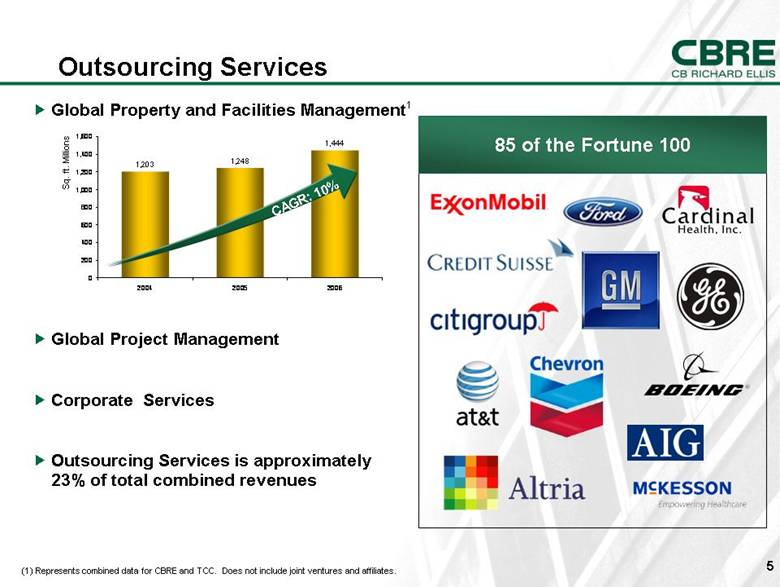

Outsourcing Services 85 of the Fortune 100 Sq. ft. Millions CAGR: 10% Global Property and Facilities Management1 Global Project Management Corporate Services Outsourcing Services is approximately 23% of total combined revenues (1) Represents combined data for CBRE and TCC. Does not include joint ventures and affiliates. |

|

|

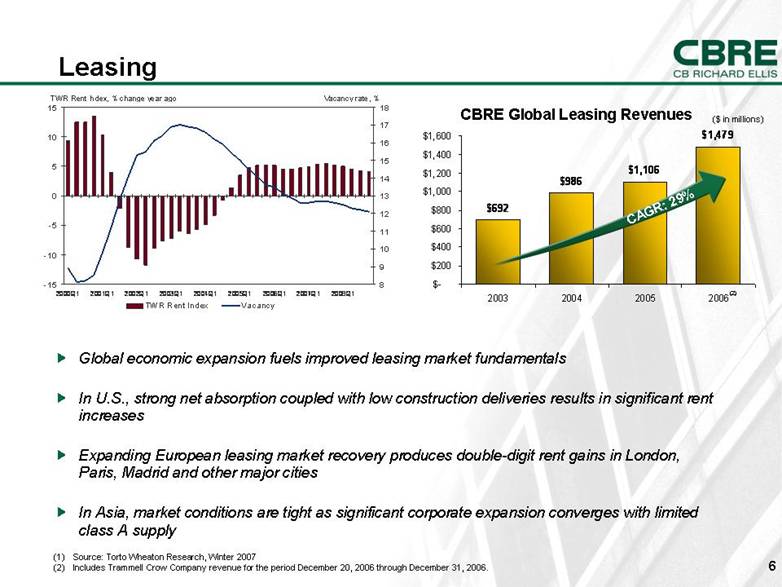

Global economic expansion fuels improved leasing market fundamentals In U.S., strong net absorption coupled with low construction deliveries results in significant rent increases Expanding European leasing market recovery produces double-digit rent gains in London, Paris, Madrid and other major cities In Asia, market conditions are tight as significant corporate expansion converges with limited class A supply (1) Source: Torto Wheaton Research, Winter 2007 (2) Includes Trammell Crow Company revenue for the period December 20, 2006 through December 31, 2006. Leasing CAGR: 29% CBRE Global Leasing Revenues ($ in millions) (2) $692 $986 $1,106 $1,479 $- $200 $400 $600 $800 $1,000 $1,200 $1,400 $1,600 2003 2004 2005 2006 -15 -10 -5 0 5 10 15 2000Q1 2001Q1 2002Q1 2003Q1 2004Q1 2005Q1 2006Q1 2007Q1 2008Q1 8 9 10 11 12 13 14 15 16 17 18 TWR Rent Index Vacancy TWR Rent Index, % change year ago Vacancy rate, % |

|

|

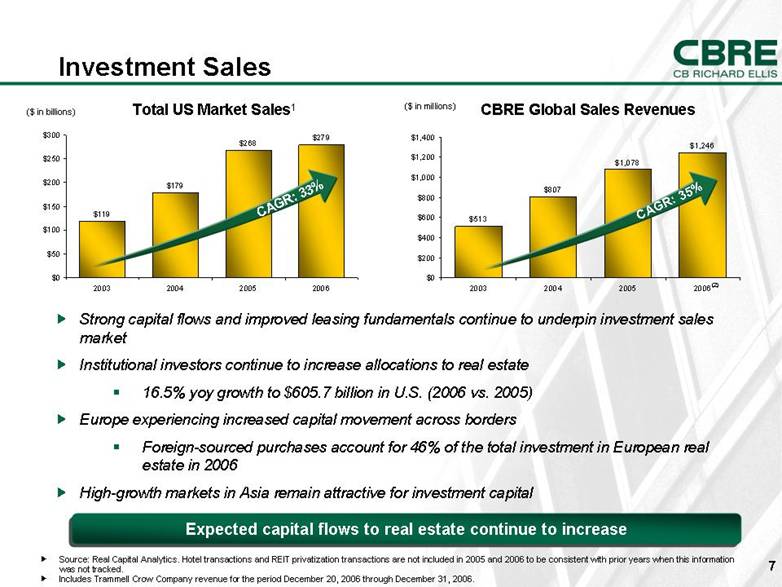

Investment Sales Strong capital flows and improved leasing fundamentals continue to underpin investment sales market Institutional investors continue to increase allocations to real estate 16.5% yoy growth to $605.7 billion in U.S. (2006 vs. 2005) Europe experiencing increased capital movement across borders Foreign-sourced purchases account for 46% of the total investment in European real estate in 2006 High-growth markets in Asia remain attractive for investment capital ($ in billions) CAGR: 33% Expected capital flows to real estate continue to increase CAGR: 35% ($ in millions) CBRE Global Sales Revenues Total US Market Sales1 Source: Real Capital Analytics. Hotel transactions and REIT privatization transactions are not included in 2005 and 2006 to be consistent with prior years when this information was not tracked. Includes Trammell Crow Company revenue for the period December 20, 2006 through December 31, 2006. (2) $513 $807 $1,078 $1,246 $0 $200 $400 $600 $800 $1,000 $1,200 $1,400 2003 2004 2005 2006 $119 $179 $268 $279 $0 $50 $100 $150 $200 $250 $300 2003 2004 2005 2006 |

|

|

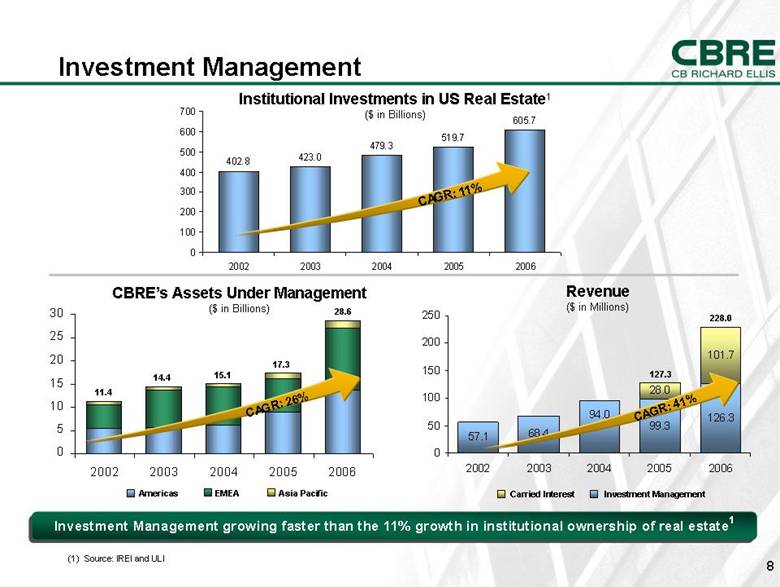

Investment Management Americas EMEA Asia Pacific Investment Management growing faster than the 11% growth in institutional ownership of real estate1 CBRE’s Assets Under Management ($ in Billions) Revenue ($ in Millions) (1) Source: IREI and ULI CAGR: 41% 127.3 228.0 CAGR: 26% Carried Interest Investment Management Institutional Investments in US Real Estate1 ($ in Billions) CAGR: 11% 17.3 28.6 15.1 11.4 14.4 0 5 10 15 20 25 30 2002 2003 2004 2005 2006 57.1 68.4 99.3 126.3 28.0 101.7 94.0 0 50 100 150 200 250 2002 2003 2004 2005 2006 |

|

|

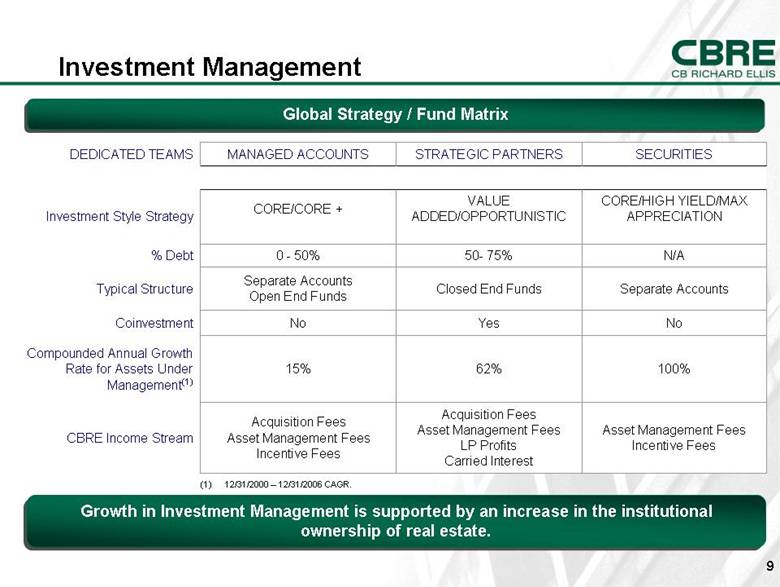

Investment Management Global Strategy / Fund Matrix 100% 62% 15% Compounded Annual Growth Rate for Assets Under Management(1) No Yes No Coinvestment Asset Management Fees Incentive Fees Acquisition Fees Asset Management Fees LP Profits Carried Interest Acquisition Fees Asset Management Fees Incentive Fees CBRE Income Stream Separate Accounts Closed End Funds Separate Accounts Open End Funds Typical Structure N/A 50- 75% 0 - 50% % Debt CORE/HIGH YIELD/MAX APPRECIATION VALUE ADDED/OPPORTUNISTIC CORE/CORE + Investment Style Strategy SECURITIES STRATEGIC PARTNERS MANAGED ACCOUNTS DEDICATED TEAMS (1) 12/31/2000 – 12/31/2006 CAGR. Growth in Investment Management is supported by an increase in the institutional ownership of real estate. |

|

|

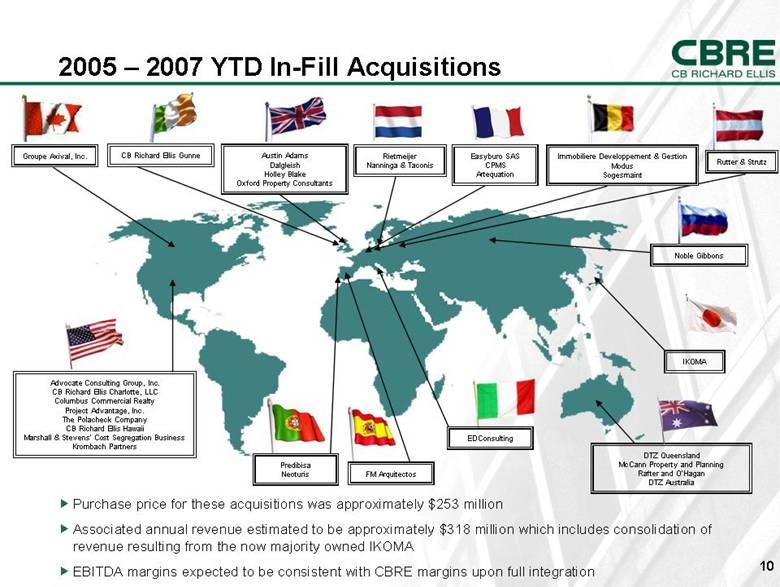

2005 – 2007 YTD In-Fill Acquisitions Easyburo SAS CPMS Artequation DTZ Queensland McCann Property and Planning Rafter and O’Hagan DTZ Australia Advocate Consulting Group, Inc. CB Richard Ellis Charlotte, LLC Columbus Commercial Realty Project Advantage, Inc. The Polacheck Company CB Richard Ellis Hawaii Marshall & Stevens’ Cost Segregation Business Krombach Partners Rutter & Strutz Groupe Axival, Inc. Noble Gibbons IKOMA Purchase price for these acquisitions was approximately $253 million Associated annual revenue estimated to be approximately $318 million which includes consolidation of revenue resulting from the now majority owned IKOMA EBITDA margins expected to be consistent with CBRE margins upon full integration CB Richard Ellis Gunne Immobiliere Developpement & Gestion Modus Sogesmaint Austin Adams Dalgleish Holley Blake Oxford Property Consultants Predibisa Neoturis Rietmeijer Nanninga & Taconis EDConsulting FM Arquitectos |

|

|

Trammell Crow Company Acquisition Business is comprised of: Global Corporate Services (GCS) and Development Services GCS consists of the following businesses: Property & Facilities Management Project Management Corporate Advisory Transaction Management Statistics # of Employees – 7,600 # of Project Managers – 1,600 # of Offices – 71 Revenue of approximately $1 billion Further diversification of revenue mix Significant revenue synergy potential Transaction expected to produce net synergies of $65M Projected EPS accretion in the low teens |

|

|

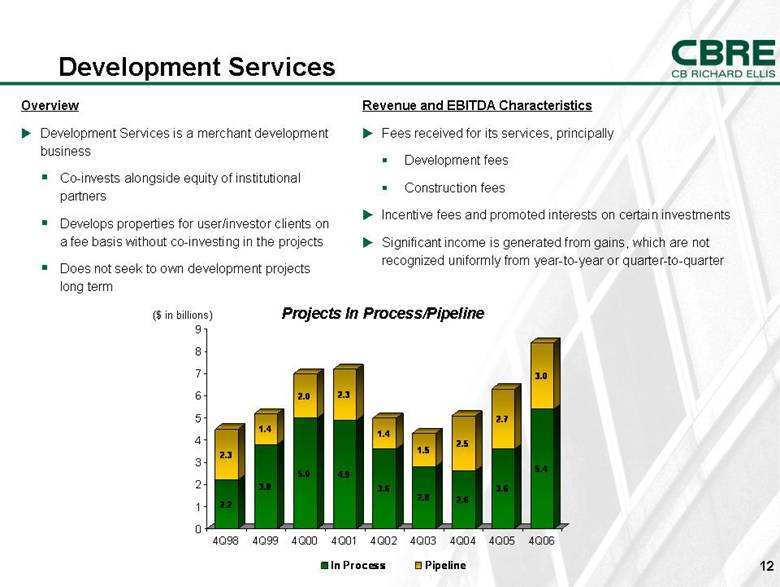

Development Services Overview Development Services is a merchant development business Co-invests alongside equity of institutional partners Develops properties for user/investor clients on a fee basis without co-investing in the projects Does not seek to own development projects long term Revenue and EBITDA Characteristics Fees received for its services, principally Development fees Construction fees Incentive fees and promoted interests on certain investments Significant income is generated from gains, which are not recognized uniformly from year-to-year or quarter-to-quarter ($ in billions) Projects In Process/Pipeline 2.2 2.3 3.8 1.4 5.0 2.0 4.9 2.3 3.6 1.4 2.8 1.5 2.6 2.5 3.6 2.7 5.4 3.0 0 1 2 3 4 5 6 7 8 9 4Q98 4Q99 4Q00 4Q01 4Q02 4Q03 4Q04 4Q05 4Q06 In Process Pipeline |

|

|

Financial Overview |

|

|

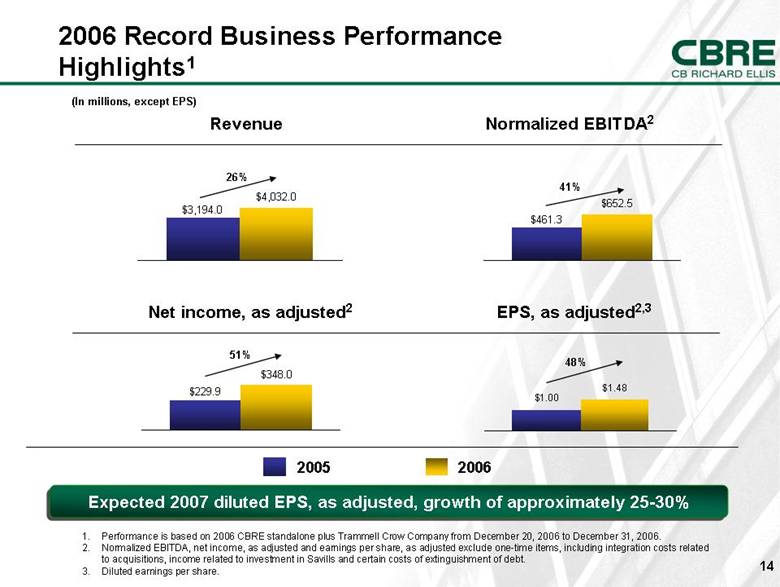

2006 Record Business Performance Highlights1 2005 2006 26% (In millions, except EPS) 41% Revenue Normalized EBITDA2 51% 48% Net income, as adjusted2 EPS, as adjusted2,3 1. Performance is based on 2006 CBRE standalone plus Trammell Crow Company from December 20, 2006 to December 31, 2006. 2. Normalized EBITDA, net income, as adjusted and earnings per share, as adjusted exclude one-time items, including integration costs related to acquisitions, income related to investment in Savills and certain costs of extinguishment of debt. 3. Diluted earnings per share. Expected 2007 diluted EPS, as adjusted, growth of approximately 25-30% $1.00 $1.48 $348.0 $229.9 $652.5 $461.3 $4,032.0 $3,194.0 |

|

|

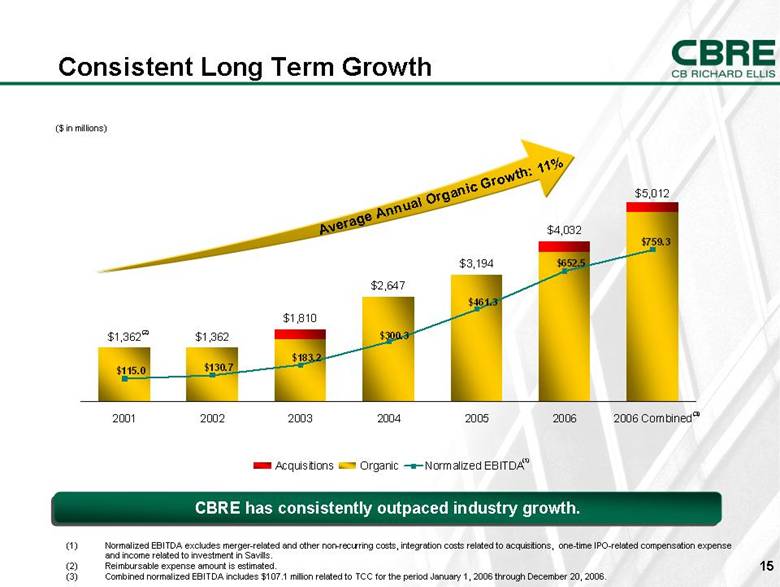

Consistent Long Term Growth CBRE has consistently outpaced industry growth. (1) Normalized EBITDA excludes merger-related and other non-recurring costs, integration costs related to acquisitions, one-time IPO-related compensation expense and income related to investment in Savills. (2) Reimbursable expense amount is estimated. (3) Combined normalized EBITDA includes $107.1 million related to TCC for the period January 1, 2006 through December 20, 2006. ($ in millions) Average Annual Organic Growth: 11% (1) (2) (3) $1,362 $1,362 $1,810 $2,647 $3,194 $4,032 $5,012 $652.5 $461.3 $300.3 $183.2 $130.7 $115.0 $759.3 2001 2002 2003 2004 2005 2006 2006 Combined Acquisitions Organic Normalized EBITDA |

|

|

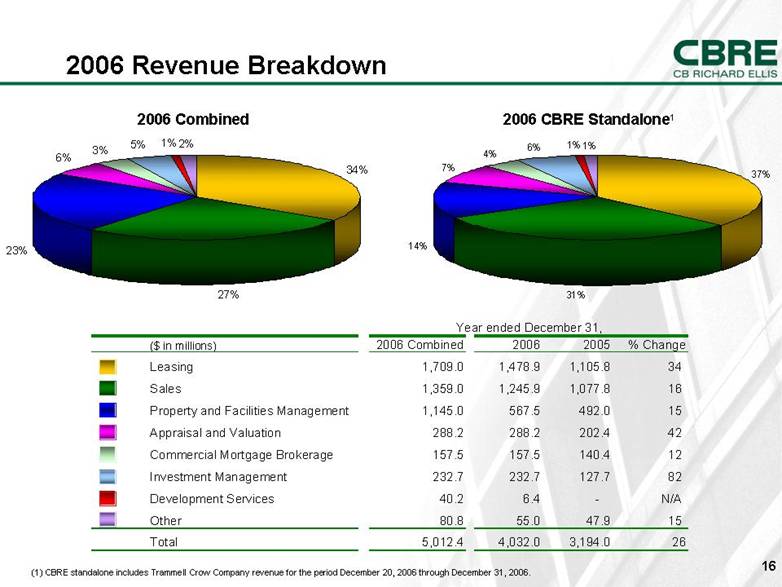

2006 Revenue Breakdown 2006 CBRE Standalone1 2006 Combined (1) CBRE standalone includes Trammell Crow Company revenue for the period December 20, 2006 through December 31, 2006. 34% 27% 23% 6% 3% 5% 1% 2% 37% 31% 14% 7% 4% 6% 1% 1% ($ in millions) 2006 Combined 2006 2005 % Change Leasing 1,709.0 1,478.9 1,105.8 34 Sales 1,359.0 1,245.9 1,077.8 16 Property and Facilities Management 1,145.0 567.5 492.0 15 Appraisal and Valuation 288.2 288.2 202.4 42 Commercial Mortgage Brokerage 157.5 157.5 140.4 12 Investment Management 232.7 232.7 127.7 82 Development Services 40.2 6.4 - N/A Other 80.8 55.0 47.9 15 Total 5,012.4 4,032.0 3,194.0 26 Year ended December 31, |

|

|

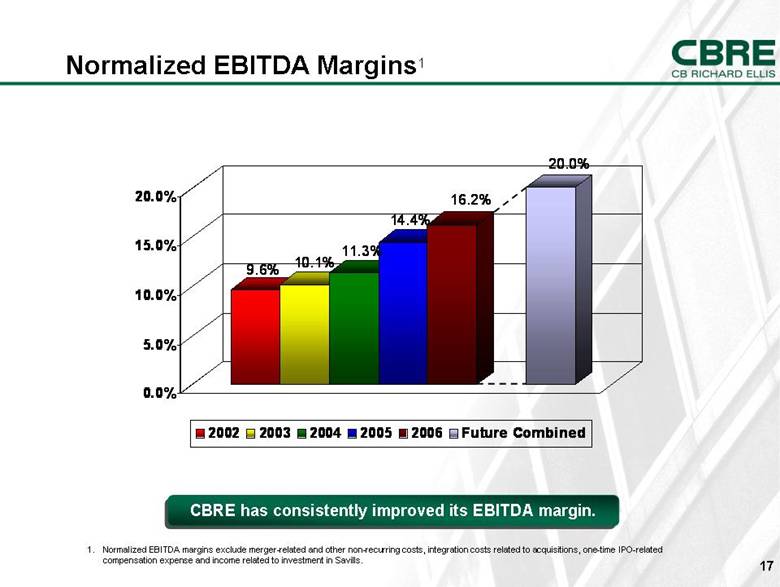

Normalized EBITDA Margins1 CBRE has consistently improved its EBITDA margin. 1. Normalized EBITDA margins exclude merger-related and other non-recurring costs, integration costs related to acquisitions, one-time IPO-related compensation expense and income related to investment in Savills. 9.6% 10.1% 11.3% 14.4% 16.2% 20.0% 0.0% 5.0% 10.0% 15.0% 20.0% 2002 2003 2004 2005 2006 Future Combined |

|

|

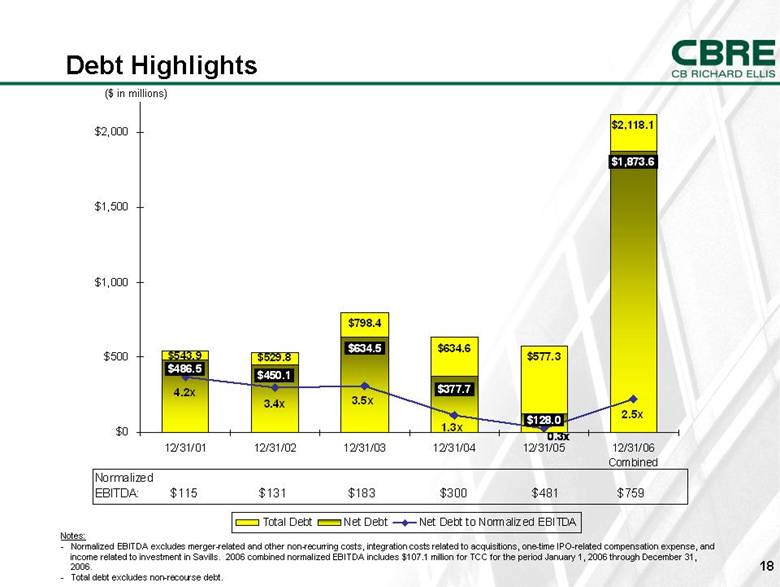

($ in millions) Debt Highlights Notes: - Normalized EBITDA excludes merger-related and other non-recurring costs, integration costs related to acquisitions, one-time IPO-related compensation expense, and income related to investment in Savills. 2006 combined normalized EBITDA includes $107.1 million for TCC for the period January 1, 2006 through December 31, 2006. - Total debt excludes non-recourse debt. $798.4 $634.6 $577.3 $2,118.1 $450.1 $634.5 $128.0 $1,873.6 $543.9 $529.8 $377.7 $486.5 4.2x 3.4x 2.5x 1.3x 0.3x 3.5x $0 $500 $1,000 $1,500 $2,000 12/31/01 12/31/02 12/31/03 12/31/04 12/31/05 12/31/06 Combined Total Debt Net Debt Net Debt to Normalized EBITDA Normalized EBITDA: $115 $131 $183 $300 $481 $759 |

|

|

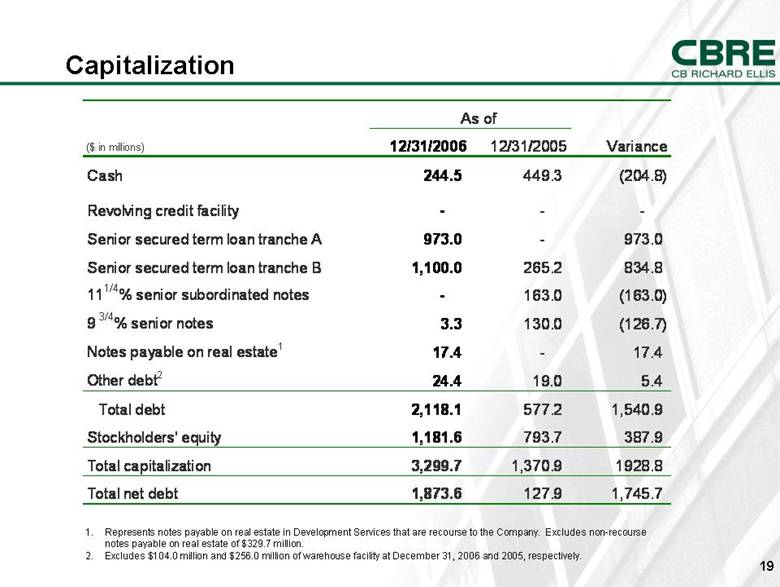

Capitalization Represents notes payable on real estate in Development Services that are recourse to the Company. Excludes non-recourse notes payable on real estate of $329.7 million. Excludes $104.0 million and $256.0 million of warehouse facility at December 31, 2006 and 2005, respectively. ($ in millions) 12/31/2006 12/31/2005 Variance Cash 244.5 449.3 (204.8) Revolving credit facility - - - Senior secured term loan tranche A 973.0 - 973.0 Senior secured term loan tranche B 1,100.0 265.2 834.8 11 1/4 % senior subordinated notes - 163.0 (163.0) 9 3/4 % senior notes 3.3 130.0 (126.7) Notes payable on real estate 1 17.4 - 17.4 Other debt 2 24.4 19.0 5.4 Total debt 2,118.1 577.2 1,540.9 Stockholders' equity 1,181.6 793.7 387.9 Total capitalization 3,299.7 1,370.9 1928.8 Total net debt 1,873.6 127.9 1,745.7 As of |

|

|

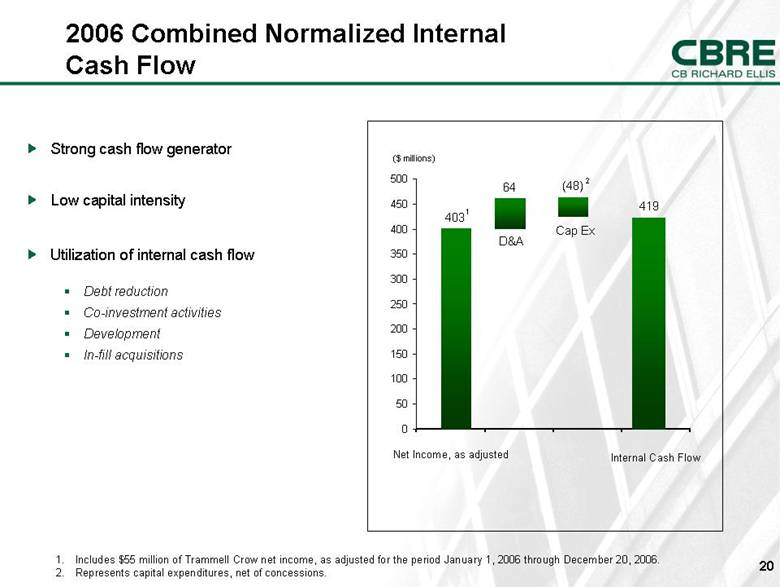

Strong cash flow generator Low capital intensity Utilization of internal cash flow Debt reduction Co-investment activities Development In-fill acquisitions Includes $55 million of Trammell Crow net income, as adjusted for the period January 1, 2006 through December 20, 2006. Represents capital expenditures, net of concessions. 2006 Combined Normalized Internal Cash Flow ($ millions) 64 403 Net Income, as adjusted D&A Cap Ex (48) 419 Internal Cash Flow 2 1 0 50 100 150 200 250 300 350 400 450 500 |

|

|

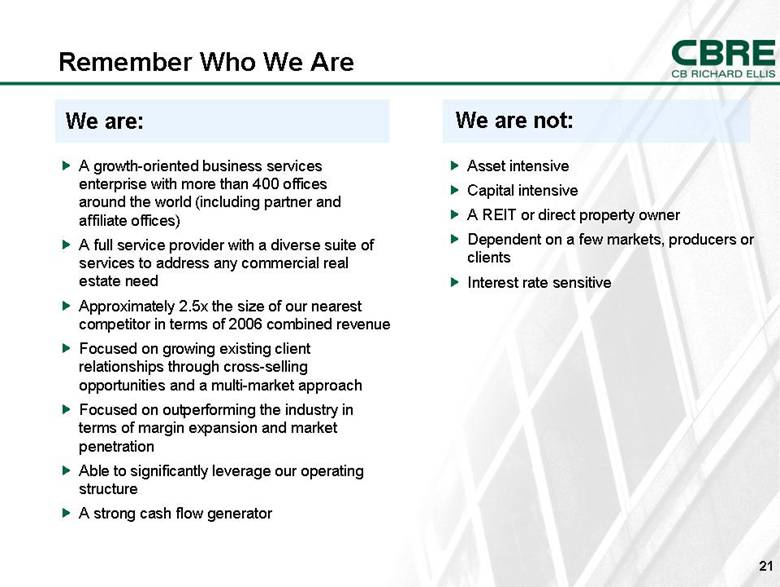

Remember Who We Are A growth-oriented business services enterprise with more than 400 offices around the world (including partner and affiliate offices) A full service provider with a diverse suite of services to address any commercial real estate need Approximately 2.5x the size of our nearest competitor in terms of 2006 combined revenue Focused on growing existing client relationships through cross-selling opportunities and a multi-market approach Focused on outperforming the industry in terms of margin expansion and market penetration Able to significantly leverage our operating structure A strong cash flow generator Asset intensive Capital intensive A REIT or direct property owner Dependent on a few markets, producers or clients Interest rate sensitive We are: We are not: |

|

|

Appendix |

|

|

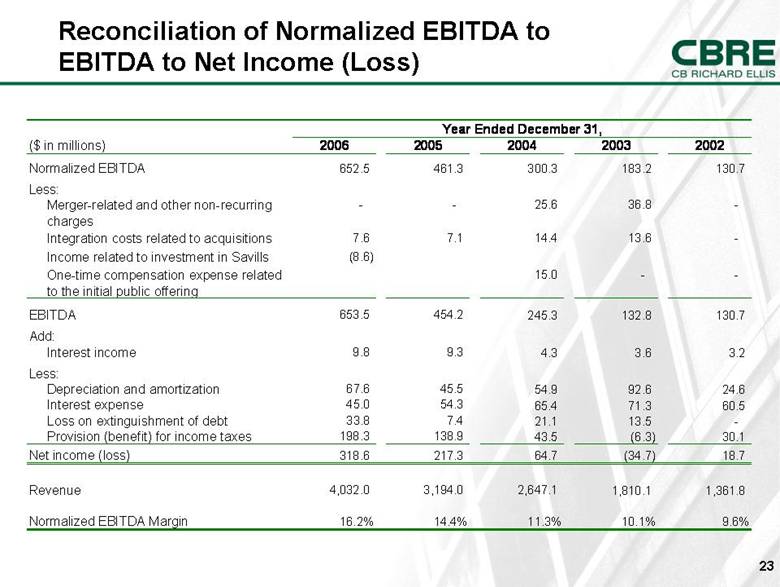

Reconciliation of Normalized EBITDA to EBITDA to Net Income (Loss) ($ in millions) 2006 2005 2004 2003 2002 Normalized EBITDA 652.5 461.3 300.3 183.2 130.7 Less: Merger-related and other non-recurring charges - - 25.6 36.8 - Integration costs related to acquisitions 7.6 7.1 14.4 13.6 - Income related to investment in Savills (8.6) One-time compensation expense related to the initial public offering 15.0 - - EBITDA 653.5 454.2 245.3 132.8 130.7 Add: 9.8 9.3 4.3 3.6 3.2 Less: 67.6 45.5 54.9 92.6 24.6 45.0 54.3 65.4 71.3 60.5 33.8 7.4 21.1 13.5 - 198.3 138.9 43.5 (6.3) 30.1 Net income (loss) 318.6 217.3 64.7 (34.7) 18.7 Revenue 4,032.0 3,194.0 2,647.1 1,810.1 1,361.8 Normalized EBITDA Margin 16.2% 14.4% 11.3% 10.1% 9.6% Year Ended December 31, Provision (benefit) for income taxes Loss on extinguishment of debt Interest expense Depreciation and amortization Interest income |

|

|

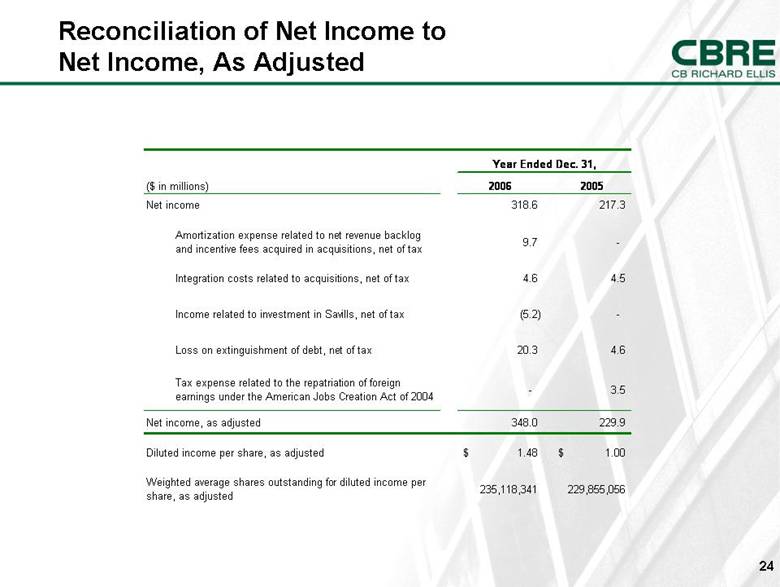

Reconciliation of Net Income to Net Income, As Adjusted Year Ended Dec. 31, ($ in millions) 2006 2005 Net income 318.6 217.3 Amortization expense related to net revenue backlog and incentive fees acquired in acquisitions, net of tax 9.7 - Integration costs related to acquisitions, net of tax 4.6 4.5 Income related to investment in Savills, net of tax (5.2) - Loss on extinguishment of debt, net of tax 20.3 4.6 Tax expense related to the repatriation of foreign earnings under the American Jobs Creation Act of 2004 - 3.5 Net income, as adjusted 348.0 229.9 Diluted income per share, as adjusted 1.48 $ 1.00 $ Weighted average shares outstanding for diluted income per share, as adjusted 235,118,341 229,855,056 |

|

|

|