Exhibit 99.1

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Link to searchable text of slide shown above

Searchable text section of graphics shown above

Business Review Day

CBRE Overview

Brett White, President

Ken Kay, CFO

March 23, 2005

[GRAPHIC]

[LOGO]

Forward Looking Statements

This presentation contains statements that are forward looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements should be considered as estimates only and actual results may ultimately differ from these estimates. Except to the extent required by applicable securities laws, CB Richard Ellis undertakes no obligation to update or publicly revise any of the forward-looking statements that you may hear today. Please refer to our annual report on Form 10-K and our quarterly reports on Form 10-Q, which are filed with the SEC and available at the SEC’s website (http://www.sec.gov), for a full discussion of the risks and other factors, that may impact any estimates that you may hear today. Our responses to questions must be limited to information that is acceptable for dissemination within the public domain. In addition, we may make certain statements during the course of this presentation which include references to “non-GAAP financial measures,” as defined by SEC regulations. As required by these regulations, we have provided reconciliations of these measures to what we believe are the most directly comparable GAAP measures.

1

Overview

2

The World Class Commercial Real Estate Services Provider

Leading Global Brand

• 99 years

• 50 countries

• #1 in key cities in U.S., Europe and Asia

Broad Capabilities

• #1 commercial real estate brokerage

• #1 appraisal and valuation

• #1 property and facilities management

• #2 commercial mortgage brokerage

• $15.1 billion in investment assets under management

Scale, Diversity and Earnings and Power

• 2x nearest competitor

• Thousands of clients, more than 70% of Fortune 100

• 2004 Revenue of $2.4 billion

• 2004 Normalized EBITDA of $300.3 million (1)

• Strong organic revenue and earnings growth for 2004

(1). Excludes merger-related charges, integration costs and one-time IPO compensation expense.

3

Global Reach & Local Leadership

2004 Revenue by Region

[CHART]

Leading

Market Positions

|

New York |

|

ý |

|

|

|

|

|

London |

|

ý |

|

|

|

|

|

Los Angeles |

|

ý |

|

|

|

|

|

Chicago |

|

ý |

|

|

|

|

|

Sydney |

|

ý |

|

|

|

|

|

Paris |

|

ý |

|

|

|

|

|

Washington, D.C. |

|

ý |

|

|

|

|

|

Madrid |

|

ý |

|

|

|

|

|

Singapore |

|

ý |

CBRE is unique in offering customers global coverage and leading local expertise.

4

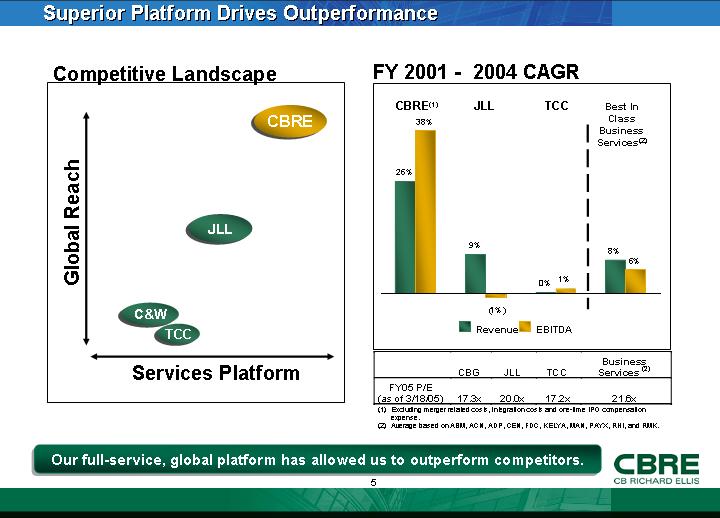

Superior Platform Drives Outperformance

Competitive Landscape

[CHART]

FY 2001 - 2004 CAGR

[CHART]

|

|

|

CBG |

|

JLL |

|

TCC |

|

Business |

|

|

FY05 P/E |

|

|

|

|

|

|

|

|

|

|

(as of 3/18/05) |

|

17.3 |

x |

20.0 |

x |

17.2 |

x |

21.6 |

x |

(1) Excluding merger related costs, integration costs and one-time IPO compensation expense.

(2) Average based on ABM, ACN, ADP, CEN, FDC, KELYA, MAN, PAYX, RHI, and RMK.

Our full-service, global platform has allowed us to outperform competitors.

5

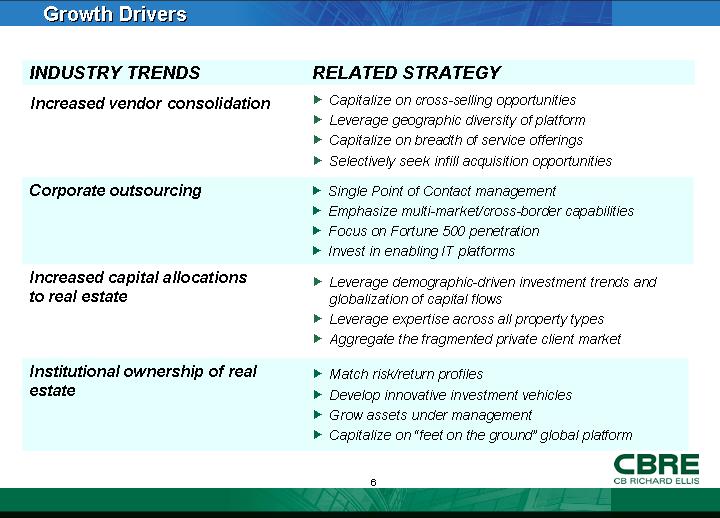

Growth Drivers

|

INDUSTRY TRENDS |

|

RELATED STRATEGY |

|

|

|

|

|

Increased vendor consolidation |

|

• Capitalize on cross-selling opportunities • Leverage geographic diversity of platform • Capitalize on breadth of service offerings • Selectively seek infill acquisition opportunities |

|

|

|

|

|

Corporate outsourcing |

|

• Single Point of Contact management • Emphasize multi-market/cross-border capabilities • Focus on Fortune 500 penetration • Invest in enabling IT platforms |

|

|

|

|

|

Increased capital allocations to real estate |

|

• Leverage demographic-driven investment trends and globalization of capital flows • Leverage expertise across all property types • Aggregate the fragmented private client market |

|

|

|

|

|

Institutional ownership of real estate |

|

• Match risk/return profiles • Develop innovative investment vehicles • Grow assets under management • Capitalize on “feet on the ground” global platform |

6

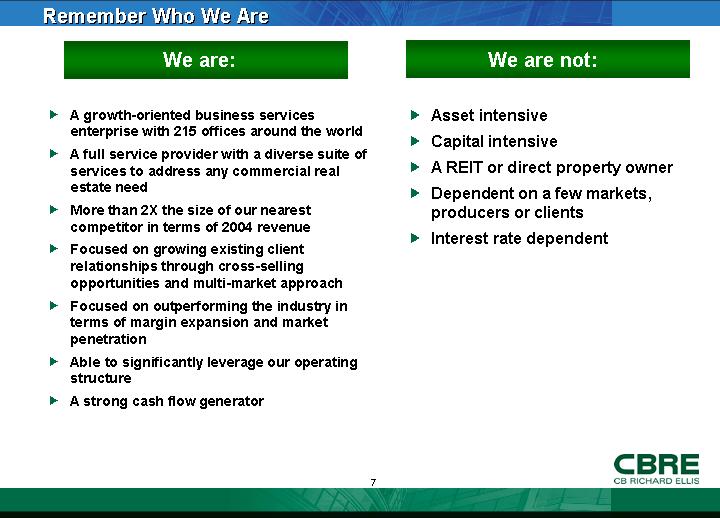

Remember Who We Are

We are:

• A growth-oriented business services enterprise with 215 offices around the world

• A full service provider with a diverse suite of services to address any commercial real estate need

• More than 2X the size of our nearest competitor in terms of 2004 revenue

• Focused on growing existing client relationships through cross-selling opportunities and multi-market approach

• Focused on outperforming the industry in terms of margin expansion and market penetration

• Able to significantly leverage our operating structure

• A strong cash flow generator

We are not:

• Asset intensive

• Capital intensive

• A REIT or direct property owner

• Dependent on a few markets, producers or clients

• Interest rate dependent

7

Financial Overview

8

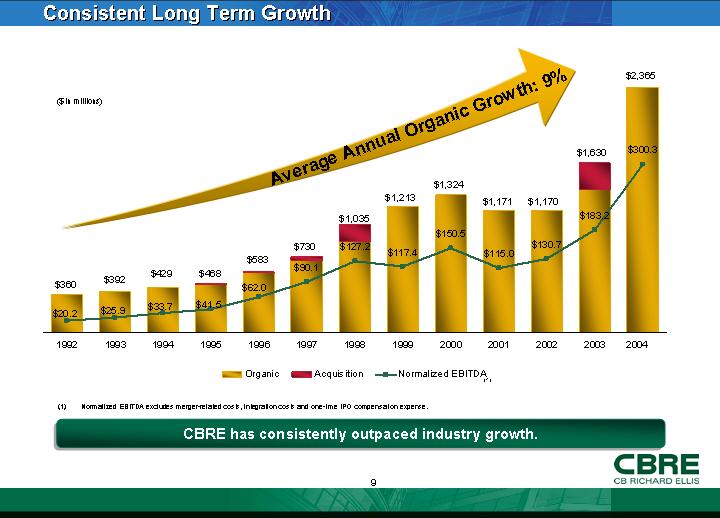

Consistent Long Term Growth

[CHART]

(1) Normalized EBITDA excludes merger-related costs, integration costs and one-time IPO compensation expense.

CBRE has consistently outpaced industry growth.

9

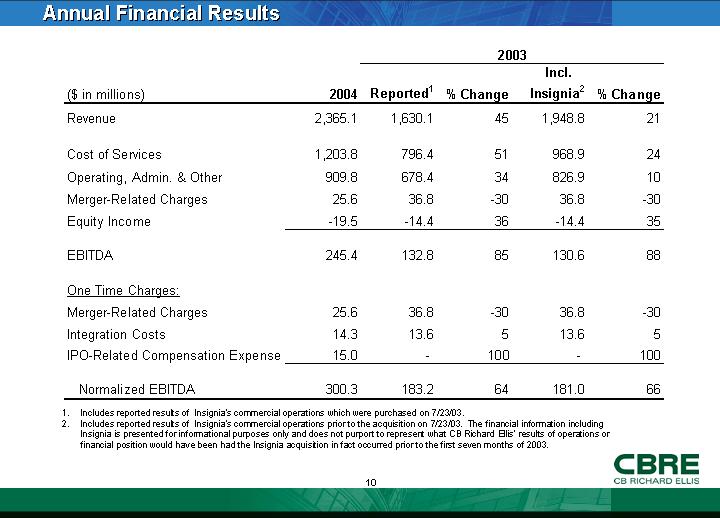

Annual Financial Results

|

|

|

|

|

2003 |

|

||||||

|

|

|

|

|

|

|

|

|

Incl. |

|

|

|

|

($ in millions) |

|

2004 |

|

Reported(1) |

|

% Change |

|

Insignia(2) |

|

% Change |

|

|

Revenue |

|

2,365.1 |

|

1,630.1 |

|

45 |

|

1,948.8 |

|

21 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cost of Services |

|

1,203.8 |

|

796.4 |

|

51 |

|

968.9 |

|

24 |

|

|

Operating, Admin. & Other |

|

909.8 |

|

678.4 |

|

34 |

|

826.9 |

|

10 |

|

|

Merger-Related Charges |

|

25.6 |

|

36.8 |

|

-30 |

|

36.8 |

|

-30 |

|

|

Equity Income |

|

-19.5 |

|

-14.4 |

|

36 |

|

-14.4 |

|

35 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EBITDA |

|

245.4 |

|

132.8 |

|

85 |

|

130.6 |

|

88 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

One Time Charges: |

|

|

|

|

|

|

|

|

|

|

|

|

Merger-Related Charges |

|

25.6 |

|

36.8 |

|

-30 |

|

36.8 |

|

-30 |

|

|

Integration Costs |

|

14.3 |

|

13.6 |

|

5 |

|

13.6 |

|

5 |

|

|

IPO-Related Compensation Expense |

|

15.0 |

|

— |

|

100 |

|

— |

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Normalized EBITDA |

|

300.3 |

|

183.2 |

|

64 |

|

181.0 |

|

66 |

|

(1). Includes reported results of Insignia’s commercial operations which were purchased on 7/23/03.

(2). Includes reported results of Insignia’s commercial operations prior to the acquisition on 7/23/03. The financial information including Insignia is presented for informational purposes only and does not purport to represent what CB Richard Ellis’ results of operations or financial position would have been had the Insignia acquisition in fact occurred prior to the first seven months of 2003.

10

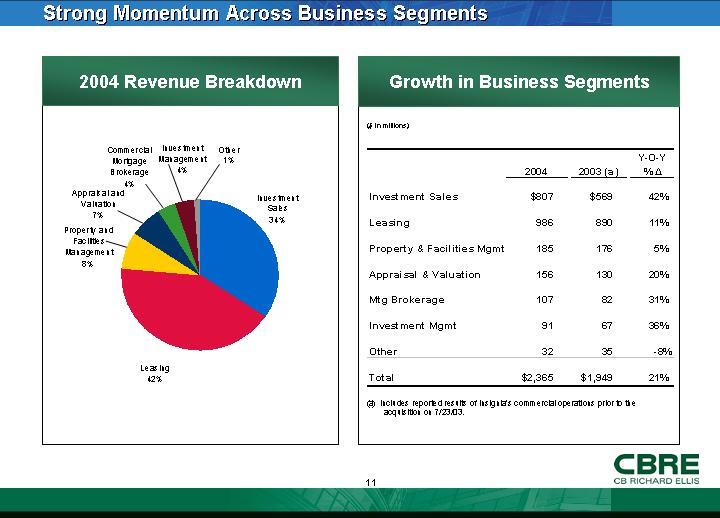

Strong Momentum Across Business Segments

2004 Revenue Breakdown

[CHART]

Growth in Business Segments

($ in millions)

|

|

|

|

|

|

|

Y-O-Y |

|

||

|

|

|

2004 |

|

2003 (a) |

|

% Δ |

|

||

|

Investment Sales |

|

$ |

807 |

|

$ |

569 |

|

42 |

% |

|

Leasing |

|

986 |

|

890 |

|

11 |

% |

||

|

Property & Facilities Mgmt |

|

185 |

|

176 |

|

5 |

% |

||

|

Appraisal & Valuation |

|

156 |

|

130 |

|

20 |

% |

||

|

Mtg Brokerage |

|

107 |

|

82 |

|

31 |

% |

||

|

Investment Mgmt |

|

91 |

|

67 |

|

36 |

% |

||

|

Other |

|

32 |

|

35 |

|

-8 |

% |

||

|

Total |

|

$ |

2,365 |

|

$ |

1,949 |

|

21 |

% |

(a) Includes reported results of Insignia’s commercial operations prior to the acquisition on 7/23/03.

11

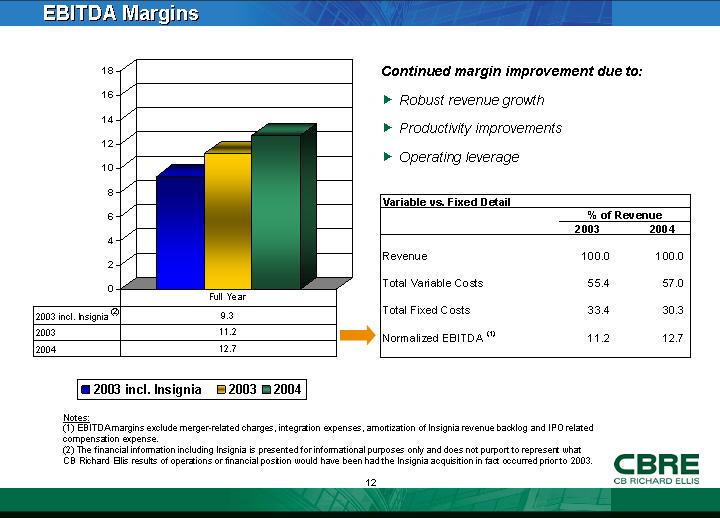

EBITDA Margins

[CHART]

Continued margin improvement due to:

• Robust revenue growth

• Productivity improvements

• Operating leverage

Variable vs. Fixed Detail

|

|

|

% of Revenue |

|

||

|

|

|

2003 |

|

2004 |

|

|

|

|

|

|

|

|

|

Revenue |

|

100.0 |

|

100.0 |

|

|

|

|

|

|

|

|

|

Total Variable Costs |

|

55.4 |

|

57.0 |

|

|

|

|

|

|

|

|

|

Total Fixed Costs |

|

33.4 |

|

30.3 |

|

|

|

|

|

|

|

|

|

Normalized EBITDA (1) |

|

11.2 |

|

12.7 |

|

Notes:

(1) EBITDA margins exclude merger-related charges, integration expenses, amortization of Insignia revenue backlog and IPO related compensation expense.

(2) The financial information including Insignia is presented for informational purposes only and does not purport to represent what CB Richard Ellis results of operations or financial position would have been had the Insignia acquisition in fact occurred prior to 2003.

12

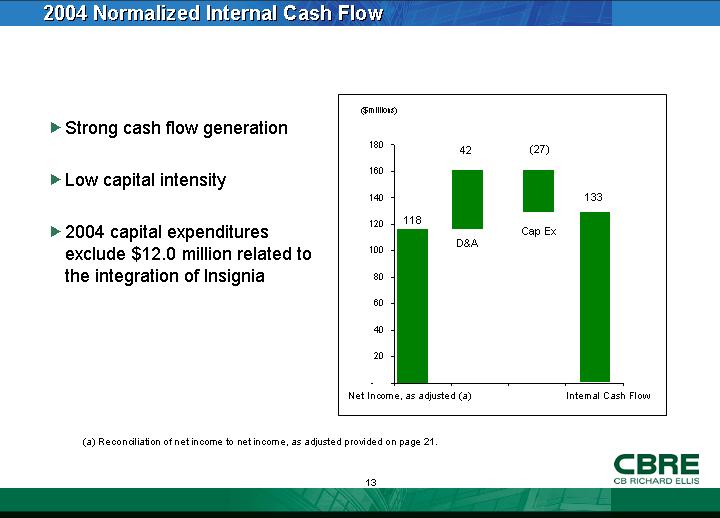

2004 Normalized Internal Cash Flow

• Strong cash flow generation

• Low capital intensity

• 2004 capital expenditures exclude $12.0 million related to the integration of Insignia

[CHART]

(a) Reconciliation of net income to net income, as adjusted provided on page 21.

13

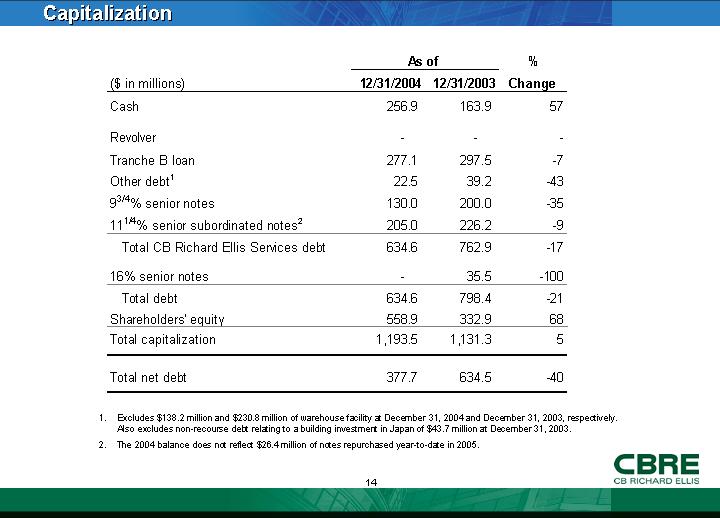

Capitalization

|

|

|

As of |

|

% |

|

||

|

($ in millions) |

|

12/31/2004 |

|

12/31/2003 |

|

Change |

|

|

Cash |

|

256.9 |

|

163.9 |

|

57 |

|

|

|

|

|

|

|

|

|

|

|

Revolver |

|

— |

|

— |

|

— |

|

|

Tranche B loan |

|

277.1 |

|

297.5 |

|

-7 |

|

|

Other debt(1) |

|

22.5 |

|

39.2 |

|

-43 |

|

|

93/4% senior notes |

|

130.0 |

|

200.0 |

|

-35 |

|

|

111/4% senior subordinated notes(2) |

|

205.0 |

|

226.2 |

|

-9 |

|

|

Total CB Richard Ellis Services debt |

|

634.6 |

|

762.9 |

|

-17 |

|

|

|

|

|

|

|

|

|

|

|

16% senior notes |

|

— |

|

35.5 |

|

-100 |

|

|

Total debt |

|

634.6 |

|

798.4 |

|

-21 |

|

|

Shareholders’ equity |

|

558.9 |

|

332.9 |

|

68 |

|

|

Total capitalization |

|

1,193.5 |

|

1,131.3 |

|

5 |

|

|

|

|

|

|

|

|

|

|

|

Total net debt |

|

377.7 |

|

634.5 |

|

-40 |

|

(1). Excludes $138.2 million and $230.8 million of warehouse facility at December 31, 2004 and December 31, 2003, respectively. Also excludes non-recourse debt relating to a building investment in Japan of $43.7 million at December 31, 2003.

(2). The 2004 balance does not reflect $26.4 million of notes repurchased year-to-date in 2005.

14

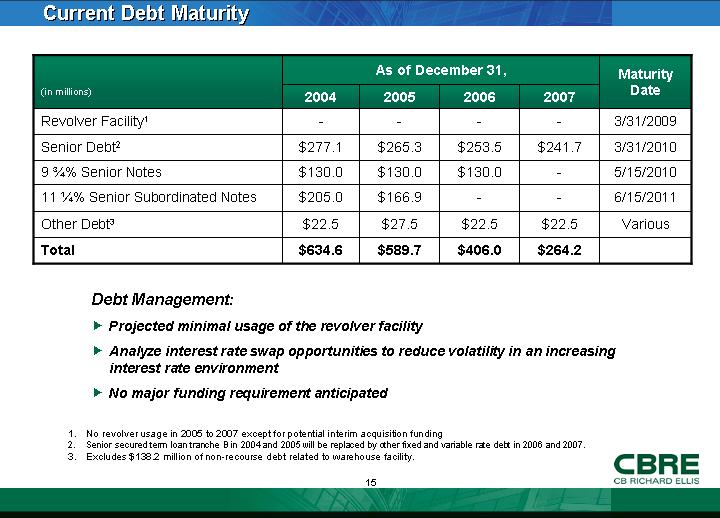

Current Debt Maturity

|

|

|

As of December 31, |

|

Maturity |

|

||||||||||

|

(in millions) |

|

2004 |

|

2005 |

|

2006 |

|

2007 |

|

Date |

|

||||

|

Revolver Facility(1) |

|

— |

|

— |

|

— |

|

— |

|

3/31/2009 |

|

||||

|

Senior Debt(2) |

|

$ |

277.1 |

|

$ |

265.3 |

|

$ |

253.5 |

|

$ |

241.7 |

|

3/31/2010 |

|

|

9 ¾% Senior Notes |

|

$ |

130.0 |

|

$ |

130.0 |

|

$ |

130.0 |

|

— |

|

5/15/2010 |

|

|

|

11 ¼% Senior Subordinated Notes |

|

$ |

205.0 |

|

$ |

166.9 |

|

— |

|

— |

|

6/15/2011 |

|

||

|

Other Debt(3) |

|

$ |

22.5 |

|

$ |

27.5 |

|

$ |

22.5 |

|

$ |

22.5 |

|

Various |

|

|

Total |

|

$ |

634.6 |

|

$ |

589.7 |

|

$ |

406.0 |

|

$ |

264.2 |

|

|

|

Debt Management:

• Projected minimal usage of the revolver facility

• Analyze interest rate swap opportunities to reduce volatility in an increasing interest rate environment

• No major funding requirement anticipated

(1). No revolver usage in 2005 to 2007 except for potential interim acquisition funding

(2). Senior secured term loan tranche B in 2004 and 2005 will be replaced by other fixed and variable rate debt in 2006 and 2007.

(3). Excludes $138.2 million of non-recourse debt related to warehouse facility.

15

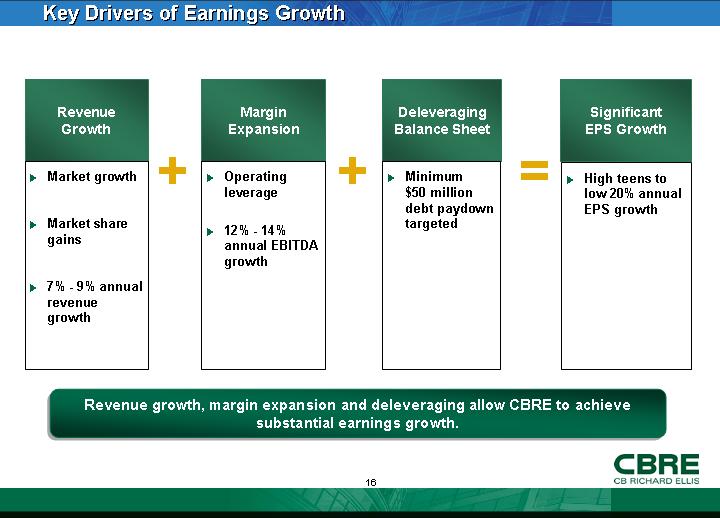

Key Drivers of Earnings Growth

|

Revenue |

|

Margin |

|

Deleveraging |

|

Significant |

|

Growth |

|

Expansion |

|

Balance Sheet |

|

EPS Growth |

|

|

|

|

|

|

|

|

|

• Market growth |

+ |

• Operating leverage |

+ |

• Minimum $50 million |

= |

• High teens to low |

|

|

|

|

|

debt paydown targeted |

|

20% annual EPS |

|

|

|

|

|

|

|

growth |

|

• Market share gains |

|

• 12% - 14% annual |

|

|

|

|

|

|

|

EBITDA growth |

|

|

|

|

|

• 7% - 9% annual revenue |

|

|

|

|

|

|

Revenue growth, margin expansion and deleveraging allow CBRE to achieve substantial earnings growth.

16

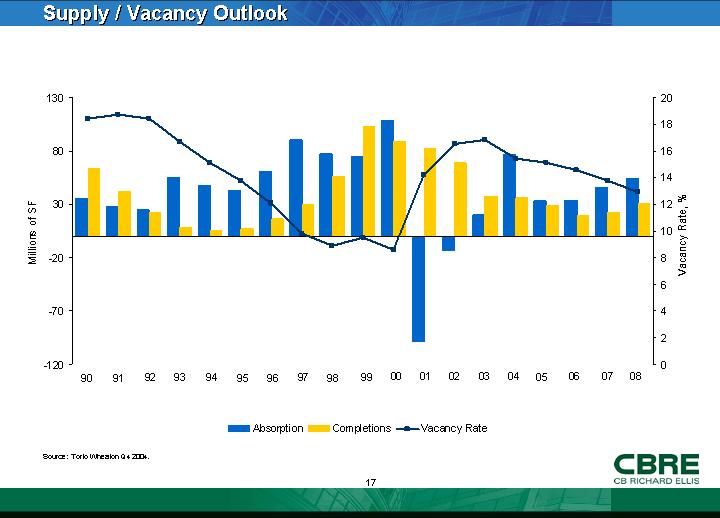

Supply / Vacancy Outlook

[CHART]

Source: Torto Wheaton Q4 2004.

17

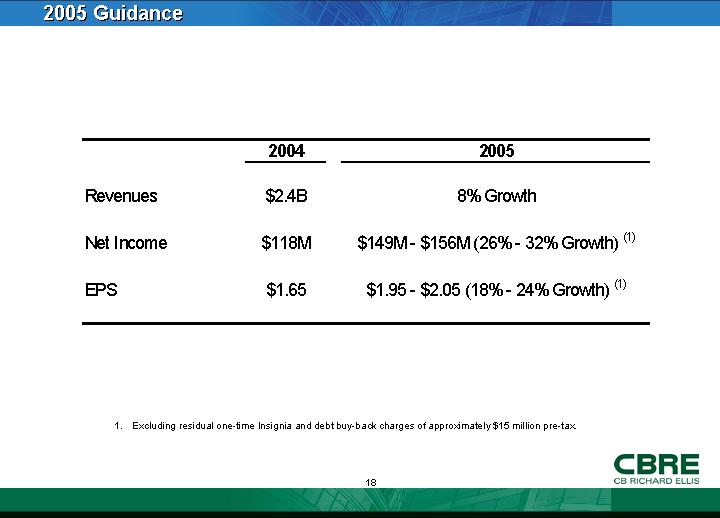

2005 Guidance

|

|

|

2004 |

|

2005 |

|

|

|

|

|

|

|

|

|

|

|

Revenues |

|

$ |

2.4 |

B |

8% Growth |

|

|

|

|

|

|

|

|

|

|

Net Income |

|

$ |

118 |

M |

$149M - $156M (26% - 32% Growth) (1) |

|

|

|

|

|

|

|

|

|

|

EPS |

|

$ |

1.65 |

|

$1.95 - $2.05 (18% - 24% Growth) (1) |

|

(1). Excluding residual one-time Insignia and debt buy-back charges of approximately $15 million pre-tax.

18

[LOGO]

19

Appendix

20

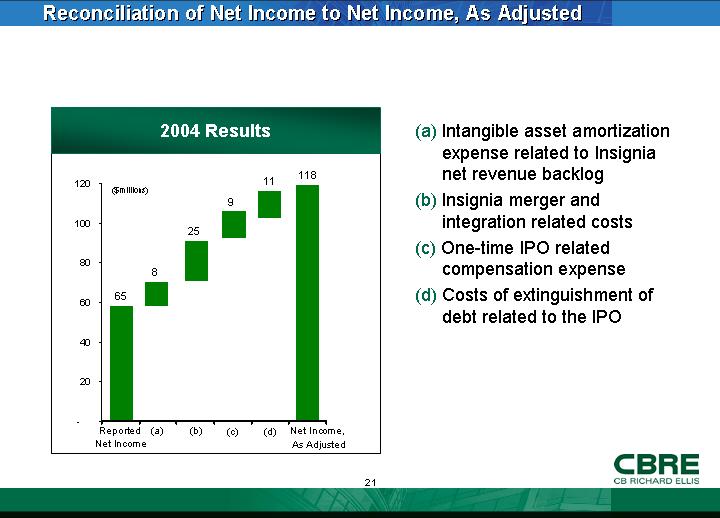

Reconciliation of Net Income to Net Income, As Adjusted

[CHART]

(a) Intangible asset amortization expense related to Insignia net revenue backlog

(b) Insignia merger and integration related costs

(c) One-time IPO related compensation expense

(d) Costs of extinguishment of debt related to the IPO

21

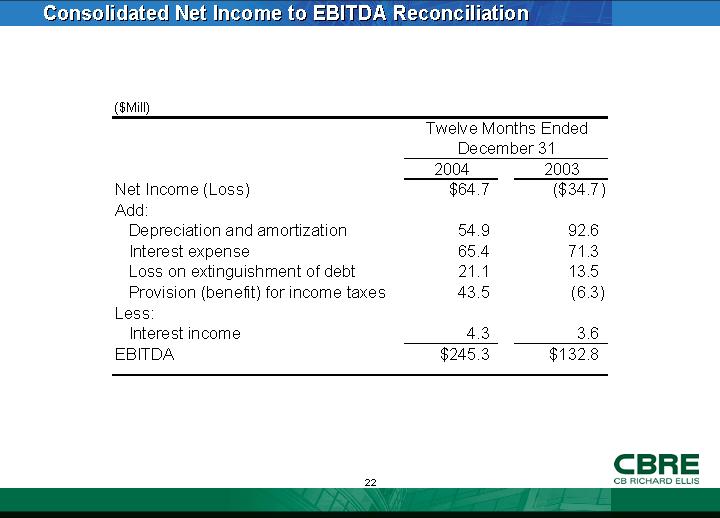

Consolidated Net Income to EBITDA Reconciliation

|

|

|

Twelve Months Ended |

|

||||

|

($Mill) |

|

2004 |

|

2003 |

|

||

|

Net Income (Loss) |

|

$ |

64.7 |

|

$ |

(34.7 |

) |

|

Add: |

|

|

|

|

|

||

|

Depreciation and amortization |

|

54.9 |

|

92.6 |

|

||

|

Interest expense |

|

65.4 |

|

71.3 |

|

||

|

Loss on extinguishment of debt |

|

21.1 |

|

13.5 |

|

||

|

Provision (benefit) for income taxes |

|

43.5 |

|

(6.3 |

) |

||

|

Less: |

|

|

|

|

|

||

|

Interest income |

|

4.3 |

|

3.6 |

|

||

|

EBITDA |

|

$ |

245.3 |

|

$ |

132.8 |

|

22

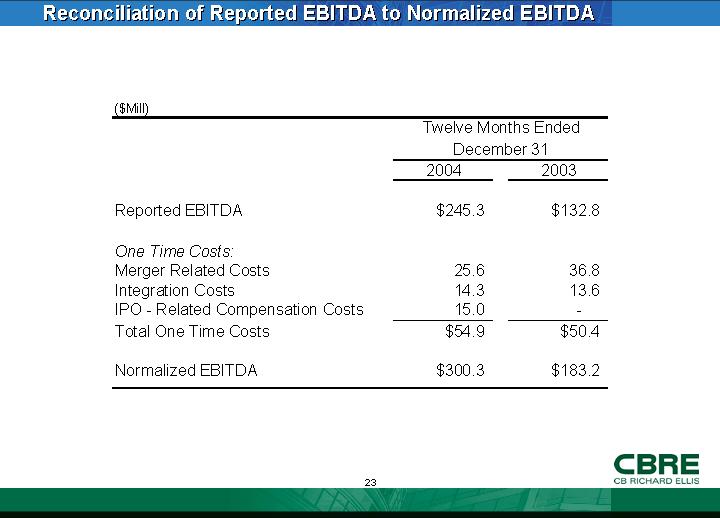

Reconciliation of Reported EBITDA to Normalized EBITDA

|

|

|

Twelve Months Ended |

|

||||

|

($Mill) |

|

2004 |

|

2003 |

|

||

|

|

|

|

|

|

|

||

|

Reported EBITDA |

|

$ |

245.3 |

|

$ |

132.8 |

|

|

|

|

|

|

|

|

||

|

One Time Costs: |

|

|

|

|

|

||

|

Merger Related Costs |

|

25.6 |

|

36.8 |

|

||

|

Integration Costs |

|

14.3 |

|

13.6 |

|

||

|

IPO - Related Compensation Costs |

|

15.0 |

|

— |

|

||

|

Total One Time Costs |

|

$ |

54.9 |

|

$ |

50.4 |

|

|

|

|

|

|

|

|

||

|

Normalized EBITDA |

|

$ |

300.3 |

|

$ |

183.2 |

|

23