Exhibit 99.1

|

|

Acquisition of Trammell Crow Company Investor Presentation October 2006 |

Exhibit 99.1

|

|

Acquisition of Trammell Crow Company Investor Presentation October 2006 |

|

|

Forward Looking Statements This presentation contains statements regarding the acquisition of Trammell Crow Company that are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements involve risks and uncertainties, including, but not limited to, the ability of the parties to close the transaction and successfully integrate the operations of Trammell Crow Company with CB Richard Ellis, the ability to leverage the integrated platform to capture a larger share of the commercial real estate market in the U.S., the cost of financing the transaction, the ability of the Company to achieve expense savings and other synergies as a result of the transaction and the price obtained for the sale of the ownership interest in Savills, plc, as well as other risks and uncertainties discussed in CB Richard Ellis’ filings with the Securities and Exchange Commission (SEC). Any forward-looking statements speak only as of the date of this release and, except to the extent required by applicable securities laws, CB Richard Ellis expressly disclaims any obligation to update or revise any of them to reflect actual results, any changes in expectations or any change in events. If CB Richard Ellis does update one or more forward-looking statements, no inference should be drawn that it will make additional updates with respect to those or other forward-looking statements. For additional information concerning factors that may cause actual results to differ from those anticipated in the forward-looking statements, and risks to CB Richard Ellis’ business in general, please refer to the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2005, its Quarterly Report on Form 10-Q for the quarter ended June 30, 2006, and its press releases and other periodic filings with the SEC. Such filings are available publicly and may be obtained off the CB Richard Ellis website at www.cbre.com or upon request from the CB Richard Ellis Investor Relations Department at investorrelations@cbre.com. |

|

|

Agenda Introduction Shelley Young Director, Investor Relations Transaction Overview & Rationale for Acquisition Brett White President & Chief Executive Officer Financial Aspects of Acquisition Ken Kay Chief Financial Officer Q&A CBRE Management Team |

|

|

Transaction Overview & Rationale for Acquisition Brett White, President & Chief Executive Officer CB Richard Ellis |

|

|

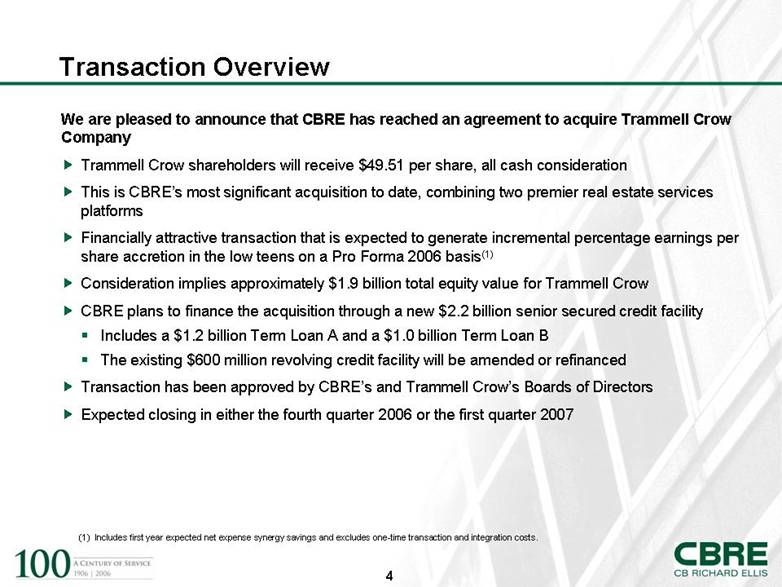

Transaction Overview We are pleased to announce that CBRE has reached an agreement to acquire Trammell Crow Company Trammell Crow shareholders will receive $49.51 per share, all cash consideration This is CBRE’s most significant acquisition to date, combining two premier real estate services platforms Financially attractive transaction that is expected to generate incremental percentage earnings per share accretion in the low teens on a Pro Forma 2006 basis(1) Consideration implies approximately $1.9 billion total equity value for Trammell Crow CBRE plans to finance the acquisition through a new $2.2 billion senior secured credit facility Includes a $1.2 billion Term Loan A and a $1.0 billion Term Loan B The existing $600 million revolving credit facility will be amended or refinanced Transaction has been approved by CBRE’s and Trammell Crow’s Boards of Directors Expected closing in either the fourth quarter 2006 or the first quarter 2007 (1) Includes first year expected net expense synergy savings and excludes one-time transaction and integration costs. |

|

|

Rationale for Acquisition A respected and leading industry brand that will add value to our brand Furthers CBRE’s position as the world’s premier commercial real estate services provider Complementary alignment, in particular our strength in Transaction Management is a perfect match with Trammell Crow’s strength in Property & Facilities Management and other outsourcing services Acquisition of Trammell Crow’s well respected D&I business Expands our blue chip client base Continues to diversify revenue sources Enhances operating leverage potential Combines two highly effective and complementary management teams Financially attractive transaction |

|

|

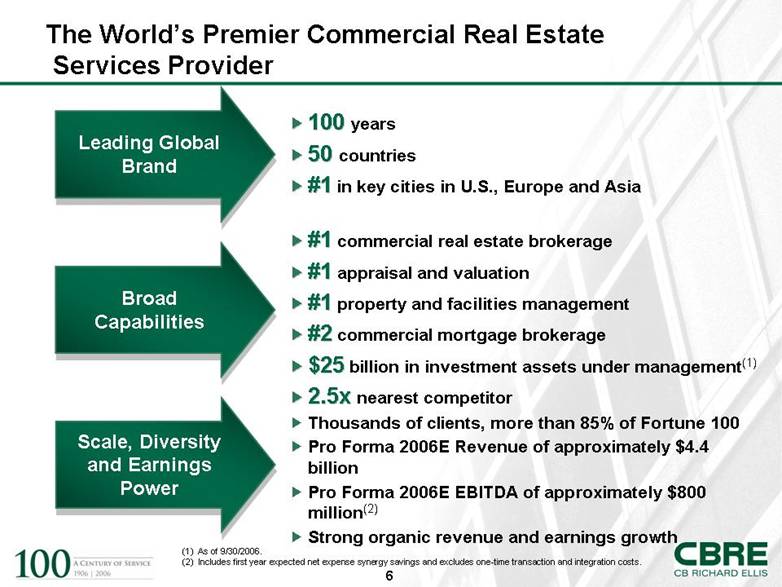

2.5x nearest competitor Thousands of clients, more than 85% of Fortune 100 Pro Forma 2006E Revenue of approximately $4.4 billion Pro Forma 2006E EBITDA of approximately $800 million(2) Strong organic revenue and earnings growth #1 commercial real estate brokerage #1 appraisal and valuation #1 property and facilities management #2 commercial mortgage brokerage $25 billion in investment assets under management(1) Leading Global Brand Broad Capabilities Scale, Diversity and Earnings Power 100 years 50 countries #1 in key cities in U.S., Europe and Asia (1) As of 9/30/2006. (2) Includes first year expected net expense synergy savings and excludes one-time transaction and integration costs. The World’s Premier Commercial Real Estate Services Provider |

|

|

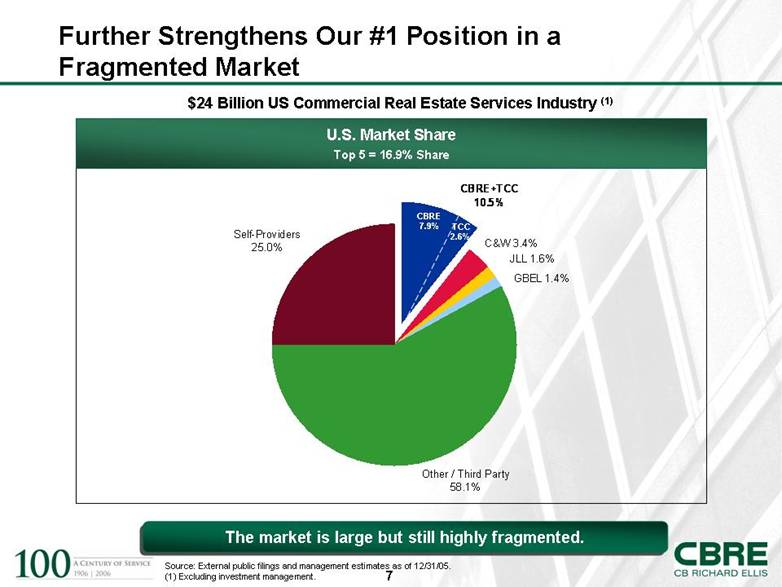

$24 Billion US Commercial Real Estate Services Industry (1)U.S. Market Share Top 5 = 16.9% Share Further Strengthens Our #1 Position in a Fragmented Market Source: External public filings and management estimates as of 12/31/05. (1) Excluding investment management. The market is large but still highly fragmented. CBRE 7.9% TCC 2.6% CBRE+TCC 10.5%C&W 3.4%JLL 1.6%GBEL 1.4%Other / Third Party 58.1%Self-Providers 25.0% |

|

|

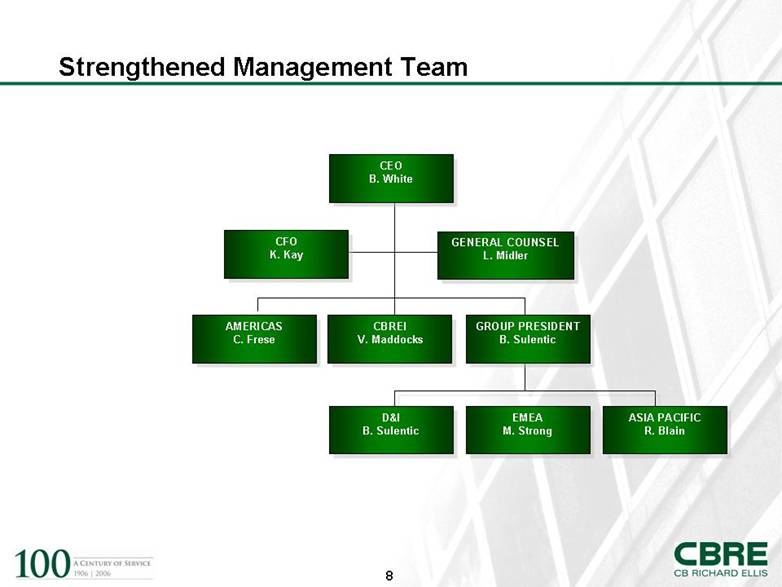

Strengthened Management Team CEO B. White GENERAL COUNSEL L. Midler CFO K. Kay GROUP PRESIDENT B. Sulentic CBREI V. Maddocks AMERICAS C. Frese D&I B. Sulentic EMEA M. Strong ASIA PACIFIC R. Blain |

|

|

Financial Aspects of Acquisition Ken Kay, Chief Financial Officer CB Richard Ellis |

|

|

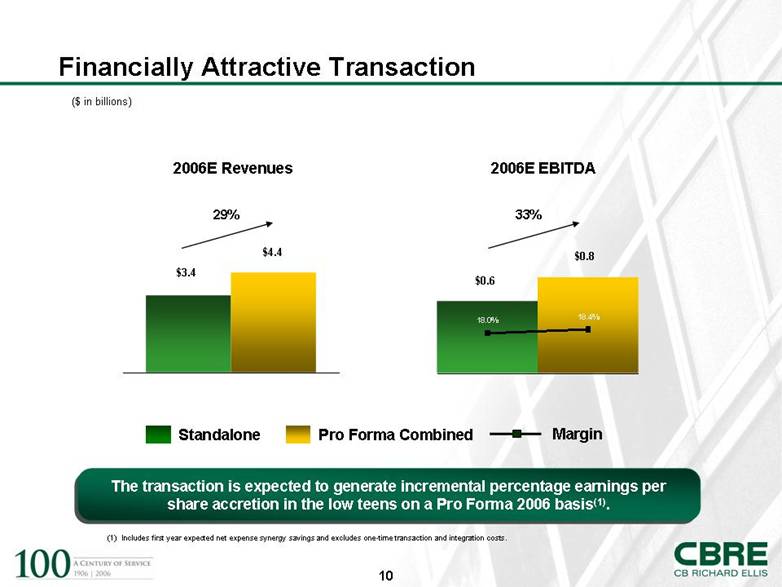

Financially Attractive Transaction $3.4 $4.4 29% ($ in billions) 2006E Revenues 2006E EBITDA The transaction is expected to generate incremental percentage earnings per share accretion in the low teens on a Pro Forma 2006 basis(1). Standalone Pro Forma Combined $0.6 $0.8 33% (1) Includes first year expected net expense synergy savings and excludes one-time transaction and integration costs.Margin 18.4% 18.0% |

|

|

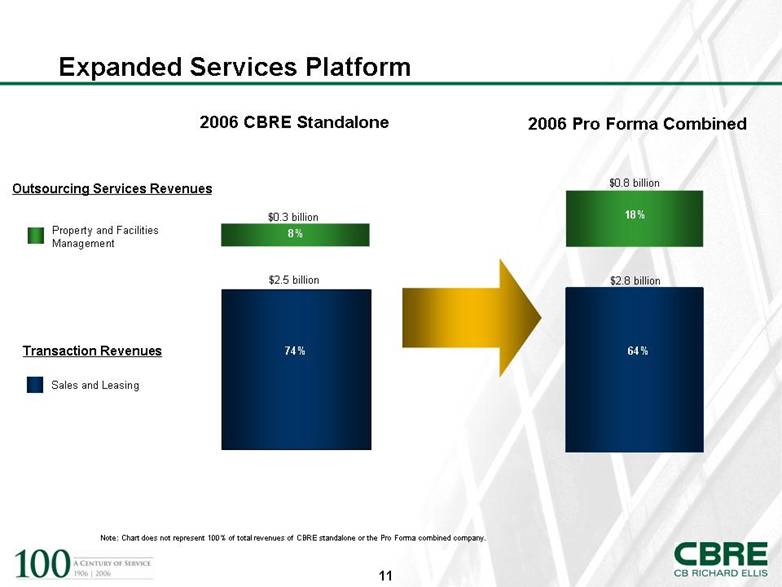

Expanded Services Platform Property and Facilities Management Sales and Leasing $0.3 billion $0.8 billion $2.8 billion 8% 18% [ ]% 2006 CBRE Standalone 2006 Pro Forma Combined Outsourcing Services Revenues Transaction Revenues$2.5 billion 74% 64% Note: Chart does not represent 100% of total revenues of CBRE standalone or the Pro Forma combined company. |

|

|

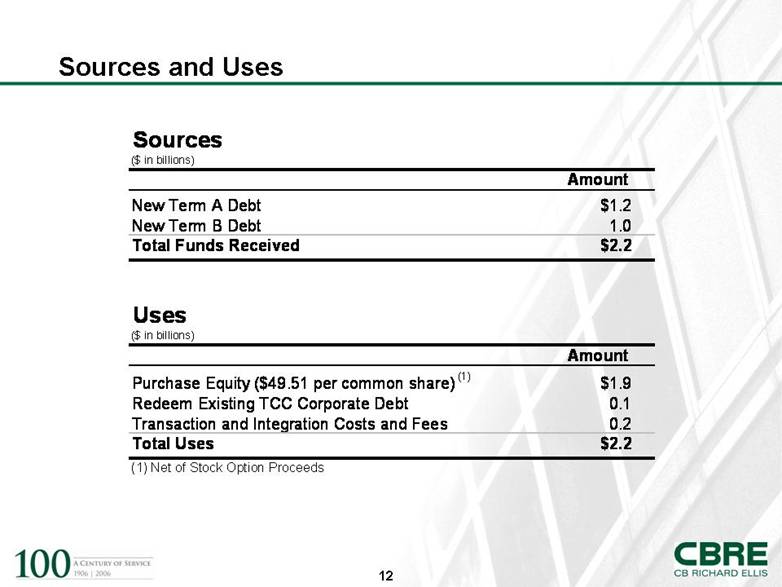

Sources and Uses Sources($ in billions)AmountNew Term A Debt$1.2New Term B Debt1.0Total Funds Received$2.2Uses($ in billions)AmountPurchase Equity ($49.51 per common share)(1)$1.9Redeem Existing TCC Corporate Debt0.1Transaction and Integration Costs and Fees0.2Total Uses$2.2(1) Net of Stock Option Proceeds |

|

|

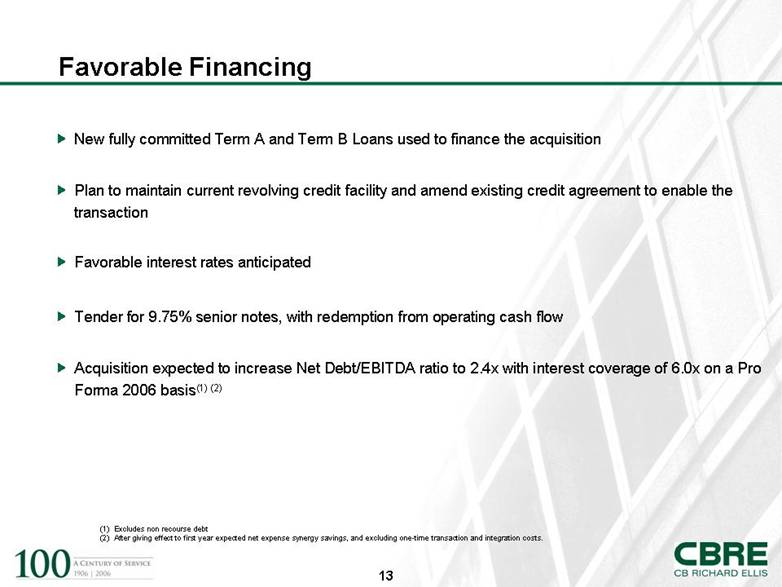

Favorable Financing New fully committed Term A and Term B Loans used to finance the acquisition Plan to maintain current revolving credit facility and amend existing credit agreement to enable the transaction Favorable interest rates anticipated Tender for 9.75% senior notes, with redemption from operating cash flow Acquisition expected to increase Net Debt/EBITDA ratio to 2.4x with interest coverage of 6.0x on a Pro Forma 2006 basis(1)(2) (1) Excludes non recourse debt (2) After giving effect to first year expected net expense synergy savings, and excluding one-time transaction and integration costs. |

|

|

Q&A CB Richard Ellis Management Team |

|

|

|